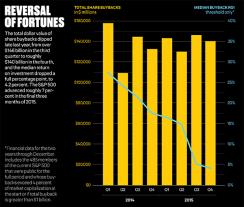

The Wal-Mart Stores brand advertises nothing if not low prices for consumers. Last October that applied as well to the giant retailer’s stock, which had sagged a third below the price from a few months earlier — one everyday low price situation the company felt it needed to fix. Wal-Mart responded by, among other steps, authorizing a $20 billion program to buy back its shares.

Bentonville, Arkansas–based Wal-Mart intends to complete the buybacks over the next two years, shrinking its current market capitalization of $216 billion by around 10 percent. Its buyback announcement topped all others in 2015, with the exception of the $50 billion stock-repurchase program that Fairfield, Connecticut, industrial conglomerate General Electric unveiled in April, when stocks were still rising.

That makes Wal-Mart something of an outlier. Across the Standard & Poor’s 500, buyback announcements and repurchasing activity eased in the final months of 2015, when stocks slid amid mounting volatility.

Institutional Investor’s most recent Corporate Buyback Scorecard, created by Fortuna Advisors using data from Capital IQ, judges buyback programs over eight quarters. The latest Scorecard ranks buyback return on investment at 299 companies where repurchases of stock reduced market capitalization by 4 percent or more, and, in a few instances, exceeded $1 billion, two thresholds for materiality.

The Buyback Scorecard, which Institutional Investor has been publishing since the first quarter of 2013, provides investors with a set of metrics to evaluate corporate buyback programs. The core measure, buyback ROI, estimates the internal rate of return of cash flow associated with buybacks. Cash flow includes money paid to investors who sold their shares; the value of undistributed dividends; and an estimate of the value of the accumulated repurchased shares.

| Buyback Scorecard The S&P 500 as Stock Repurchasers Best & Worst CompaniesIndustry Comparisons |

The evidence from buybacks over the past eight quarters ending in the fourth quarter of 2015 indicates that buyback programs have lost some luster. Median ROI posts a seventh successive decline on the latest Scorecard, to 4.2 percent, from 29.6 percent two years ago. Part of that decline stems from subpar execution in buyback effectiveness, a metric that measures the gap between buyback ROI and annualized total shareholder returns. Positive buyback effectiveness indicates that companies repurchased shares ahead of rising price trends. When buyback ROI is negative, however, companies bought back shares only to discover stock prices falling. Access to internal data on daily repurchase activity can refine Scorecard results.

The overall effectiveness of repurchase programs peaked on 2013’s second-quarter Scorecard, when buyback ROI surpassed underlying shareholder return by nearly 10 percent. The relationship reversed in mid-2014, with buyback ROI falling short of shareholder return. On the current Scorecard buyback effectiveness is down to –5 percent, the second-lowest since we launched the Scorecard.

If pressed to validate its buyback execution, Wal-Mart might have a tough time right now. The retailer’s buyback ROI is running at –21.2 percent, trailing 260 other companies, including five of its six peers in the Food and Staples Retailing sector. Only Whole Foods Market, headquartered in Austin, Texas, fared worse. A four-year window doesn’t improve the view. Wal-Mart tumbles 49 places from its Scorecard ranking two years ago, which reflected buybacks in 2012 and 2013. Wal-Mart’s buyback effectiveness in the latest period is at –12.9 percent. Poor timing of buybacks did more damage to shareholder wealth than the decline in the underlying shares.

What’s more, the impressive $20 billion figure of Wal-Mart’s newest buyback program requires an asterisk. That amount includes nearly $9 billion rolled over from the $15 billion buyback program announced two years ago. At that time, Wal-Mart’s chief financial officer, Charles Holley, touted strong cash flow and pride in “our long history of returning value to shareholders through the combination of dividends and share repurchases.”

Taking two bows for the same buyback undermines investor faith that companies will execute as promised. And it may erode a company’s ability to signal confidence, a prime motive for many buybacks. “The market is smart,” says John Tomlinson, head of consumer research at New York–based ITG Investment Research. “Companies can’t continue to say they’re going to buy back stock and not do it.”

Double-dipping on buybacks is not unique to Wal-Mart. In December, Chicago aerospace giant Boeing Co. scrapped a $12 billion buyback authorization from 2014 with $5.3 billion still unused and advertised a new $14 billion repurchase plan. In February, American International Group, the New York–based insurer that was at the epicenter of the financial crisis, authorized $5 billion on top of a $10.7 billion repurchase authorization with nearly $6 billion still untouched.

Wal-Mart might not want to publicize the counterintuitive reality that by not repurchasing those shares the retailer actually preserved value for shareholders; the business would have lost more if it had spent all the money. Even so, Wal-Mart buyback ROI on the current Scorecard underperforms total shareholder return by nearly 13 percentage points.

Tomlinson sees no legerdemain at work. Market forces, he says, compelled Wal-Mart to step up as it did. Authorizing more buybacks suggested that its robust cash flow could support huge demands. “[Wal-Mart] wanted to assure the shareholder base they were not running away from their capital-allocation strategy,” says Tomlinson, especially in terms of returning capital to investors. Investors responded, if cautiously. By early March, shares traded at a 10 percent premium to the price just before the buyback was announced — commensurate with the expected impact of the program.

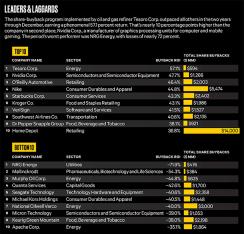

Elsewhere in the rankings the largest independent refiner and marketer of oil in the U.S. proves that buyback ROI can flourish even in beleaguered sectors. San Antonio, Texas–based Tesoro Corp. garners first place on the current Scorecard. Falling oil prices have fueled big profits at refiners. Tesoro delivered buyback ROI of 57.1 percent with buyback effectiveness of 7.1 percent. Only Tesoro boasts buyback ROI over 50 percent, while seven companies surpassed 40 percent, and 11 were above 30 percent.

No. 3 O’Reilly Automotive, based in Springfield, Missouri, also put buybacks to good use. The automotive retailer authorized $5 billion in buybacks in January 2011 and subsequently added $500 million to that program. “When we look at buying stock back, we look at what we think the long-term discounted cash flow value is and set our targets that way,” CFO Tom McFall told analysts in August 2015.

During the conference call McFall credited buybacks in part to unexpected performance. Faster-than-anticipated growth attracted suppliers to finance inventory. The resulting cash flow prompted O’Reilly to find ways to maximize the return to shareholders. “To date that’s been repurchasing shares,” McFall said.

UBS analyst Michael Lasser noted that the only piece of O’Reilly that was not working to its potential was the balance sheet and pressed McFall on buyback execution. “How much we repurchase during a quarter is a portion of our long-term plan,” McFall replied, but cash flow and market conditions decide the pace: “We really look at buybacks as call to call.” Early in 2015 “we were in a dark period ... and we bought back not very many shares.” A month later, when cash flow picked up, O’Reilly revved up its buybacks.

Lasser applauds the strategy: “O’Reilly has produced fantastic operating results while enhancing the return for shareholders by consistently buying back their stock.”

One of the Scorecard’s biggest losers this quarter operates in the pharmaceuticals, biotechnology and life sciences sector: St. Louis–based Mallinckrodt Pharmaceuticals. Stock repurchased by the company surrendered more than half its value, even as annualized total shareholder return produced a 19 percent gain.

Houston-based Quanta Services, which provides construction, maintenance and technology services, retired 52.5 percent of its market capitalization — more than any other company in the current Scorecard.

Quanta CEO James O’Neil described the final tranche, a $1.25 billion buyback, during the second-quarter conference call with the zest that often accompanies such announcements. “This is by far the largest share-repurchase authorization in Quanta’s history,” he said. “This action reflects our commitment to creating shareholder value and our ongoing confidence in the longer-term outlook for our business.”

The final accounting on Quanta’s buyback ROI awaits expiration of its accelerated repurchase agreement, when the initial price per share, using the volume-weighted average pricing before the buyback began, will be adjusted. That adjustment, or true-up, reconciles the sum earmarked for the buyback with the volume-weighted average price per share over the course of the buyback.

Like many companies, Quanta has seen its stock fall. A falling stock price provides one benefit — it allows cash allocations to repurchase more shares. However, it all but guarantees negative buyback ROI. In 296th place overall, Quanta underperformed 30 of 32 companies in buyback ROI in the Capital Goods sector. The sector generated a median buyback ROI of 1.6 percent, whereas Quanta posted –42.6 percent and lagged shareholder return on its stock by 33 percentage points, subject to the true-up.

Quanta investor relations chief Kip Rupp urges a wait-and-see attitude before judging a buyback program that was designed to pass to shareholders a windfall from the sale of a business unit. “We had sold off Sunesys and had $800 million in cash come in the door,” Rupp says. “We did determine that our stock was attractive and that this was the best use of capital for shareholders.”

Senior analyst Daniel Mannes at Nashville, Tennessee–based Avondale Partners agrees. “There was not an easily identifiable better use of proceeds given the size,” says Mannes. A special dividend might send the wrong signal to growth-oriented investors, and the infusion would swamp capital expenditures. If you want to nitpick, acknowledges Mannes, Quanta might not have launched a buyback program had it known that the stock would peak in June and then fall. “It’s not wrong,” Mannes says, “but you could certainly quibble with the timing.”

One way to identify companies that have risen or fallen the most in the Scorecard rankings is to look back at successive two-year windows. For instance, Raleigh, North Carolina–based open-source software developer Red Hat generated buyback ROI in 2012 and 2013 of –8 percent, only slightly better than its anemic buyback effectiveness. Of 261 companies on that Scorecard, Red Hat landed at No. 254 in buyback ROI.

However, following an accelerated share-repurchase program that retired 6 million shares at an average price of $56.47, Red Hat’s buyback ROI rose to 31.2 percent on the current Scorecard, placing it among the top 20 companies. Red Hat’s shares hit a high of $83.65 on December 30, then slipped into the $60s by early March during the brutal early-2016 market. Reclaiming that share price high will be a challenge, say analysts at Bank of America Merrill Lynch: “We believe that the stock achieving high end of historical 25 times free cash flow multiple will be hampered by secular concern,” BofA Merrill reported in February.

Buybacks don’t exist in a vacuum. The Scorecard allows investors to scrutinize buyback programs through several lenses. “Before buyback ROI, there was no return-based metric for comparing buybacks to allocations like M&A, capital expenditures or R&D,” says Fortuna CEO Gregory Milano. “Buyback ROI allows us to look back at a company’s track record and see if they’ve earned adequate returns.”

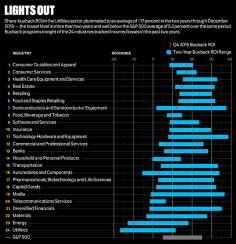

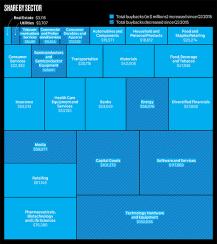

Among 24 sectors Technology Hardware and Equipment repurchased the most stock. These companies sank $150 billion into buybacks, three times the median for all sectors. Their collective buyback ROI of 7.9 percent, however, trails those of ten sectors, led by Consumer Services and Consumer Durables and Apparel, which tie with median buyback ROIs of 17.2 percent. Utilities comes in last, with a –17 percent in buyback ROI, offset by the fact that the sector had the lowest volume of buybacks of any industry beside Real Estate.

Quintile groupings can also provide benchmarks for evaluating buybacks. Investors can compare companies in five tranches of buyback ROI, median dollar total buybacks and total dollar buybacks as a percentage of market capitalization. For instance, that last metric, total dollar buybacks as a percentage of market cap, shows the buyback ROI that companies were able to deliver based on how much market cap they eliminated. The top tranche reduced market cap by over 20 percent. These aggressive buybacks produced, however, the lowest median buyback ROI at –14.3 percent. Companies in the middle tranche retired just under 8 percent of market cap and enjoyed median buyback ROI of 10.1 percent. The bottom tranche retired 4.2 percent of market capital, with median buyback ROI at 7.5 percent.

Senior analyst Michael Halloran at Robert W. Baird in Milwaukee argues the widely held notion that stock repurchases are exempt from judgment applied to other uses of shareholders’ capital. “Buybacks have nothing to do with the destruction of value,” he insists.

That’s good news for Flowserve Corp., an Irving, Texas–based maker of industrial pumps, valves and seals that Halloran follows. In terms of buyback ROI, Flowserve sits right above Quanta Services in the basement of the Capital Goods sector, with a buyback ROI of –28 percent. Another investment with a negative ROI over two years might irk investors, but, said Flowserve CEO Mark Blinn last October, “Returning capital to shareholders was another key priority during the quarter.”

At Flowserve, Halloran sees a balance sheet in good shape, a suitable amount earmarked for accelerated share repurchase and ample free cash flow available for capital expenditures, M&A or capital returns to shareholders. “I’m not going to ding them for a consistent policy when over time it will probably prove to be okay,” he says. His current rating on the stock is neutral.

However, Halloran also admits that buybacks might allow managers to punt instead of taking the kind of risk that spurs growth. “I certainly suspect that is part of the discussion,” he says, noting that boards insist on hitting a lot of boxes before material transactions can proceed. For shareholders, as the Scorecard reveals, no-risk buybacks pose risk, too.

Get more on corporations and equities.