Despite a significant increase in uncertainty following major US policy changes, private markets continue to present attractive opportunities. Valuations and yields are appealing given a multi-year slowdown in fundraising and deal activity. Furthermore, private markets tend to show resilience in times of volatility. To navigate uncertainties, we suggest investors be discerning in selecting strategies with attractive risk/return profiles and to ensure diversification across private market strategies.

Despite current challenges, our outlook for new private markets investments remains optimistic, although we are cognizant of increased risks arising from significant US policy changes and resulting uncertainties affecting growth, inflation and interest rates.

We see the most attractive allocation options in the current market as being characterized by:

- Balanced capital supply and demand dynamics, leading to favorable entry valuations and yields.

- Domestic companies and assets offering some insulation from geopolitical risks and trade conflicts.

- Opportunities for additional risk premiums arising from complexity, innovation, transformation, or market inefficiencies.

- Robust downside protection through limited leverage or asset backing.

- Reduced correlation with listed markets, owing to distinct risk exposures.

To read more click here: Private Markets Investment Outlook Q2 2025: Opportunities amid uncertainty

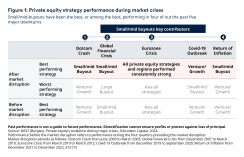

Private equity: Small is beautiful

In 2024, the prolonged slowdown in private equity deal, exit and fundraising activity that has persisted since 2022 showed signs of bottoming out. In our view, this creates an attractive environment for new investments as, historically, private equity has delivered particularly strong performance when capital supply and demand dynamics are favorable.

As we have shown previously, over the past 25 years, private equity has thrived during periods of market disruption, achieving twice the outperformance in times of high volatility compared to more stable periods. Importantly, in four of the five major market disruptions within this timeframe, small and mid-sized buyouts were key contributors to private equity’s resilience. In 2025, we again expect small and mid-sized buyouts to offer particularly attractive opportunities for enhancing portfolio resilience.

Small and mid-sized buyouts look especially attractive for multiple reasons

We prefer small to mid-sized buyouts over larger transactions, as they benefit from a favorable capital supply-demand dynamic and face lower competition for a broader range of deals. Additionally, this market segment offers compelling entry points for investment, with less reliance on debt financing and significant potential for value creation. Furthermore, small to mid-sized buyouts can grow to become acquisition targets for larger buyout funds, providing an additional exit path. In the current market context, it is especially beneficial for smaller buyouts that they typically focus on domestic companies, making them less susceptible to trade and geopolitical tensions.

Continuation funds poised to continue strong growth trend

The secondaries market saw a record transaction volume of $160 billion in 2024. Continuation funds remained a key growth area, providing valuable liquidity options to investors and accounting for a record $71 billion in transaction value. Continuation funds are a compelling exit route for portfolio companies, especially small and mid-market firms with significant transformational growth potential. In the short term, this appeal is amplified by current uncertainties that are slowing the recovery of exit markets. In the long term, considering the ongoing growth of private equity and the trend of companies staying private longer, we project that the continuation fund market segment could reach an annual transaction value of $250 billion within the next decade.

Despite exuberance around AI, innovation dynamics remain attractive

Efficiency gains demonstrated by DeepSeek have sparked concerns about the significant capital expenditure related to AI, contributing to valuation pressures for certain AI companies, particularly in the US. We view these risks as relatively contained for private companies, as venture and growth capital investments typically favor capex-light investments focused on the application layer of the AI stack. Companies leveraging AI models can benefit significantly from the associated efficiency gains. Moreover, while AI investments reached 15% of global venture investment in 2024, innovation and disruption extend beyond AI, encompassing sectors such as biotech, fintech, climate tech, and deep tech. Accelerating innovation dynamics across various sectors are supported by increased political focus on venture capital as a strategic tool to bolster national competitiveness. We see significant potential in the recovering biotech sector, which has faced years of risk aversion, and generally find early-stage venture more attractively priced and isolated from current uncertainties than late-stage venture and growth capital.

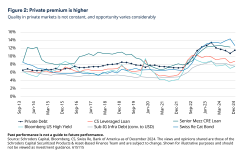

Private debt and credit alternatives: Specialized strategies offer attractive yields

Volatility has significantly increased due to the uncertainty surrounding US policy changes. In the short term, we anticipate that inflation may remain elevated or even rise, thereby exerting pressure on both consumers and companies. If businesses are unable to pass these higher costs onto consumers, profit margins could decline, potentially leading to increased unemployment in the US and exerting additional pressure on the global economy.

Given the Federal Reserve’s dual mandate, we would expect to see a substantial decline in the Federal Funds rate in the latter half of the year should unemployment rise. Additionally, we believe that increasing uncertainty may hinder investment in property development, consumer spending, corporate capital expenditure, and project investments.

Refinancing creates opportunities in commercial real estate debt

While we anticipate a decrease in the initiation of commercial real estate development projects, we foresee a strong demand for capital to refinance construction loans for completed projects, as well as for maturing loans. These needs are likely to be urgent, coinciding with a period of market uncertainty that has impeded issuance in syndicated markets, such as Commercial Mortgage-Backed Securities (CMBS). Considering the varying attractiveness of fundamentals across regions and property types, selectivity remains crucial. We generally favor lending for multi-family properties, such as apartments, and providing transitional financing for completed projects.

Infrastructure debt provides stable cashflows amid volatility

As inflation concerns resurface and volatility increases, stable defensive cashflows become crucial portfolio additions. In this context, infrastructure debt offers a unique opportunity for high-quality, stable, and high-income investments. Specialty finance and asset-based lending provide diversification and benefit from market inefficiencies.

Specialty finance and asset-based lending provide diversification and benefit from market inefficiencies

Just as liquid market volatility brings opportunities in adjacent private markets for real estate debt, infrastructure debt, specialty finance and asset-based lending offer additional income and diversify risks by focusing on consumer-oriented borrowers and SMEs. The variety of investment opportunities adds to diversification benefits. They can be sole originated or syndicated to a club, allowing for a variety of tenors and the creation of solutions that span both illiquid and liquid allocations.

Insurance-linked securities: The ultimate diversifier

Today, insurance-linked securities stand out. Their unique advantage lies in their lack of correlation with the macroeconomy, providing a much-needed respite from unstable market performance. This advantage is further enhanced by attractive valuations, as insured events offer opportunities for re-pricing. The Palisades and Eaton wildfires in California, expected to result in significant losses estimated at $40 billion, exemplify this potential. We foresee that the consistent level of catastrophe losses experienced by the insurance industry will continue to fuel the demand for protection. This demand is likely to maintain spreads of insurance-linked securities at historically high levels, positioning it as one of the most attractive options among alternative fixed income asset classes due to its appealing risk premiums. Well-collateralized debt helps navigate current uncertainties Over the past five years, corporate balance sheets have deleveraged, and incomes remain robust. However, given the prevailing uncertainty, it is crucial to focus on strong borrowers and higher-priority collateral. We anticipate that weaker or more leveraged consumers and companies may face increased challenges, potentially leading to higher default rates. The ability to select well-collateralized debt, backed by strong borrowers and robust security packages, is a significant advantage of private debt markets.

To read the full report that discusses each asset class in more detail, click here (Private Markets Investment Outlook Q2 2025: Opportunities amid uncertainty)

Important information

Marketing material for qualified investors only. All investments involve risk, including loss of principal.

The views and opinions contained herein are those of Schroders Capital and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. Such opinions are subject to change without notice. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment recommendations. Any reference to regions/ countries/ sectors/ stocks/ securities is for illustrative purposes only and not a recommendation to buy or sell any financial instruments or adopt a specific investment strategy. Schroders Capital has expressed its own views and opinions in this document and these may change.

This information is a marketing communication

Information herein is believed to be reliable but Schroders Capital does not warrant its completeness or accuracy. The data contained in this document has been sourced by Schroders Capital and should be independently verified. Third party data is owned or licenced by the data provider and may not be reproduced, extracted or used for any other purpose without the data provider’s consent. Neither Schroders Capital, nor the data provider, will have any liability in connection with the third-party data.

The forecasts stated in the document are the result of statistical modelling, based on a number of assumptions. Forecasts are subject to a high level of uncertainty regarding future economic and market factors that may affect actual future performance. The forecasts are provided to you for information purposes as at today’s date. Our assumptions may change materially with changes in underlying assumptions that may occur, among other things, as economic and market conditions change. We assume no obligation to provide you with updates or changes to this data as assumptions, economic and market conditions, models or other matters change.

This document may contain “forward-looking” information, such as forecasts or projections. Please note that any such information is not a guarantee of any future performance and there is no assurance that any forecast or projection will be realized.

Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amount originally invested. Diversification cannot ensure profits or protect against loss of principal.

Schroders Capital is the private markets investment division of Schroders plc. Schroders Capital Management (US) Inc. (‘Schroders Capital US’), registered as an investment adviser with the US Securities and Exchange Commission (SEC). Issued by Schroder Fund Advisors LLC (“SFA”), CRD Number 24129, registered as a limited purpose broker-dealer with the Financial Industry Regulatory Authority (FINRA) and as an Exempt Market Dealer with the securities regulatory authorities in Alberta, British Columbia, Manitoba, New Brunswick, Newfoundland and Labrador, Nova Scotia, Ontario, Quebec, and Saskatchewan. Schroder Fund Advisors LLC, 7 Bryant Park, New York, NY 10018-3706. For more information, visit www.schroderscapital.com