Alternative assets have become an increasingly important component of model portfolios, offering investors unique opportunities to invest in private market assets that are typically available only to large institutions. While the asset class is broad, alternatives are typically illiquid investments such private equity and private credit, along with real estate, commodities, and managed futures. Both alternative assets and model portfolios have seen a significant rise in popularity in recent years. Private debt assets under management grew by more than 460% from 2010 to 2022, reaching $1.4 trillion.1 The global alternative investments market is projected to reach $24.5 trillion by 2028, up from approximately $16.3 trillion at the end of 2020, according to figures from RBC Wealth Management.2 This rising interest in alternatives may be driven by the prospect of generating yields that exceed those of publicly traded stocks and bonds, their historically low correlation with public market price volatility, and their increasing availability to investors through vehicles such as model portfolios.

Alternative Assets in Model Portfolios

The breadth of alternative assets allows investors to use them to pursue a variety of their financial goals such as risk mitigation or return enhancement. Conservative portfolios may leverage alternatives to manage volatility (by attempting to reduce equity correlation via managed futures), while aggressive portfolios might use them to seek higher returns compared with publicly traded assets.

A key challenge – and benefit – with alternative investments is their inherently low correlation with traditional asset classes such as public equities and fixed income. While this diversification can be valuable, it must be carefully balanced to avoid inadvertently sacrificing long-term return potential. Properly funding alternative allocations is critical to ensuring they complement, rather than detract from, overall portfolio performance.

"Integrating alternative assets into portfolios offers several key benefits: the potential for higher returns due to illiquidity premiums, enhanced diversification through lower correlations, strong performance during market downturns, and access to non-correlated income streams.” says Patrick Jamin, Head of Platform Channels at Kovitz Investment Group Partners, a Focus Partners Firm. While the use of the asset class now includes various vehicles for liquidity, Jamin cautions that alternatives should be applied only when they make sense "While alternative investments were historically limited to LP structures, investors now have access to more liquid vehicles such as nontraditional ETFs and innovative structures like interval 40 Act funds. Still, careful attention to liquidity constraints and thorough due diligence remain essential to ensure suitability.” say Jamin.

For example, market-neutral liquid alternative strategies may offer appealing return opportunities while maintaining low correlation with traditional assets. However, they should be funded strategically to maintain portfolio balance. Managed futures and CTA strategies for instance, are often funded from fixed income – sometimes even more than 100% – with the remaining allocation offset by an overweight position in equities.

This approach ensures that diversification benefits are captured without compromising the portfolio’s risk-return profile.

Demand among advisors for model customization and alternative assets is on the rise, says Karl Desmond, client portfolio manager at Invesco. “Some of the new, unique requests we’re getting are related to how financial advisors may position custom model portfolios for their high-net-worth clients. For example, these advisors are asking about how we might include exposure to individual stocks and/or bonds via separately managed accounts (SMAs), as well as less liquid alternative asset classes, into their broader model portfolios.”

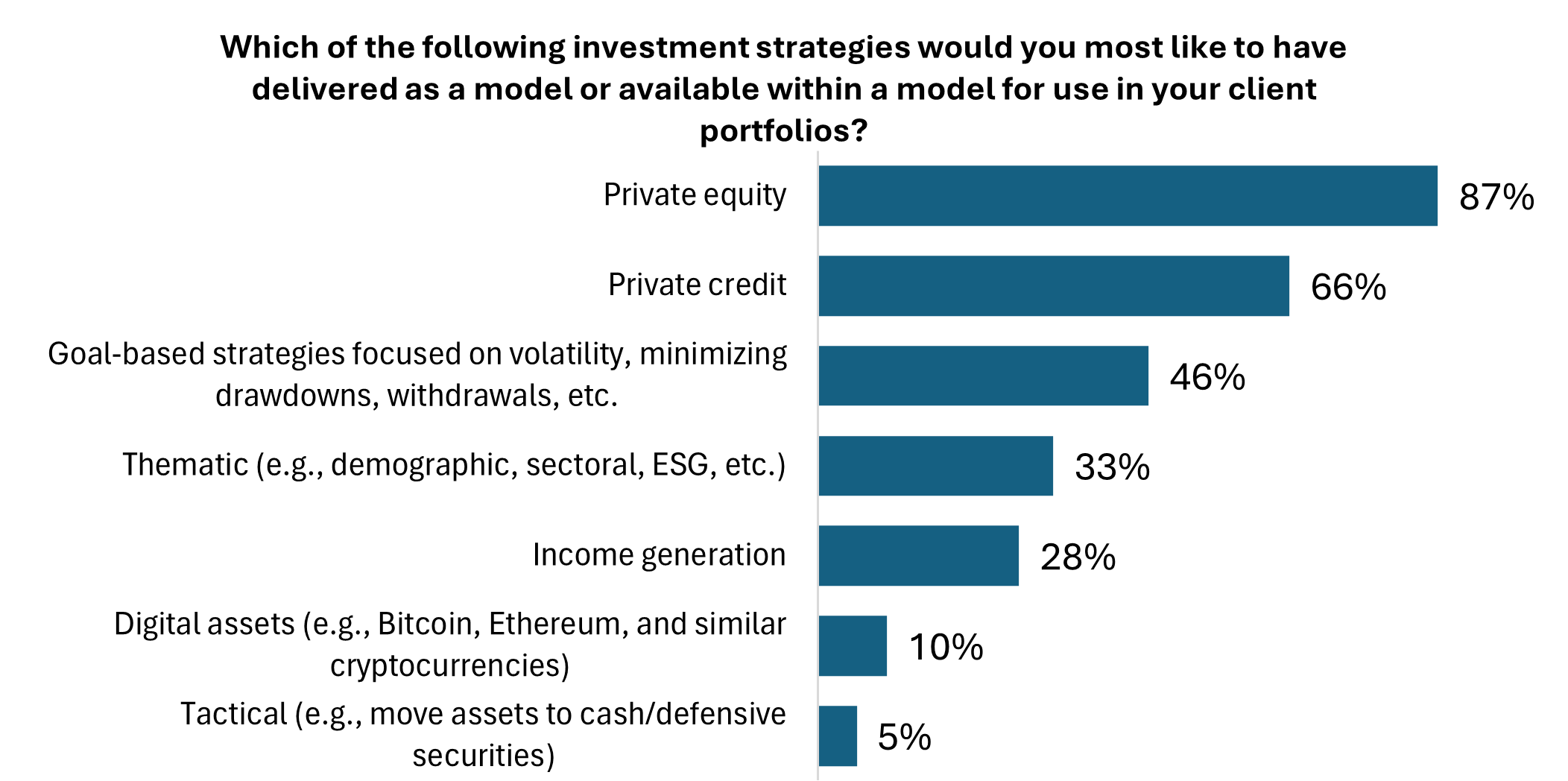

Recent research confirms the demand for alternative assets in model portfolios among advisors and their clients. In a 2024 study from BlackRock and Institutional Investor’s custom research group, a solid majority of the 500 wealth managers in the study say they’d like to have private equity or private credit available to clients through model portfolios (see figure below).3 In the same study, a majority of the 250 wealth management clients participating say they are “eager to invest in sophisticated financial assets such as private market assets, hedge funds, private equity, etc. which are typically available only through investment professionals.”

Advisors seek private market alternatives delivered via model portfolios

“Alternative assets are a common topic when we develop custom model portfolios with our clients”, says Karl Desmond of Invesco. “The benefits of model portfolios are fairly well known: it’s all about saving time in your day as a financial advisor, and deploying that time with existing clients and building your business. Custom model portfolios are beneficial because advisors can co-create the portfolios with a firm like Invesco, versus taking portfolios off-the-shelf, which a lot of the time have no exposure to alternative asset classes.” Thoughtful customization – that is, when an advisor combines and tailors various models and other instruments to meet client needs – is a compelling use case for alternative assets. Advisors are likely to “have preferences for some investment vehicles, such as ETFs or mutual funds. They may have views on the use of alternative assets like private equity or private credit too,” says Desmond. Accordingly, by customizing model portfolios, advisors are able to bring in their viewpoints on these asset classes, and combine it with our institutional asset allocation process.”

1https://alterdomus.com/insight/alternative-asset-annual-review-how-markets-performed-in-2023/?utm_source=chatgpt.com

3“Model Portfolios: A New Generation of Investment Solutions for Wealth Managers and Their Clients,” published by Institutional Investor Custom Research Lab, 2024.

Important Information

For Institutional & Financial Professional Use Only - Not for the General Public

This information should not be relied upon as investment advice, research, or a recommendation by BlackRock regarding (i) the funds, (ii) the use or suitability of the model portfolios or (iii) any security in particular. Only an investor and their financial professional know enough about their circumstances to make an investment decision.

Carefully consider the investment objectives, risk factors, charges and expenses of funds within the model portfolios before investing. This and other information can be found in the funds’ prospectuses or, if available, the summary prospectuses which may be obtained by visiting each fund company’s website or calling their toll-free number. For BlackRock and iShares Funds, please visit www.BlackRock.com or www.iShares.com. Read the prospectuses carefully before investing.

Investing involves risk, including possible loss of principal.

Asset allocation and diversification may not protect against market risk, loss of principal or volatility of returns.

The BlackRock model portfolios are provided for illustrative and educational purposes only. The BlackRock model portfolios do not constitute research, are not personalized investment advice or an investment recommendation from BlackRock to any client of a third party financial professional, and are intended for use only by a third party financial professional, with other information, as a resource to help build a portfolio or as an input in the development of investment advice for its own clients. Such financial professionals are responsible for making their own independent judgment as to how to use the BlackRock model portfolios. BlackRock does not have investment discretion over, or place trade orders for, any portfolios or accounts derived from the BlackRock model portfolios. BlackRock is not responsible for determining the appropriateness or suitability of the BlackRock model portfolios, or any of the securities included therein, for any client of a financial professional. Information concerning the BlackRock model portfolios – including holdings, performance, and other characteristics – may vary materially from any portfolios or accounts derived from the BlackRock model portfolios. There is no guarantee that any investment strategy or model portfolio will be successful or achieve any particular level of results. The BlackRock model portfolios themselves are not funds.

The BlackRock model portfolios include investments in shares of funds. Clients will indirectly bear fund expenses in respect of portfolio assets allocated to funds, in addition to any fees payable associated with any applicable advisory or wrap program. BlackRock intends to allocate all or a significant percentage of the BlackRock model portfolios to funds for which it and/or its affiliates serve as investment manager and/or are compensated for services provided to the funds (“BlackRock Affiliated Funds”). BlackRock has an incentive to (a) select BlackRock Affiliated Funds and (b) select BlackRock Affiliated Funds with higher fees over BlackRock Affiliated Funds with lower fees. The fees that BlackRock and its affiliates receive from investments in the BlackRock Affiliated Funds constitute BlackRock’s compensation with respect to the BlackRock model portfolios. This may result in BlackRock model portfolios that achieve a level of performance less favorable to the model portfolios, or reflect higher fees, than otherwise would be the case if BlackRock did not allocate to BlackRock Affiliated Funds.

This material does not constitute any specific legal, tax or accounting advice. Please consult with qualified professionals for this type of advice.

Any information on funds not managed by BlackRock or securities not distributed by BlackRock is provided for illustration only and should not be construed as an offer or solicitation from BlackRock to buy or sell any securities.

This information is intended for use in the United States. This information is not a solicitation for or offering of any investment, product, or service to any person in any jurisdiction or country in which such solicitation or offering would be unlawful.

Investing in digital assets involves significant risks due to their extreme price volatility and the potential for loss, theft, or compromise of private keys. The value of the investment is closely tied to acceptance, industry developments, and governance changes, making them susceptible to market sentiment. A disruption of the internet or a digital asset network would affect the ability to transfer digital assets, and, consequently, would impact their value.

Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments.

International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation and the possibility of substantial volatility due to adverse political, economic or other developments. These risks often are heightened for investments in emerging/developing markets and in concentrations of single countries.

There can be no assurance that performance will be enhanced or risk will be reduced for funds that seek to provide exposure to certain quantitative investment characteristics (“factors”). Exposure to such investment factors may detract from performance in some market environments, perhaps for extended periods. In such circumstances, a fund may seek to maintain exposure to the targeted investment factors and not adjust to target different factors, which could result in losses.

Alternative investments present the opportunity for significant losses and some alternative investments have experienced periods of extreme volatility. Alternative investments may be less liquid than investments in traditional securities.

Actively managed funds do not seek to replicate the performance of a specified index, may have higher portfolio turnover, and may charge higher fees than index funds due to increased trading and research expenses.

Transactions in shares of ETFs may result in brokerage commissions and will generate tax consequences. All regulated investment companies are obliged to distribute portfolio gains to shareholders. Certain traditional mutual funds can also be tax efficient.

ETFs are obliged to distribute portfolio gains to shareholders by year-end. These gains may be generated due to index rebalancing or to meet diversification requirements. Trading shares of ETFs may also generate tax consequences and transaction expenses.

The information provided is not intended to be tax advice. Investors should be urged to consult their tax professionals or financial advisors for more information regarding their specific tax situations.

BlackRock is not affiliated with Kovitz Investment Group Partners or Invesco.

Prepared by BlackRock Investments, LLC, member FINRA.

©2025 BlackRock, Inc. or its affiliates. All rights reserved. BLACKROCK, ALADDIN, iBONDS, and iSHARES are trademarks of BlackRock, Inc., or its affiliates. All other trademarks are those of their respective owners.

iCRMH0425U/S-4426044