Municipal tobacco bonds are one of the largest, most liquid and best-returning sectors within the municipal high-yield bond market. Issued by 17 states, the District of Columbia, three U.S. territories and a handful of counties, senior lien tobacco bonds total about $32 billion in par amount outstanding. Their structure is securitized and sensitive to future cigarette consumption, requiring detailed modeling and forecasting to support investment decisions. Despite the headline risks regarding cigarette consumption declines, we see many tobacco bonds as an attractive source of yield.

Municipal tobacco bonds are secured by a claim on a perpetual stream of annual settlement payments owed from the U.S. tobacco manufacturers to the states. These payments result from the 1998 Master Settlement Agreement (MSA) between the then four-largest tobacco companies and 52 attorneys general. Under the terms of the landmark court settlement, the tobacco companies agreed to make annual payments to the states and to restrict many of their advertising practices, particularly those targeting young consumers. In return, the participating states and territories released the tobacco companies from past and future liabilities arising from tobacco-related health care costs. The MSA payments were set at approximately $9 billion per year across all 46 participating states, subject to annual adjustments for U.S. cigarette consumption, inflation and other variables. A number of states have since set up trusts with the settlement money, as well as securitized their share of the MSA payment, thus creating this municipal bond sector.

Tobacco bonds frequently make headlines, given the sensitivity of the MSA payment to the secular decline in tobacco consumption. Many of the bonds issued in the latter half of the 2000s were structured with high leverage, requiring annual cigarette consumption declines of less than 4 percent a year to repay fully. Since then, actual cigarette consumption has come in lower than those expectations, declining an average of 4.5 percent a year starting in 2006. While good for society and public health, this has led to rating agency downgrades and increased uncertainty of full repayment. According to our estimates at PIMCO, a large portion of these bonds can now withstand only about 3 to 3.5 percent in annual cigarette consumption declines for full repayment of principal at stated maturity.

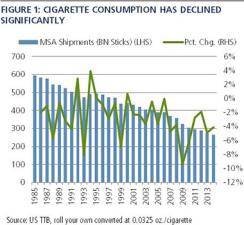

The most important factor affecting the stream of settlement payments under the MSA is U.S. cigarette consumption. Whereas the consumption decline averaged 2.8 percent a year between 1985 and 2014, declines have accelerated over time, with 1985 to 1995 averaging 1.8 percent, 1995 to 2005 averaging 2.5 percent and 2005 to 2014 averaging 4 percent (see chart 1).

Looking at the various historical drivers of U.S. cigarette consumption, PIMCO has found that the declining size of the U.S. adult smoking population, the price of cigarettes (including increased taxes), reduced disposable income and certain other factors have all had significant effects on cigarette smoking. These pressures have increased over time, culminating in the 2009 decline of 9.35 percent that coincided with a 62 cents-per-pack federal excise tax increase and the 2008–’09 financial crisis.

We forecast that cigarette consumption declines will exceed the historical average, and we assume that many of the pressures on the market segment, such as tax hikes and a decline in the number of smokers, will continue. Our forecast also gives credit to human ingenuity in finding new ways for people to quit, and to factors in negative network effects that tend to dissuade smoking, such as social stigma and smoking bans. Over the past decade, advances in pharmaceuticals and in alternatives like e-cigarettes have contributed to declines.

As mentioned earlier, many tobacco bonds require no more than 3 to 3.5 percent average annual consumption declines to fully repay. Therefore, they would likely default under our forecasts.

Wait, did you say default?

Yes. Municipal tobacco bonds can still be an attractive investment, however, because they behave differently from a typical corporate bond in a default scenario. For a typical corporate bond, assets are sold or debtor liabilities are reorganized, leaving the original creditor with a recovery claim. For a tobacco bond, if the tobacco trust does not have enough cash to pay interest and principal due, bonds remain outstanding and payments continue to be made from whatever tobacco settlement revenues are available. As a reminder: The settlement payments go on in perpetuity until the bonds are paid off or people stop smoking altogether.

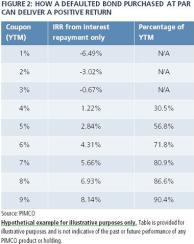

Whereas bondholders may not receive 100 percent of promised cash flows in a default scenario, our projections show they may receive a substantial enough sum to generate moderately attractive internal rates of return based on today’s prices (see chart 2).

Although tobacco bonds are more complex than this example, long-maturity 2007 vintage tobacco bonds have a current yield (coupon/price) in the 6 to 7 percent range, indicating that a large part of their promised yield-to-maturity comes from the coupon payments. We believe full interest payment is highly likely over the next decade, as this is before long-term bonds mature. The trust may still draw from a reserve sized at roughly one year of debt service. After default, tobacco settlement payments are divided pro rata among bonds to pay interest first and with any excess used to pay down principal. A 1 percent decline in settlement revenue each year is still enough in most cases to generate internal rates of return within 2 percent of the stated yield-to-maturity, despite full principal not being repaid.

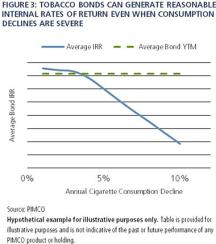

Municipal tobacco bonds offer relatively good cash flow returns, even in downside scenarios in which smoking declines are larger than expected. Whereas there are left-tail risks to cigarette consumption, broadly speaking, the MSA cash flow is relatively stable. Even under a consumption decline scenario of 6 percent a year, which is 50 percent higher than the average consumption decline over the past decade, bond cash flows drop by around 3 percent or less annually, given the inflation adjustment. It would take a very severe cigarette consumption decline for the cash flow internal rates of return to turn negative; investors therefore have some cushion (see chart 3).

As we do with all other investments, PIMCO forecasts expected cash flows under a variety of scenarios, gauges the risk associated with those cash flows and applies an appropriate discount rate to determine whether the market price of the asset is attractive. There are many different tobacco bonds, each with their own repayment schedule and likelihood of loss. With careful security selection and credit modeling, active management we believe can add a great deal of value in optimizing tobacco bond exposure.

David Hammer is an executive vice president and municipal bond portfolio manager in the New York office, and Steven Chuang is a vice president and credit analyst covering municipal credits in the Newport Beach, California, office; both at Pacific Investment Management Co.

Get more on fixed income.