Investors concerned that low nominal interest rates portend slow economic growth should take a look under the hood at the changing composition of nominal rates. Upon closer inspection, interest rates actually suggest we are experiencing a rather healthy environment for economic growth — and likely a good environment for risk assets.

Nominal rates in and of themselves don’t really tell us much about the economy. The components that make up nominal rates — real interest rates plus inflation — are much more insightful. To see how nominal rates can be a misleading economic indicator, consider stagflation. In such an environment, real rates will be low — that is, “stag” — but inflation will be high. These conditions can make it difficult to draw conclusions from the sum alone. Looking at the real interest rate and inflation components individually, however, gives a lot of information about where the economy is heading.

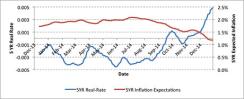

So what are nominal interest rates telling us today? First, rates are low, which could be a positive or negative, depending on the cause. At the moment, inflation is the culprit. Real interest rates, which are the true sign of economic growth expectations and ultimately will converge with real gross domestic product, actually have been steadily rising for the past six months, whereas inflation expectations, as proxied by break-even inflation, have been falling.

Chart 1: Recent Trajectory of Five-Year Real Rates and Inflation Expectations

The bond market is swapping inflation for real growth, a welcome trade-off. An environment in which the economy is growing with little threat of inflation — one we at Janus like to call a disinflationary boom — is the ideal type of economic growth.

Typically, there are two ways the economy can grow. Inflationary pressures can build, which causes prices to rise. This may look like economic expansion, but it’s just inflation. What we are seeing today is a market developing through productivity. This scenario is optimal because companies can generate cash flows and earnings without having to worry about the uncertainties of inflation and needing to hedge that inflation with higher prices. Such an environment leads to broad-based growth, rather than growth in only those industries that have pricing power.

Disinflationary boom periods like the one we are in now have historically been good for risk assets. As chart 2 shows, equities have typically performed best when real rates are high and inflation is low. To no one’s surprise, the worst environment for equities historically has been when growth surprises to the downside, and inflation to the upside, a so-called stagflationary period.

Chart 2: Return of the S&P 500 in Excess of Three-Month Treasury Returns

Note : Positive and negative surprises are defined as U.S. real GDP/CPI that prints higher and lower, respectively, than the consensus forecast. Consensus forecasts are sourced from the Survey of Professional Forecasters, available from the Federal Reserve Bank of Philadelphia. Data from 1982.

Investors should welcome the changing composition of nominal interest rates. If nominal rates were rising solely because of inflation, without any growth in real interest rates — the opposite scenario of what we’ve seen in the past six months — it would signal that we are likely entering a period of stagflation, which would be bad for the economy and financial markets alike.

It is very important to look into the components of nominal interest rates to get clues about the health of the economy. Nominal rates by themselves do not provide information on how real rates are moving relative to inflation. Nominal rates can only provide information about their sum. It is this relative movement between real rates and inflation that accurately characterizes the economy. This is truly a case in which the parts are much more valuable than the sum.

Ashwin Alankar, based in Denver, is senior vice president, head of asset allocation and risk management for Janus Capital Group and is co-manager of the Janus Global Allocation Funds.

Get more on macro.