Hard landing? Soft landing? No recession after all? As economic news that’s far rosier than most analysts expected to see this summer keeps coming in, a growing number of pundits are now openly wondering if the “severe downturn” long predicted to strike by late 2023 may turn out to be milder (and later in coming) than even the cheeriest of them had recently envisioned.

While a number of factors will contribute to the severity and timing of an eventual economic slowdown – or genuine recession, as a vocal cohort of market experts still believe one is inevitable – inflation’s path and US Federal Reserve activity are, naturally, among the most influential issues that any prognosticator must divine.

Should US inflation remain stubbornly high, or simply not fall quickly or sharply enough for the Fed’s taste, the latter might retain a more hawkish stance into 2024, further quelling economic growth by keeping interest rates higher – either by making more rate hikes than anticipated, or (perhaps a likelier scenario) by delaying or foregoing one of the rate cuts that most analysts now believe the Fed will start making early next year.

Morningstar is bullish on plunging inflation

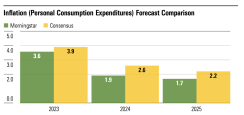

At the extremes, analyst opinions run the gamut from “move to cash now” pessimism to “perpetual growth is the new normal” optimism. But one of the most prominent economic research organizations recently made it clear that its sits decidedly past center on the sentiment bell curve, at least for now. In its US Economic Pulse report for June, Morningstar’s Chief US Economist, Preston Caldwell, notes that “we expect inflation to fall much faster than consensus.”Chart 1, which appears in the June report (as do all charts in this article), shows how Morningstar’s current forecast on inflation through 2025 compares to the consensus outlook.

Chart 1: Morningstar predicts US inflation to remain lower than market consensus is expecting to see over the next 2-plus years.

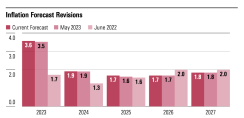

Chart 2: While a stronger US economy– and the expectation of a more hawkish Fed – has led Morningstar to slightly raise its inflation forecast through 2025, the company still expects inflation to plunge soon.

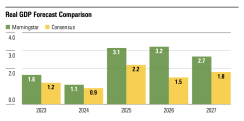

Long-term GDP outlook lower, but still strong

In his June report, which (along with the wider market) correctly anticipated that the Fed would raise the interest rate again in July (and it did so on July 26), Caldwell also makes it clear that Morningstar is “more bullish than consensus on long-run GDP.” And, as with its inflation forecast, this extra notch of optimism holds even though the company has actually lowered its long-term GDP outlook in recent months – in believing that the humming US economy will give it an initial boost (buoying 2023’s projection), but will then indirectly tamp down GDP growth over the next several years:Just how much more bullish is Morningstar on US economic growth than the current market consensus? As shown in Chart 3, the company expects to see “cumulative 5% more real GDP growth through 2027 than consensus.” As for near-term drivers, “the divergence is driven by our view that falling inflation will allow the Fed to cut rates and jump-start the economy,” Caldwell writes. Following this period, in the latter two to three years of the forecast, Morningstar has more optimism than analysts at large currently hold that “supply-side expansion, in terms of labor supply and productivity” will buoy GDP growth.

Chart 3: Morningstar predicts US economic growth will be stronger in the coming years than most analysts currently expect, especially from 2025 through 2027.

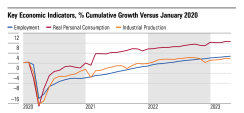

Economic measures have been surprisingly strong…

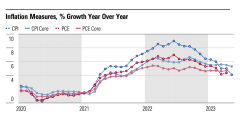

Caldwell notes in the June publication that most measures of US economic activity – including employment, real personal consumption, and industrial goods production – are either continuing to trend upward (especially job growth) or at least holding stable (as shown in Chart 4). This makes the recent nosedive in inflation (see Chart 5) all the more extraordinary. “It’s remarkable that inflation has already fallen so much while economic growth has remained resilient,” he writes, adding: Chart 4: Three vital measures of the US economy have kept trending upward or shown resilience since the depth of the pandemic…

…but expect a slowdown this year

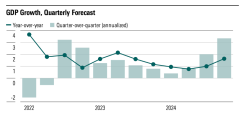

While Morningstar doesn’t believe a full recession is coming soon, Caldwell relays that the organization sees the “stronger momentum in the economy than we had anticipated” emphatically giving way to a deep slowdown in the remainder of 2023 and first half of 2024. “Rate hikes have had no impact on bank lending thus far, but that is set to change,” he says, adding that Morningstar expects consumers’ pockets to tighten soon, further dragging down growth:Chart 6 provides a quarterly view of Morningstar’s forecast for US economic growth, showing the weakening in the remainder of 2023 and rebound in 2024.

Chart 6: Morningstar expects US GDP growth to decline until early to mid 2024, given depleted consumer savings and other factors, but believes strong growth will then resume.

Look for the first rate cut in February

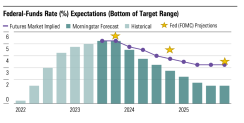

If the US economy markedly weakens in the next several months, as Morningstar predicts, the company sees the Fed making its first rate cut in February – which is in line with wider market expectations. However, Morningstar is more bullish than consensus on the decline of the federal-funds rate. Caldwell notes that the company forecasts that rate to drop from 5.25%-5.5% at the end of 2023 to about 1.5% by mid-2025 – which is roughly two points lower than the market’s (and the Fed’s) current expectations for the latter period (see Chart 7).

Chart 7: Morningstar forecasts a more significant drop in the federal-funds rate than the Fed through 2025.