For much of the past five years, investors have used one of two words to describe the market: precrisis and postcrisis. We at KKR Asset Management feel that the lines between the two descriptors have begun to blur.

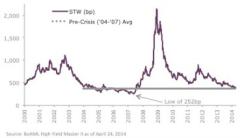

When spreads are nearing levels seen in 2005–’06, can we really talk about a postcrisis market? Or are the present economic conditions a precursor of the next financial meltdown? In fact, although we are still more than 100 basis points off the tightest spreads of the past 15 years, the Bank of America Merrill Lynch U.S. High Yield Master II index is hovering around the average spread seen between 2004 and 2007.

Since mid-2007, which, for the sake of argument, we will say was the peak of the last precrisis market, assets under management at high-yield funds have grown by more than $132 billion. The investment-grade market has almost doubled, adding more than $280 billion of assets, while the amount of levered loans outstanding over the same time period has grown by $154 billion. In total, that’s more than $560 billion of new demand from just these three sources. High-yield assets under management in funds has grown by 81 percent and investment-grade has grown by 196 percent since mid-2007. The dollar amount of loans outstanding has grown by 28 percent. The key, however, is the dollar amount of the growth. Much of the expansion in the loan asset class happened in 2004–’06.

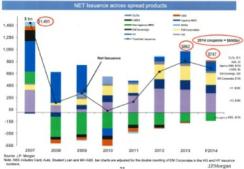

What’s more, there is a supply and demand imbalance across the system. There just aren’t enough assets to go around. Total net issuance of spread products is forecast to be $747 billion in 2014, according to investment bank J.P. Morgan. That would be about half of the net issuance in 2007. Consider that there is $668 billion of coupon income coming into the system from the same asset classes, and it is thus easy to see why there is such a bid for spread assets.

It’s true: We can’t help noticing the similarities between 2007 and 2014. Here are a few:

New issues. The exuberance of the 2007 market allowed for large-scale deals that pushed the amount of leverage accepted on a cap structure, including covenant-lite structures with aggressive ebitda add-back provisions, and that were done with peak-cycle earnings. Today, however, the aggressiveness in volume stems mainly from the size of the company coming to market and its ability to secure terms that befit big-market corporations. In the present market, less attractive companies are often first-time issuers that require more due diligence. These firms typically lack the secondary liquidity that should be necessary for many of these buyers, who include all types of investors.

Mismatch of assets and liabilities. In the last precrisis period, we saw a tremendous mismatch between assets and liabilities, as many investors used short-term mark-to-market leverage to boost their buying ability and returns. All this money needs to be put to work. Corporate credit has been the beneficiary.

Liquidity challenges. With this increased demand, getting enough of what investors want can pose a challenge. New-issue allocations are often a fraction of the order, and, when coupled with a limited ability to trade these securities in the secondary market, liquidity seems to be only one-directional. As we’ve seen over the past few years, reverse inquiry is a good way around the allocation situation, but even then, exit options can be limited.

In contrast to these similarities, there is one stark difference between 2007 and 2014: banks’ apparent inability to use balance-sheet capital. This doesn’t seem to be causing much of a hiccup for the time being. But when investors start selling, the lack of a natural buyer may only exacerbate market volatility.

Any similarities to the market conditions seen in 2007 notwithstanding, we do not think that a market reversal would be of the magnitude seen in 2008. For one, we believe that retail deposits would likely be less volatile than the leverage facilities that funded much of the 2007 market.

Second, we also feel better about the health of debt-issuing companies. We don’t think we are at peak ebitda for much of the market; in fact, we think there is room for improvement. A meaningful amount of operational leverage remains in the system. And although excessively high leverage ratios, limited cash flow and the probability of repayment were the concerns in 2008, there is now more of a question as to whether investors are being adequately compensated for the underlying credit profile. With the general consensus being that defaults may remain low for the near term, the primary concern is pricing.

Third, we think the tailwinds supporting credit are still strong. Aside from the robust inflows from pensions, insurance and other institutional markets, money flowed into loan mutual funds consistently for 95 weeks and only recently saw a first outflow. There have also been steady flows into high-yield bonds, except for a few weeks of money moving out in December 2012 and June 2013, spurred by rising interest rates. Everyone from individual to institutional investors is starving for yield. We believe high-yield bonds and loans are the fixed-income asset classes that offer attractive absolute yields.

This tailwind is still gusting. Demand is continuing despite recent regulations that have weighed on bank-lending practices and on the ability of collateralized loan obligations to grow their platforms. The U.S. Federal Reserve, the Federal Deposit Insurance Corp. and the Office of the Comptroller of the Currency set limits in March on acceptable levels of leverage on newly issued loans. These rules may limit the types of deals that make it to market, as they require CLO managers to hold 5 percent of a structure directly, which may restrict their ability to invest. If this happens, investors may be driven to other spread assets, edging that much closer to the peak of the next precrisis period. On the other hand, if the guidelines are just guidelines, rather than strict rules for enforcement, we expect the risk-on market to continue.

In markets like the present, we come across all sorts of situations that provide the opportunity to buy strong assets at decent prices. Whether there is an earnings miss, selling driven by flows from exchange-traded funds or a technical mismatch presented by an off-the-run bond, we’ll take a look at the asset. In the end, maintaining a solid grip on the market involves three key points: knowing our credits, doing our homework and only taking risk that is fairly compensated. In addition, investors should look at credit as a whole and not just focus on specific asset classes.

As the market begins to feel a bit choppier, we are yet again beginning to wonder what to call the present market. Whatever the term may be, we’ll stick to our fundamentals and invest with conviction.

Christopher Sheldon is the co-head of leveraged credit at KKR Asset Management in San Francisco.