The U.S. inflation-protected bond markets, primarily composed of Treasury Inflation-Protected Securities (TIPS), have been extremely turbulent in 2013 — with most of the volatility seen in May, June and July. In this piece, we look at the factors that contributed to these extremely sharp moves in TIPS prices and argue that present U.S. real rate valuations are near their most compelling levels in years.

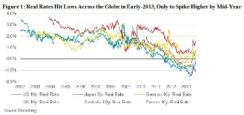

In an attempt to stimulate the economy in the aftermath of the 2008 financial crisis, the Federal Reserve lowered its target fed funds rate to between zero and 25 basis points and employed various programs such as quantitative easing (QE) and Operation Twist, which had the effect of pushing spot real rates to incredibly low levels by early 2013, before the sharp May-to-September reversal sent real rates higher (see chart 1). Not only did policy drive spot rates down at the long end of the curve, but it also pushed forward rates lower.

There are multiple ways to determine the value of fixed-income investments, and more specifically real rate–focused TIPS. Commonly used valuation methodologies involve comparing spot rates (such as five-year TIPS rates or ten-year TIPS rates for immediate settlement) with forward rates, or what markets imply the rate will be for a specified period of time, such as the real rate five years from now, extending for the next five years from then, commonly known as the 5y5y forward rate. This is the Fed’s favored measure for observing market-implied inflation expectations.

This past spring the 5y5y forward rate was just below 3 percent. That level does not seem like a stretch from a valuation perspective, given the central bank’s mandate, but to understand fully what it implies, we must examine its underlying assumptions. In order to generate a near 3 percent inflation run rate between 2018 and 2023, for example, one must assume that meaningful growth will have returned to the economy. Keeping that in mind, surely 5y5y real rates — the real rate between 2018 and 2023 — would reflect at least some of this optimism, but what were 5y5y real rates in April 2013? The answer is very close to zero and at times even negative.

From a macroeconomic policy standpoint, the inflation market in early 2013 was implying that the U.S. economy was likely to experience zero real growth from 2018 until 2023, while informing us that the inflation rate for the same time period would be almost 3 percent. That is either an extremely dire economic scenario — stagflation — or a tremendous job of market manipulation by monetary authorities. We think the latter is more likely.

How was it, then, that the central bank–inspired overvaluation of TIPS markets unraveled so dramatically in the summer of 2013? We believe that there were two main contributors to the sell-off. The first, and probably the lesser of the two influences, was a decline in the run rate of headline inflation going into the second quarter. The slowdown in inflation subsequently forced owners of inflation-linked assets to question the potential future returns from investments, given the extremely negative real rate valuations witnessed at the time. To use a very simple example, two-year TIPS yielded negative 2 percent in March 2013; if inflation did not run above a 2 percent average for the remaining life of that bond, then owners of that issue would suffer capital losses.

The second, more important factor behind the sharp move higher in real rates was the realization among market participants that the Fed would eventually slow the rate at which it purchases mortgage-backed securities and Treasury securities. The concept of tapering emerged in its full form in May, stemming from comments Fed chairman Ben Bernanke made in a congressional hearing, and it gathered further momentum as Larry Summers temporarily became the front-runner to take over the Fed’s top spot.

Lower risk-free real rates were a direct effect of QE. The threat of a slowing and potential cessation of Fed balance sheet expansion would certainly have ramifications for both real and nominal rate valuations, even if policy is to remain broadly accommodative, as we expect it will. Furthermore, the tepid run rate of inflation, combined with the liquidity differential between TIPS and nominal Treasuries, laid the foundation for a violent real rate sell-off, as market expectations of future policy accommodation were scaled back. Still, given the turbulent price action over the summer and the subsequent stabilization heading into fall, how do valuations look today?

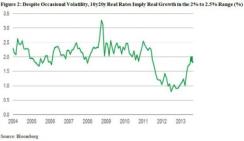

When we look at forward-rate valuations following the upward move in yield earlier this year, they look reasonably attractive relative to history— and extremely attractive relative to recent history — despite spot rates still being low on an absolute basis. Historically, long real rates have been a great proxy for long-term real growth, so when we look at 10y20y real rates — that is, 20-year rates, ten years into the future — in the context of a 2 percent level, it does not seem too far out of line with where this relationship has historically been. Further, if we look at chart 2, which displays this relationship from 2004 until today, we can see that apart from some volatility around 2008, and the lows in yields over the past 12 months as the Fed took duration out of the market with the various QE and Twist programs, this long-forward real rate measure has generally averaged between 2 percent and 2.5 percent, a reasonable level at which to expect longer-term real GDP growth to reside.

Additionally, an interesting point when considering long-term forward rates is to acknowledge what happened to these rates when the Fed last embarked on a tightening cycle, which took place from July 2004 until early 2006. During that period the Fed moved the funds rate from 1 percent to 5.25 percent, and long-forward rates actually dropped substantially. Granted, this decline was from higher spot rate levels than in the present environment. The proper valuation for these long-forward rates will ultimately be determined by expectations for future real economic growth. If anything, we believe growth expectations are biased lower in the postcrisis period, given the deleveraging process and the demographic headwinds that the U.S. and, to an even greater extent, the developed world as a whole are facing.

Given current valuations and a steep yield curve alongside the tailwinds of investor need for yield and potentially lower trend levels of growth in the U.S., we would thus look for opportunities to own long-forward rate exposures generally anytime they venture north of 2 percent. Granted, spot rate levels may still rise, but we believe that at the longer end of the curve, the bulk of the repricing from the severely repressive levels earlier in the year has already taken place, and investors should be looking for opportunities to build real rate exposures as opportunities present themselves.

The famed economist Milton Friedman was quoted as saying that monetary policy operates on long and variable lags. This line of thinking is where we think owning TIPS instead of nominal fixed income begins to make a lot of sense, as we are in the midst of a massive monetary policy experiment, and its long-term impact is unknown. We believe that within that context,one should be an accumulator of inflation insurance at current or lower valuations. Real rates may not appear outright cheap, but should another round of bond selling occur in the wake of forthcoming Fed tapering, it may offer a good opportunity to allocate to a fixed-income sector offering positive real rates of return, despite a cloudy outlook.

Martin Hegarty is a manager for BlackRock’s institutional multisector portfolios and is co-head of global inflation-linked portfolios.