Congressional appearances by the head of the Federal Reserve Board are usually occasions of false drama. Politicians posture about the state of the economy; journalists sit in rapt attention, waiting to pounce on any shift in nuance; but the Fed chairman sticks to a carefully honed script, eager to avoid any surprises. That’s especially the case for Ben Bernanke, whose hallmark transparency aims to enhance the Fed’s effectiveness by making its policy deliberations an open book.

But when Bernanke appeared before the Joint Economic Committee of Congress on May 22, he set off a firestorm with a single sentence. “In the next few meetings, we could take a step down in our pace of purchase,” he told the committee members. It was a clear signal that the Fed was preparing to wind down its quantitative easing program, an unprecedented series of bond purchases that has driven interest rates to record lows and stoked financial markets around the world over the past four years.

The reaction was immediate. Interest rates on the U.S. Treasury’s benchmark ten-year note spiked 9 basis points, a huge daily move, and have continued to climb, reaching 2.99 percent early this month, up a heady 1.33 percentage points from early May. The climb in U.S. rates has injected fresh volatility into financial markets and triggered the biggest flight of capital from emerging markets since the depth of the crisis, in 2009. Central banks from Brazil to India to Indonesia have hiked rates to defend their currencies. “Everybody is amazed by the reaction to the tapering discussion in the U.S.,” says one European central banker, who spoke on condition of anonymity.

Notably, all this turbulence resulted not from an actual tightening or even a threat of tightening but simply a hint that the Fed would soon taper its purchases and buy bonds in smaller volumes. As Bernanke himself told Congress in July, “A highly accommodative monetary policy will remain appropriate for the foreseeable future.” (See also why low rates and slow growth are likely to perist for years)

Click to enlarge |

Since the failure of Lehman Brothers Holdings in September 2008, the Fed has taken extraordinary measures to avert a modern-day depression and steer the U.S. economy back to health. Initially, the central bank provided tens of billions of dollars in credit to American International Group to prevent the insurer from going bust, launched massive loan facilities to unfreeze the U.S. money market and securitization markets, and slashed interest rates to zero for the first time in U.S. history. Later it embarked on a series of ever more ambitious bond purchase programs in a bid to drive down long-term rates and revive investors’ risk appetite, more than quadrupling its balance sheet in the process, to some $3.6 trillion. For Bernanke, a scholar of the Great Depression determined to avoid the Fed’s past mistakes, the central bank needed to rewrite its policy playbook to confront such dire circumstances. (Read more: “The New Art of Central Banking”)

The Legacy of Lehman: A Look at the World 5 Years After the Financial Crisis

- 5 Years After Lehman, No One Can Declare the Financial System Safe

- Europe's Banks, Slow to Restructure, Pose a Systemic Risk Today

- Emerging Markets Face Mounting Challenges as Global Liquidity Dries Up

- China Exploits Crisis, Positions Renminbi as Potential Rival to Dollar

Now the Fed faces daunting challenges as it weighs an exit from unconventional monetary policies. The U.S. has bounced back better than most advanced economies, but the recovery remains tepid by historical standards, held back by consumer deleveraging and the fiscal drag from budget-cutting federal and state governments. No one knows for sure whether the economy can withstand significantly higher rates. Mortgage applications have fallen in recent weeks, a potential signal of weakness in the housing market, following a 1-point rise in mortgage rates since May. A relapse into recession with monetary policy virtually exhausted would be a nightmare scenario akin to Japan’s long stagnation.

“Going back into recession would be really difficult at this juncture. Europe has really shown that,” James Bullard, president of the Federal Reserve Bank of St. Louis, tells Institutional Investor. “They’ve got years of repair ahead of them. We certainly do not want to get into that situation.”

Delaying an exit carries dangers too. The Fed’s policies, combined with similar monetary easing by the Bank of England, Bank of Japan and European Central Bank, have pushed investors to load up on risk in a bid to maintain returns. Skeptics fear this creates more costs than benefits. In a noteworthy speech in February, Fed governor Jeremy Stein pointed to surging issuance of junk bonds, convenant-lite loans and U.S. agency mortgage real estate investment trusts as evidence of “a fairly significant pattern of reaching-for-yield behavior” that could pose a threat to financial stability. In the view of many Fed watchers, Stein’s warning strengthened the anti-QE camp inside the Federal Open Market Committee and tilted the balance toward an earlier exit. “The committee is itching to taper,” says Laurence Meyer, co-founder of Washington-based research firm Macroeconomic Advisers and a former Fed governor.

So the stakes will be high when the FOMC meets on September 17 and 18. Although Fed officials have stressed in recent weeks that any decision will depend on economic data, most analysts believe the policymaking committee will decide to taper bond purchases then, or at the latest at the committee’s December meeting. Managing the shutdown of the Fed’s massive liquidity spigot without crashing financial markets and the global economy will be a delicate task that will keep investors on edge well into 2014.

Click to enlarge |

Many financial market participants are less sanguine. They worry that the recent rise in U.S. rates and volatility in global markets offer a foretaste of the turmoil to come when the Fed actually begins to exit from QE. “We’ve never seen a policy like this, so it’s difficult to imagine what the result of going back to a market pricing system will do,” says James O’Shaughnessy, chairman, CEO and CIO of O’Shaughnessy Asset Management, a Stamford, Connecticut–based quantitative firm that manages $5.6 billion. He predicts that long-term U.S. rates will revert to their post–World War II average of 7 to 7.5 percent over the next five to ten years.

“We are nervous,” says Ben Inker, head of asset allocation at GMO, a Boston-based manager with $108 billion in assets. “We own less in stocks and less in bonds because we are afraid rates might have to come up in a quicker and less well-choreographed manner than the market is pricing in.”

Others see the U.S. economy as too fragile to support sharply higher rates, especially if other shocks arise, such as a flare-up of Europe’s debt crisis or a sharper slowdown in China. Could ten- year yields fall back below 2 percent? “I’m betting on it,” says John Makin, a resident scholar at the American Enterprise Institute and former chief economist at Caxton Associates.

Whatever the outlook, investors can count on greater market turbulence going forward. Aggressive action by the Fed and other central banks has intentionally depressed volatility; it is bound to return as monetary authorities pull back. Recent jumps in rates after the release of strong U.S. employment figures offer a hint of what’s to come. “We’re actually going to get back to a world where economic data is very important,” says Russel Matthews, a portfolio manager at BlueBay Asset Management in London.

Fed officials have tried to calm market jitters by stressing that any move to reduce bond purchases will be gradual and that the central bank is unlikely to begin raising interest rates before the second quarter of 2015. They believe the commitment to maintain zero rates well into the future, known as forward guidance, should limit the rise in long-term market rates during the tapering period. But guidance isn’t foolproof. Mark Carney, the new governor of the Bank of England, introduced the strategy in the U.K. last month, when the central bank’s Monetary Policy Committee promised to keep its short-term rate at 0.5 percent until unemployment falls to 7 percent. U.K. interest rates rose sharply that day, however.

“I don’t think guidance really does very much,” says Charles Goodhart, director of the financial regulation research program at the London School of Economics and Political Science and a former member of the MPC. “The market’s always going to be a bit cynical, assuming it’s just words.”

As if the Fed’s challenge isn’t tough enough, the central bank will make its pivotal policy decision at a time of unparalleled speculation over its leadership. With Bernanke due to depart in January, when his second four-year term expires, Washington has been transfixed by the succession race between Lawrence Summers and Janet Yellen. Fed watchers believe President Barack Obama will announce his nominee shortly after the September FOMC meeting to dissociate the new head from the decision to taper. In his few comments about monetary policy, Summers has been much more skeptical about the benefits of QE than Yellen, one of the Fed’s leading doves. If Summers gets the nod for chairman, investors may well anticipate a somewhat more hawkish stance by the central bank and push up market rates faster than if Yellen was chosen.

“Any time you change any member of the committee, you’re going to change the credibility of the forward guidance,” says Adam Posen, head of the Washington-based Peter G. Peterson Institute for International Economics and a former member of the MPC. “If you change who’s talking, it changes the message.” (See also “Investors Hampered by Sovereign Debt and Political Uncertainty”)

THE FED’S UNCONVENTIONAL POLICIES, like those of other central banks, are a response to extraordinary economic strain. The U.S. recession of 2008 and ’09 was the most severe since the Great Depression and the recovery the weakest. The unemployment rate stands at 7.3 percent, down from the recession peak of 10 percent, in good part because many people have dropped out of the labor market. There are 2 million fewer people on nonfarm payrolls today than at the start of 2008.

Unable to cut interest rates any further, the Fed launched its quantitative easing policy in November 2008, saying it would buy $600 billion of mortgage-backed securities and agency bonds, an amount it later upped to $1.75 trillion. It launched a second round of QE two years later, buying $600 billion of U.S. Treasuries. With the economy still sluggish and inflation below target, in September 2012 the Fed embarked on an open-ended commitment, dubbed “QE infinity,” to buy $40 billion of mortgage-backeds a month until there was “substantial improvement” in the labor market. In December it tacked on an additional $45 billion a month of U.S. Treasury purchases and promised to maintain the federal funds rate at its target level of zero to 0.25 percent until unemployment fell to 6.5 percent, provided inflation remained under control.

That message sent a strong easy-money signal to financial markets, and the S&P 500 went on a tear, rising more than 23 percent between mid-November and mid-May. The guidance seemed to resolve the Fed’s exit dilemma by tying policy to discrete economic objectives. If the economy and unemployment improved, the Fed would start dialing back its purchases.

Yet disquiet over QE was brewing even as the Fed embarked on its biggest bond-buying spree ever. Several regional Fed presidents — including Richard Fisher in Dallas, Esther George in Kansas City and Jeffrey Lacker in Richmond, Virginia — expressed worries that the Fed was distorting markets and fueling future inflation pressures by buying so many bonds. Governor Stein drew attention to broader risk concerns with his February speech. The International Monetary Fund and the Bank for International Settlements chimed in with warnings that the Fed’s unprecedented easing ran the risk of igniting inflation and fostering new asset bubbles. In financial markets volatility and the term premium between short- and long-term rates plumbed new lows, worrying even Fed doves.

“There’s a huge amount of uncertainty about how this prolonged period of low rates may be stoking up risks,” says Karl Habermeier, assistant director in the IMF’s monetary and capital markets department.

Doubts about the efficacy of QE were also growing. Proponents contend that the policy stimulates the economy through portfolio rebalancing as investors shift from Treasuries into riskier assets and by signaling that monetary policy will remain accommodative, which helps bring down long-term rates critical to the housing market and business investment. Economists struggle to quantify the precise impact, though. In a speech at the Kansas City Fed’s August 2012 symposium in Jackson Hole, Wyoming, Bernanke cited several Fed studies that showed that quantitative easing by that stage had reduced ten-year Treasury yields by 80 to 120 basis points, boosted economic output by 3 percentage points and increased employment by more than 2 million jobs. In August 2013, however, a study by Fed economists Vasco Cúrdia and Andrea Ferrero estimated that the second round of QE had reduced long-term market rates by just 13 basis points, or less than the usual impact of a quarter-point cut in the fed funds rate.

When Bernanke went before Congress in May and hinted at a tapering of bond purchases, his suggested timetable — starting this autumn — matched the expectations of the primary dealers in the government bond market that the New York Fed surveys. The Fed chairman wanted to signal an impending shift in stance and blow some froth off the markets, but he didn’t want to trigger a sharp rise in rates that could hurt the recovery. The market reaction was greater than he expected, Fed insiders acknowledge. Yet at the FOMC meeting in June, the committee agreed that Bernanke should provide more-explicit guidance about the exit path from QE. At his subsequent news conference, the chairman told reporters that the Fed was likely to start reducing its bond purchases later this year and end them by the middle of 2014, when FOMC members expect unemployment to have fallen to about 7 percent.

The reaction was immediate: The bond market slump turned into a rout. Over the next five days, yields on the ten-year Treasury note leaped 40 basis points, to 2.6 percent.

By signaling that the central bank expected to begin tapering in September even as most private forecasters — and FOMC members — were lowering their projections for U.S. growth, Bernanke suggested that dates, not data, were driving Fed policy. Such reasoning prompted the St. Louis Fed’s Bullard to dissent from the FOMC decision. “We were taking an action that would be viewed by markets as more hawkish at a meeting where we were downgrading our expectations for growth and inflation in 2013,” he says.

For many analysts the episode represented a major gaffe for the Fed’s vaunted communicator-in-chief. “He screwed it up. We had so much confusion in the market,” says the AEI’s Makin.

The incident also cast doubt on the way QE works and the Fed’s ability to use forward guidance to contain the rise in market rates as it tapers its bond buying. Bernanke and other Fed officials contend that the central bank’s multitrillion-dollar stockpile of bonds has a bigger impact on rates than its monthly purchases, and it intends to maintain that stock even as it winds down its monthly inflows. And even in the most likely taper scenario, the Fed would buy nearly $500 billion worth of bonds between now and mid-2014, nearly as much as the $680 billion purchased in the first eight months of 2013.

Many outside analysts, however, say the flow of purchases affects the markets much more than the stockpile because of the signal it sends about future Fed policy. The severe market reaction of May and June suggests the flow view is correct. If so, the Fed may find it difficult to calm financial markets with talk — wrapping the taper in a dovish package of forward guidance, as Morgan Stanley’s chief U.S. economist and former Fed staffer Vincent Reinhart puts it. “It underlines how difficult the [tapering] exercise is likely to be,” says the LSE’s Goodhart.

The recent confusion has made Fed officials warier of potential market reactions but hasn’t altered the calculus of the taper decision, people close to the central bank say. “It was kind of a minitest,” says Donald Kohn, a former Fed vice chairman whom Obama has cited as a possible candidate to succeed Bernanke. “Markets went through it. Interest rates rose. I didn’t see any threats to financial stability.”

Recent economic signals have been mostly positive. The U.S. economy grew at a revised pace of 2.5 percent in the second quarter, up from 1.1 percent in the first. Growth in nonfarm payrolls slowed in August, but gains have averaged 184,000 a month since the Fed began its latest round of QE, up from 139,000 previously, and could be deemed to pass Bernanke’s test of a substantial improvement in the labor market. “The underlying resistance of the private sector is really, really good,” says Macroeconomic Advisers’ Meyer. “We’re poised to move to a higher gear.”

In the Fed’s ideal scenario, a strengthening economy will enable it to gradually remove accommodation, then slowly start to raise interest rates from the zero bound where they’ve been locked for the past five years. That’s essential to restoring markets to a healthy equilibrium and ensuring that the Fed has ammunition to deal with a future recession when it inevitably comes.

Most of the seven Fed governors and the presidents of the 12 regional Fed banks expect to begin raising interest rates in 2015, with the fed funds rate ending the year at about 1 percent. In the longer run they see the fed funds rate getting back to a so-called normalized level of about 4 percent. Such a policy rate would imply yields on ten-year Treasuries moving up to about 5.5 percent, or roughly 2.5 percentage points above current levels, says Morgan Stanley’s Reinhart. “That’s going to be painful. It’s going to be a real-time stress test of our financial system.”

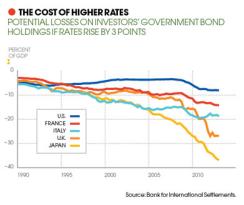

Consider the potential losses to investors. If yields were to rise by 3 percentage points across the U.S. Treasury yield curve, investors (excluding the Fed) would suffer losses of more than $1 trillion, or nearly 8 percent of U.S. gross domestic product, according to the Bank for International Settlements (see chart, page 61). For other countries losses from a similar rise in rates would be even more daunting: roughly 15 percent of GDP in France, 25 percent in the U.K. and 35 percent in Japan. The untold billions in low-rate bonds issued by corporations in recent years would take a hit. An investor who bought Apple’s 30-year, 3.85 percent bonds at the end of April is already nursing losses of more than 17 percent.

Rising rates would also deal a blow to banks. In March, U.S. banks were sitting on unrealized gains of $33.3 billion on their available-for-sale securities portfolios as Fed-induced declines in market rates increased the value of those positions. By July, after the rise in rates generated by the taper talk, banks had unrealized losses of $5.7 billion on those same securities positions.

A return to a normalized yield curve would involve a much larger increase in rates than the recent climb and could have far greater repercussions. Says one senior regulator, “There’s a significant risk that there could be a lot of market turbulence that central banks are not going to be able to control very easily.”

The turbulence would extend well beyond American shores. “The spillover into other economies is probably going to be large,” says Jan Hatzius, chief U.S. economist at Goldman Sachs Group. “The U.S. is still the center of the financial system. A lot of emerging-markets countries are pretty dependent on capital flows from the U.S.”

Market turmoil could also affect other developed countries. After a long period in which the major central banks pursued complementary policies, the Fed is now poised to begin tightening its credit stance at a time when the Bank of England, the Bank of Japan and the ECB are maintaining an easy posture. The European banks have adopted forward guidance of their own in recent months in a bid to insulate themselves from rising U.S. rates. That isn’t working too well for Carney’s Bank of England, as growing signs of economic strength are pushing up rates in the U.K., but ECB officials note that yields on German Bunds have lagged the recent rises in U.S. Treasury yields and that spreads in the euro area’s periphery haven’t widened. “The euro area is relatively sheltered,” says one European central banker. “The spillovers are not worrisome.” (See also “Growing Risks to U.S. Credit Rating and the Dollar”)

“We are going to see more and more desynchronization,” says Eric Chaney, chief economist at Paris-based insurer AXA. “The euro area has a lot of structural problems, which justifies keeping rates low for a much longer period than in the U.S.”

To be sure, focusing solely on the risks of monetary tightening gives a one-sided picture. If rates increase in an improving environment in which companies are creating jobs and incomes and earnings are rising, the economy should be able to cope. David Rosenberg, an economist at Gluskin Sheff and Associates in Toronto, notes that the Fed was able to raise rates from 2003 to 2006 without aborting that recovery, notwithstanding the lingering effects of the tech stock crash and the collapse of Enron Corp. “Typically, the economy is doing better when interest rates are on the rise,” he says.

The Fed also stands ready to intervene again if the economy flags. Bernanke insisted in his June news conference that tightening was “predetermined” and that the central bank could ease off on its tapering or even ramp up bond purchases again if economic conditions required.

How does this leave markets? Nervous and prone to sharp movements. “The minute the Fed stops doing what it’s doing, you’re going to see a pretty significant upward move in interest rates,” predicts fund manager O’Shaughnessy. He believes U.S. rates could spike an additional 100 basis points after the Fed starts to taper, heightening the risk of recession. On the other hand, he adds, “if we get to a 3 percent growth rate, rates could go up and do no harm to the economy and the stock market.”

The Fed and its extraordinary monetary policies are about to face the ultimate test. As GMO’s Inker puts it: “The economy used to be able to survive higher rates. If it can’t now, we’ve still got a lot of work to do.” • •

The Legacy of Lehman: A Look at the World 5 Years After the Financial Crisis

- 5 Years After Lehman, No One Can Declare the Financial System Safe

- Europe's Banks, Slow to Restructure, Pose a Systemic Risk Today

- Emerging Markets Face Mounting Challenges as Global Liquidity Dries Up

- China Exploits Crisis, Positions Renminbi as Potential Rival to Dollar