"Hands up if you know someone who’s a bullshitter.”

Jamie Dimon, chief executive officer of JPMorgan Chase & Co., stood unsmiling before a class of 300 new analysts in a conference room at the Madison Avenue headquarters of the firm’s investment banking division. The analysts stared back in silence, seemingly confused. It was September 13, 2011. Markets were beginning to stabilize after a volatile summer that had seen Europe’s debt crisis spread to Italy and Spain and the U.S. lose its triple-A credit rating. Occupy Wall Street, the messy affair that would take root in lower Manhattan’s Zuccotti Park, was still four days away.

“You know — a bullshitter,” Dimon continued. “Someone who cheats on their tax forms, who gets dinner delivered to the office when they don’t need to be there. We all know one.” First one, then two, then a small forest of arms was raised in agreement. Yes, the analysts — including myself, then a new JPMorgan recruit — all knew a bullshitter. “Right,” Dimon continued. “Now hands up if you’re a bullshitter yourself!” More silence. No hands went up. Dimon, prowling at the front of the auditorium, did not approve. “There are probably a couple of you in here who are bullshitters. If you’re a bullshitter, you should leave now. We don’t want you.”

A year later the swagger that Dimon put on display that morning had all but disappeared. Complex derivatives trades made in early 2012 by JPMorgan’s chief investment office, supposedly to hedge risk, had racked up losses of more than $6 billion. Two of the traders involved have since been charged with wire fraud and conspiracy to falsify books. Despite haranguing his trainee analysts on the evils of deception, Dimon had apparently been blind to such behavior within his own firm.

“The reason the London Whale story was so compelling was that here was an institution that was supposed to be the best-operated bank on Wall Street,” says Phil Angelides, who chaired the U.S.’s Financial Crisis Inquiry Commission from 2009 to 2011. “But it turned out that even the best-managed institution on the Street couldn’t monitor or control its own exposures or even adhere to its own internal risk parameters.” Excessive risk-taking was one of the key accelerators of the cocktail of deregulation, lax underwriting and leverage that led to the financial crisis. But risk remains a persistent feature of the postcrisis world. And as Jamie Dimon can no doubt attest, it is an exceptionally difficult beast to control.

The Legacy of Lehman: A Look at the World 5 Years After the Financial Crisis

- Europe's Banks, Slow to Restructure, Pose a Systemic Risk Today

- Emerging Markets Face Mounting Challenges as Global Liquidity Dries Up

- As the Fed Readies to Taper, Is the World Ready for Higher U.S. Rates?

- China Exploits Crisis, Positions Renminbi as Potential Rival to Dollar

Five years after the collapse of Lehman Brothers Holdings precipitated the worst financial crisis since the Great Depression, is the world any safer? The question defies an easy answer. Governments in the U.S. and Europe have drafted new laws, such as the Dodd-Frank Wall Street Reform and Consumer Protection Act, that broaden the scope of regulation to areas such as credit default swaps and give authorities new powers to resolve troubled institutions. Global regulators have imposed substantially higher capital requirements on banks to strengthen their ability to handle losses. New institutions, such as the Financial Stability Oversight Council in the U.S. and the Financial Policy Committee in the U.K., have been created to monitor systemic risks and — officials hope — nip future problems like the subprime crisis in the bud. (See also “The Ponzi Nation Topples”)

“The state of readiness to deal with threats to systemic financial stability is far greater today than it was in 2008,” asserts Mary Miller, the U.S Treasury’s undersecretary for domestic finance, who oversees the department’s work on financial stability.

Yet the changes shouldn’t leave anyone feeling particularly safe. Consider the banking system. Western governments spent hundreds of billions of dollars to prop up the system with capital injections, deposit guarantees and outright nationalizations, in some cases imperiling their own health to do so. But today the big banks are even bigger than before, and new, untested mechanisms designed to allow the authorities to resolve failed banks have convinced few in the markets that the days of bailouts are over.

Big chunks of the new regulatory infrastructure remain incomplete. The U.S. was the source of the crisis and has been at the heart of the response. Dodd-Frank contains the most comprehensive suite of reforms adopted by any government, ranging from overhauling the securitization process to bringing over-the-counter derivatives onto clearinghouses to creating a new consumer protection apparatus. Yet three years after Congress enacted the law, only 40 percent of its rules have been completed, according to Bart Chilton, who has sat on the Commodity Futures Trading Commission since 2007. The five main U.S. regulatory agencies charged with implementing the law were supposed to finish the job two years ago but are still struggling to write the myriad detailed rules required to make it effective. “Regulators by and large should have done much better,” Chilton says. (See also “Bankers in a Bind”)

In the meantime, the market is innovating in ways that may render many of the rules obsolete. One example comes from the swaps market. As the CFTC has strained to develop rules for swap execution facilities — the exchangelike platforms that are intended to bring transparency and clarity to a previously opaque OTC market — exchanges such as CME Group and IntercontinentalExchange have offered hybrid “swap futures” products that, in broad terms, reproduce the economic relationship of a swap at a fraction of its price. These products promise to shift risks previously associated with swaps into a new vehicle. Business is booming, with the CME clearing more than 100,000 in August, up from 30,000 in December, the month it launched the contract. Regulators are now engaged in a mad dash to catch up, with the CFTC and the SEC scrambling to finalize their swaps rules. (See also “New Rules, Old Risks”)

Click to enlarge |

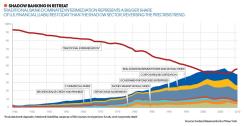

The broader shadow banking system, moreover, remains a major source of risk to financial stability. This network of lightly regulated vehicles, including repurchase agreements and money market mutual funds, provides the short-term funding that lubricates the wholesale financial markets. Shadow banking played an instrumental role in the crisis: A run by institutional investors on short-term bank debt, mainly in the form of repos and commercial paper, threatened to bring the financial system down after Lehman’s failure. Today the shadow system is nearly as large as it was before the crisis, and regulators have struggled to rein in risk. Last year the U.S. Securities and Exchange Commission had to abandon a major reform proposal for money market funds in the face of industry opposition; it’s unclear whether the agency will succeed in its current effort to adopt a watered-down proposal. Market participants face a looming collateral shortfall that could disrupt wholesale markets. And technology poses as much peril as promise to financial institutions, judging by the latest snafu, which shut down the Nasdaq Stock Market for several hours in August.

The picture, critics say, is far from reassuring. “We’ve preserved and in many ways made significantly worse a very broken financial system dominated by a handful of financial institutions that have grown too large and too systemically significant,” says Neil Barofsky, former special inspector general for the $700 billion Troubled Asset Relief Program and now a senior fellow at the Center on the Administration of Criminal Law at the New York University School of Law. “And the bad incentives that were in place prior to the crisis have been made more significant and severe. We haven’t done anything to solve that — and unless we do, we’re still on the pathway toward the next crisis.” (See also “Can Finance Be Fixed?”)

AS MAJOR COUNTRIES HAVE TIGHTENED capital requirements through the Basel III accord, big banks have pushed back. If standards are raised too high, they contend, banks will have less capacity to make loans, causing the economy to slow and financial risk to move into less tightly regulated entities, such as hedge funds and clearinghouses, that make up the shadow banking system. To date, however, there’s no evidence that raising capital has constrained lending or created new risks. Mutual funds have provided a substantial increase in credit to the U.S. high-yield corporate sector in recent years, says Tobias Adrian, head of capital markets research at the Federal Reserve Bank of New York. “There is nothing inherently unstable about this,” he says. Private equity funds and hedge funds have also stepped into the credit space more prominently, he adds, and because these funds are generally required by the very banks that lend to them to be well capitalized, no single fund constitutes a systemic risk to financial stability.

Yet shadow banking remains a primary concern of most observers. Size explains part of the preoccupation: Although the shadow banking system has shrunk somewhat since the crisis, reflecting a decline in securitization, it still accounts for nearly 40 percent of all liabilities in the U.S. financial sector, or $14.6 trillion, according to the New York Fed (see chart, page 52). Liabilities of commercial, federally insured banks, by contrast, are less than $17 trillion.

Given the short-term nature of the obligations in shadow banking, where credit is typically extended overnight in exchange for collateral, these institutions are inherently vulnerable to shocks and pose a risk to the broader financial system. The 2008 crisis intensified dramatically when the Reserve Primary Fund money market mutual fund could no longer guarantee to redeem its investors at 100 cents on the dollar because of its holdings of Lehman Brothers commercial paper. By breaking the buck the fund sparked a massive run on money market funds that threatened to starve corporate America of liquidity; only emergency federal insurance forestalled disaster.

Five years later there is still no federal backstop for any part of the shadow banking system, nor is there adequate supervision of the various institutions that constitute it, says Adrian. Many of these vehicles, including money market funds and agency real estate investment trusts, are overseen by the SEC, but the thrust of that oversight is aimed at consumer protection. “These entities are not subject to direct prudential supervision,” he says.

Efforts to close that gap on money market funds have yet to succeed. Former SEC chairman Mary Schapiro proposed requiring funds to hold capital to meet redemption requests and let their net asset values float rather than fixing them at $1 a share, but in spite of strong backing from Federal Reserve chief Ben Bernanke and then–Treasury secretary Timothy Geithner, her idea was torpedoed by strong lobbying from the fund industry. The new SEC chairman, Mary Jo White, is making another stab at reform with a watered-down proposal that would require only institutional money funds to adopt floating asset values. To prevent runs, it would also require funds to delay withdrawals or impose a 2 percent fee on them during a crisis. The SEC’s five commissioners will make a final decision after a public comment period, but even if the rule is passed, its implementation may be years away.

Derivatives, the instruments that brought down insurer American International Group in 2008, also continue to pose big risks. This giant market, with a total notional value of more than $630 trillion, dwarfs every other securities market on the planet. The broad thrust of postcrisis reform has been to shift swaps from an over-the-counter model to a centrally cleared model: The risk that formerly existed between two counterparties, usually dealer banks, on opposite sides of a swaps trade will now be warehoused in a central clearinghouse. This institution sits in the middle of a trade, becoming the seller to a buyer and the buyer to a seller, and demands collateral from those parties to back the deal. Most of the main clearinghouses, such as CME, ICE and London-based LCH.Clearnet, have been designated systemically important financial market utilities. They are already starting to see a dramatic rise in volumes. CME, which cleared virtually no swaps four years ago, did $1 trillion of business last year and had cleared almost $6 trillion in the first eight months of 2013. LCH.Clearnet, the world’s largest interest rate swaps clearinghouse, handled almost $12 trillion in notional value last year.

Most analysts agree that bringing swaps onto a centrally cleared platform represents an improvement on the precrisis trading model. The problem, for some, is the status of the clearinghouses themselves. “We are creating via clearinghouses new too-big-to-fail institutions,” says Manmohan Singh, senior financial economist at the International Monetary Fund. Dodd-Frank gives the largest clearinghouses access to the Federal Reserve’s discount window in “unusual or exigent circumstances.” Moral hazard may have a new home.

Clearinghouses themselves bristle at that suggestion. “Clearinghouses are in a much more highly scrutinized position than any other actor in the financial universe,” says Christopher Edmonds, president of the clearinghouse at ICE. The CFTC, the SEC and the Fed all have a say in the regulation of clearing. The capital and default cushions are thick: Large houses are required to hold enough capital to cover 12 months of operational expenses and to establish a default fund sufficient to cover the failure, at any given time, of the clearinghouse’s two biggest clients and those two counterparties’ top three positions. Clearinghouses are required to draw up a living will spelling out the precise order in which losses will be met and mutualized across clearing members.

No one knows how well these mechanisms will work in a crisis, though. “The failure of a large clearing member or the failure of a whole clearinghouse will not be an orderly process,” says the IMF’s Singh. “It will be messy, chaotic and disruptive.” Singh also worries that clearinghouses will lower their risk mitigation standards — either by lowering fees, accepting lower-grade collateral or cutting margin requirements — in a bid to win market share. Such efforts could introduce new channels of back-door risk into the financial system.

Kimberly Taylor, president of CME Clearing, dismisses the idea of a race to the bottom. Regulators set risk parameters, and institutions have no reason to try to skimp on margin or collateral, she says: “Safety and soundness are what clearinghouses provide to the marketplace — it’s the good we sell. We don’t want to reach the point of exigent circumstances.”

The move to clearinghouses highlights the problem of unintended consequences. In their drive to bolster the resilience of derivatives markets, European and U.S. regulators have focused on the need to post more liquid, high-quality collateral to backstop trades. Industry projections suggest that the world may need an additional $4 trillion to $5 trillion in collateral if regulations are finalized in their current form. That may well outstrip the available supply. The Fed, the Bank of England and the Bank of Japan have removed trillions of dollars’ worth of high-quality assets from the markets with their bond-buying programs. Even worse, the IMF estimates that sovereign credit rating downgrades could cut the supply of good collateral by as much as $9 trillion by 2016.

Market participants could respond to this collateral shortfall in a number of ways. They could withdraw from the derivatives market and leave their underlying investment positions unhedged, or they may try to cobble together imperfect hedges through the futures market, where collateral requirements are generally less expensive. As a result, the IMF’s Singh says, “you’ll end up introducing bubbles of financial risk into the system.”

In an alternative scenario investment banks and custodians may seek to fill the breach and provide so-called collateral transformation services. These institutions could act as intermediaries, taking high-quality assets from market participants that have them in abundance — such as pension funds, foundations and other risk-averse institutional investors — and lending them to players needing collateral in exchange for less-liquid assets such as equities or corporate debt. For the investment banks such business represents a potentially lucrative opportunity. For the broader system, though, such chains of intermediation between long-term institutional investors and risk-hungry actors like hedge funds and proprietary trading firms could become vulnerable during periods of market stress. Collateral transformation could be a catalyst for the next crisis, much like maturity transformation — using short-term borrowings to finance long-term investments — was in the last one.

“If the system gets more interconnected, especially through collateral transformation to supply the requisite collateral to clearinghouses, then you are making the shadow banking world more accessible to taxpayer bailouts,” Singh contends.

The banks, for their part, assert they are bolstering their ability to meet these new risks. Capital strength has improved substantially. In March the Federal Reserve announced that all but two of 18 large U.S. banks had sufficient levels of capital to withstand severe stress. European banks have begun to catch up in this area, with the U.K.’s Barclays and Germany’s Deutsche Bank making or announcing large share issues in recent months. And capital buffers are moving in a more, not less, stringent direction: The Basel Committee on Banking Supervision, seeking to prevent banks from gaming its capital rules by manipulating asset risk weights, is in the process of adopting a new leverage ratio that requires banks to hold capital equal to 3 percent of total assets. In a recent discussion paper, the committee suggested that it was open to reconsidering its reliance on banks’ own internal risk models in determining capital requirements.

Institutions have also ramped up their risk management efforts. Consulting firm Deloitte reported that in a recent survey 65 percent of financial institutions said they had increased their spending on risk management and compliance, up from 55 percent in 2010. “There has been a substantial evolution in risk management among the big banks” in the U.S. and Europe, says Edward Hida, global leader of Deloitte’s risk and capital management group.

To skeptics, however, assertions of a new risk culture in banking ring hollow in light of the string of financial scandals since 2008, ranging from money laundering to bid rigging on municipal debt to the manipulation of the industry’s most widely used benchmark, Libor. “Yes, there’s been progress made on capital and on the quality of assets banks hold, but not on changed behavior or the banking model,” says Mohamed El-Erian, CEO of Pacific Investment Management Co. “Left to their own devices, banks will still resume behaving in a way that society finds problematic.” This tendency toward reckless risk-taking is endemic to the universal banking model, he contends — an unavoidable by-product of the growth imperatives that come with great heft. Martin Hellwig, director of the Max Planck Institute for Research on Collective Goods, based in Bonn, Germany, agrees: “I see the continuation of overbanking as a major source of risk into the future.”

Regulators have struggled to address this problem of excessive risk-taking. The U.K. government has committed to implementing the recommendations of the Vickers Commission, which called for big banks to ring-fence their deposit-taking businesses from riskier capital markets and trading activities, although it remains unclear how that will work in practice. In the U.S. progress has been slow in implementing the Dodd-Frank Act’s so-called Volcker rule, which is supposed to bar federally insured banks from proprietary trading. At the July 2013 Delivering Alpha conference, sponsored by Institutional Investor and CNBC, Treasury Secretary Jack Lew called for “swift completion” of the rule, but the regulators charged with carrying out the task seem less sure that will happen. “On Volcker, I don’t know what’s going on,” says the CFTC’s Chilton, one of the commissioners who must vote on the final proposal. On Capitol Hill calls demanding a breakup of the largest banks into separate retail and investment institutions have grown louder, but most officials and outside analysts believe that reform has moved too far down its current path for lawmakers to tear up Dodd-Frank and decree a return to Glass-Steagall.

WHAT ABOUT THE REGULATORS themselves? Many countries have overhauled their regulatory structures to better monitor and control risks. In the U.S., Dodd-Frank created the Financial Stability Oversight Council, a 15-member body that brings together the heads of all the main regulatory agencies to monitor systemic risk, under the chairmanship of the Treasury secretary. The Bank of England has established the Financial Policy Committee to fulfill a similar role in the U.K., and the European Union has set up the European Systemic Risk Board, chaired by Mario Draghi, head of the European Central Bank.

Dodd-Frank also established the Office of Financial Research inside the Treasury to help identify future risks. The OFR has driven the agenda on several major data standardization issues. It has shown an appetite to think creatively about risk measurement, borrowing from such nonfinancial realms as epidemiology and traffic flow monitoring in a bid to improve its understanding of systemic stress.

The FSOC and the OFR have limited mandates, though. They exist to gather data, produce reports and make recommendations. When it comes to designing a direct response to systemic risks, the FSOC has to funnel recommendations through specific regulators, such as the SEC or the Fed.

“FSOC so far has gone beneath remarkably low expectations,” says former TARP inspector general Barofsky. “It’s been a nonentity. It’s not been the driving force for reform it was supposed to be.”

Treasury undersecretary Miller, who oversees many of the operations of the FSOC, defends its record. The council has held 32 principals’ meetings since it was founded in 2010, she notes: “This is not a dormant organization. Regulators want to be there.” The council provided a recommendation late last year that helped the SEC come back with its revised proposal on money market funds. “The SEC cannot be forced to accept an FSOC recommendation,” Miller admits. “But it is not a small thing to have 15 financial regulators telling you, ‘We’re worried about this, and you need to act.’?”

Yet agencies like the SEC don’t necessarily take a systemic approach to policy formulation, nor are they obliged to follow the council’s advice. In short, the new framework has the ability to monitor systemic risk but not necessarily to take policy action. “There’s a macroprudential mandate built into the FSOC,” says the New York Fed’s Adrian. But the tools at its disposal are really microprudential tools used for macroprudential purposes. “It’s still a challenge to implement prudential policy for the system as a whole,” he says.

Regulators will be able to meet their macroprudential objectives only if governments “put in place decision-making structures such that regulators don’t just talk about doing things but actually have the power to decide,” says Stefan Ingves, governor of Sveriges Riksbank, the Swedish central bank, and chairman of the Basel Committee on Banking Supervision. The Bank of England’s FPC has this power to decide. It remains to be seen whether the FPC will be able to force action — imposing some type of credit restraints if it sees risks of a bubble, say — if its stability mission clashes with the inflation objective of the bank’s Monetary Policy Committee.

The challenge of safeguarding modern finance is all the greater because the financial system itself is in constant flux.

The crisis of 2008 was unexpected not because the specific risks that triggered it — egregious subprime mortgages, flawed securitizations — were unknown, says Gary Gorton, the Frederick Frank Class of 1954 Professor of Management and Finance at the Yale School of Management. “It was unexpected because the evolution of the financial system over a thirty-year period was not understood,” he writes in his recent book, Misunderstanding Financial Crises: Why We Don’t See Them Coming. “Any market economy constantly evolves, changes, transforms. Given the constant of constant change, the only question is: How is the system evolving?”

Markets and financial institutions transformed themselves after the collapse of Lehman Brothers, and they continue to do so today. The seeds of the next major financial crisis are already germinating, but we have no idea when or where they will sprout. And few people, save for a handful of optimistic government officials, will confidently say we are better prepared for it today than we were in 2008. • •

The Legacy of Lehman: A Look at the World 5 Years After the Financial Crisis

- Europe's Banks, Slow to Restructure, Pose a Systemic Risk Today

- Emerging Markets Face Mounting Challenges as Global Liquidity Dries Up

- As the Fed Readies to Taper, Is the World Ready for Higher U.S. Rates?

- China Exploits Crisis, Positions Renminbi as Potential Rival to Dollar