Consensus opinion on when the Federal Reserve will start normalizing rates has been a moving target. The expected “lift-off” date has shifted from March, then to June, and now to September or December. Some even suggest the first half of 2016 is more likely — and a small group seems to think it will never happen.

Back in March, we at BlackRock suggested that the Fed appeared afraid of its own shadow when it came to normalizing rates. In June we argued that the central bank seemed behind the curve in recognizing the economy’s ability to withstand a modest rate hike. At that time we suggested that the labor market was as strong as it had been in 20 years, and that as wages and inflation firmed in the months ahead, it would be clear that the Fed had a window of opportunity to raise rates. At this point, however, we think a monetary policy change would be ineffective for labor market improvement. Fiscal support could help, though excessive central bank policy has provided cover for the fiscal channel’s failure. And that may create long-term trouble if existing rate distortions aren’t gradually normalized.

With less than a week until the Fed’s September meeting, we’re concerned that this window of opportunity may be closing. If the Fed fails to begin policy lift-off this year, it may find itself with a set of more difficult decisions in the next. Unfortunately, international events, such as the China currency revaluation, the precipitous decline in commodity prices and the slowing demand and growth in emerging markets, may be threatening to further delay Fed rate normalization, even as the domestic economy is clearly signaling its readiness for the change. We live in a world that always has risks and headwinds, but particularly at a time when the Fed is being aided by historically easy monetary policy out of Europe and Japan — and perhaps now China and Brazil — its policy should evolve toward a more appropriately easy policy regime that better conforms to domestic economic considerations. For the Fed to act otherwise risks further market distortions, economic resource misallocations and likely a much more difficult set of decisions down the road.

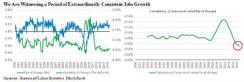

We think labor markets have witnessed such an extraordinary degree of improvement across so many fronts that regardless of the seasonally weaker nonfarm payroll employment print in August — likely to be revised meaningfully higher next month — this part of the Fed’s dual mandate has been achieved beyond reasonable doubt. Moreover, this strength is not solely in the nearly 6 million jobs gained in the past two years — as impressive as that is — but also in the manner in which it has been achieved, with an astounding degree of consistency.

To emphasize how extraordinary the consistency in jobs growth has been, we can observe that the three-year moving average in payroll change variability is at an all-time low (see chart 1). A modest slowdown in jobs growth, which we think is likely, would be because the creation of nearly 250,000 new positions a month over two years has taken a massive number of qualified applicants out of the unemployment pool, suggesting that we should reasonably expect an eventual decline in the run rate of monthly gross payroll readings.

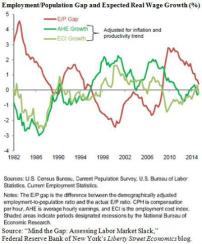

Another area that is vital for understanding the Fed’s policy reaction function is wage growth. Here, we were encouraged to see decent gains in the average hourly earnings measure, to 0.3 percent in August. The AHE had disappointed in recent months, as did the employment cost index data, but the reasons for that are clear enough. The fact is, the composition of jobs created appeared to be stronger in some of the sectors that are low-paying, keeping average wage levels subdued. There is evidence to suggest that it is the low-wage occupations that have made the least progress in real wage growth since the 2008–’09 financial crisis. Many have cited the lack of wage pressure in the system as justification for a delay in rate normalization, but here we would suggest that some of the Fed’s own research makes a strong case for why wage gains are likely on the way.

Specifically, in a recent post on the Federal Reserve Bank of New York’s Liberty Street Economics blog, Fed researchers wrote about their analysis of the degree of labor market slack by comparing the employment-to-population ratio with a demographically adjusted version of that metric, the difference in which results in the E/P gap measure (see chart 2). As the E/P gap turns negative — it is now approaching zero — labor market slack diminishes, and tightness ensues, which subsequently drives various wage measures higher. There are various other economic indicators and surveys that suggest wage gains are on the horizon.

All this is not to suggest that there are not still some pockets of slack in the labor force. At this stage, however, we think these are primarily caused by structural factors involving technological change and creative destruction, which Fed policy tools are ill equipped to remedy. Along these lines, we argue that the Fed must now determine the costs versus the benefits of maintaining interest rates at emergency condition levels, relative to whatever remaining labor force slack is left. Furthermore, we think present rate levels are unlikely to have any material influence on labor market conditions. If anything, marginally higher interest rates may in fact accelerate hiring, as more people gain confidence in forward interest income potential and decide to retire. At this stage, further help in job creation in those areas in which it is most needed, particularly for low- and middle-income households, as well as those displaced by structural forces, would be most effective coming from the fiscal channel. Beginning to raise rates now at a modest and measured pace would provide for more policy flexibility in the future.

Rick Rieder is chief investment officer of fundamental fixed income and co-head of Americas fixed income for BlackRock in New York.

Get more on macro.