The calls on the Street for a U.S. recession this year or next have intensified in recent weeks, with many forecasters rushing to stake a claim in terms of recession probabilities. The value of these calls is that they can help raise investor awareness so that a game plan can be put in place for such an eventuality. At Ned Davis Research, we’re all for that, and we advise clients to always be prudent — after all, the equity market tends to lead the broader economy. Moreover, bear markets associated with recession have historically been deeper and longer-lasting than market corrections or bear markets not associated with recession.

Enter first-quarter real GDP, which contracted at a 1.4 percent annualized rate, down for the first time since early in the pandemic. Net exports, inventory investment, and government spending all took a big bite out of growth. But consumer spending, capex, and residential investment increased, which is a sign that private domestic demand remains solid.

The case against recession

So, notwithstanding the negative print, the first-quarter contraction wasn’t broad-based enough to meet the National Bureau of Economic Research criteria for recession. In our view, there is enough economic momentum built in to sustain the expansion in 2022. Key economic indicators on our radar — which include manufacturing and services activity, employment, housing, financial conditions, and consumer and business confidence — remain broadly consistent with continued expansion, albeit at a slower pace, since many of these indicators reached local highs earlier in the expansion.Economic growth remains broad-based across the country, with the coincident indexes of all 50 states increasing in March versus one, three, and six months ago. As a result, our recession probability model based on state conditions continues to show minimal odds of recession at this time. A model reading above 50 percent would be consistent with recession, but that is not yet on the table.

The state coincident indexes are based on data from non-farm payrolls, manufacturing hours worked, the unemployment rate, and real wages and salaries. Their sustained gains in recent months show the resilience of the employment and income side of the economy in the face of rising inflation, the beginning of Fed tightening, and adverse geopolitical events.

Indeed, the labor market remains extremely tight, with job openings exceeding the number of unemployed workers, initial jobless claims hovering near their lowest level since 1969, and labor force participation still below its pre-pandemic level. Given that many older workers have left the labor force permanently, labor conditions may remain tight. And the Conference Board’s Employment Trends Index, which has a decent leading tendency when it comes to payroll growth, keeps posting new highs, all of which suggests that the labor market will stay healthy in the near term.

For this reason, aggregate payrolls — which are a proxy for labor income, and which have been growing by about 10 percent year-on-year, or more than double their usual annual pace — may continue to outperform. Needless to say, if people have jobs and continue to earn and spend, it will be hard to have a recession.

Moreover, both households and businesses have accumulated savings and cash reserves to smooth their spending and investment over time. Their balance sheets have improved, while low debt service for households and high interest coverage for non-financial businesses bode well for spending and investment and suggest a low risk of defaults.

The case for recession

There is still plenty to be concerned about. U.S. recession risks stem mainly from Fed tightening, persistently high inflation, spillover effects from the Russia-Ukraine war, and continued problems in global supply chains.Historically, recessions start a median of 25 months after the Fed begins a tightening cycle, although there have been three instances (in 1963, 1994, and 2015) when that did not lead to recession. In all three cases, unemployment was higher and inflation was lower than today. Given the lags with which Fed policy affects the real economy and the uncertainty of geopolitical and other exogenous shocks, the risk of recession increases in 2023 or later.

Fed tightening has little immediate impact on labor market conditions. But if the unemployment rate rose in short order above the Fed’s longer-run projection of 4 percent, it would signal excessive tightening and higher odds of recession.

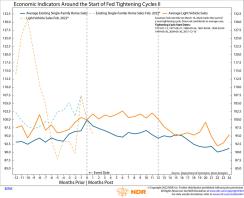

Interest-rate-sensitive parts of the economy, such as durable-goods spending and housing, usually respond quickly to Fed hikes. The housing market in particular reacts almost immediately to Fed tightening, since higher mortgage rates reduce housing affordability and weigh on future home purchases.

Single-family home sales and housing starts have already pulled back somewhat. The risk to the broader economy is amplified by a powerful housing multiplier effect. By some estimates, the multiplier effect from new construction is as large as that from infrastructure spending. Additionally, a prolonged correction in home prices could generate a negative housing-wealth effect, deepening a recession.

Housing and durable goods usually respond quickly to a Fed tightening cycle.

The early impact of the Russia-Ukraine war on the U.S. economy can be felt in reduced supply and higher prices for energy and other commodities. And since the war is still raging and economic sanctions on Russia have deepened, it could materially impact global supply chains well into next year. The risk is intensified by the widening (both in scope and duration) of the Covid lockdowns in China. Such supply shocks can reduce the Fed’s effectiveness in fighting inflation.

If inflation remains stubbornly high, the continued erosion of real incomes could sap real spending growth, leading to stagflation.

Weighing the evidence, we expect slower growth but no recession in 2022. Risks of recession increase for 2023 or later. If inflation remains stubbornly high and above the Fed’s longer-term target of 2 percent — particularly if exogenous shocks continue to hammer the economy — the risk of stagflation will rise.

Veneta Dimitrova is the Senior U.S. Economist for Ned Davis Research, a global independent investment research provider owned by Euromoney Institutional Investor.