Key Takeaways

Leveraging in-depth knowledge of infrastructure as a unique asset class is the best way to fully capture sustainability in an investment process.

- When considering North American midstream and hydrocarbon infrastructure, we have revised our longer-term growth expectations for commodity volumes lower, although it is still possible to discover relative value in the space.

- Sustainability factors are deeply embedded into the regulation of the U.K. water industry, with companies properly incentivized to deliver long-term resilience against climate change, reduce environmental degradation and improve water quality.

The features that single out infrastructure as a distinct asset class - the essential services it provides to society, its predictable long-duration cash flows and inflation-linked returns, its assets and investments exhibiting low sensitivity to economic cycles - also suggest this integration will have distinct areas of focus. Here we discuss the essential components of an integrated ESG approach to infrastructure investing and consider two case studies that illustrate how this approach may impact infrastructure portfolios.

A Three-Pillar Approach to ESG Analysis in Infrastructure

As in equities, there are many ways to incorporate ESG analysis into infrastructure investing. While many investors rely exclusively on third-party external providers to supply insight and analysis of ESG policy and practices, we believe leveraging in-depth knowledge of the asset class is the best way to fully capture sustainability in the investment process. We follow a three-pillar framework when analyzing sustainability for infrastructure assets:

- Valuation: To understand both positive and negative risks from ESG factors, it is necessary to model cash flow impacts of sustainability and perform sensitivity analysis. Factors might include different regulatory constructs, concession agreements and contracting structures as they affect infrastructure assets across the globe.

- Risk pricing or required return adjustment: ESG factors that cannot be captured in cash flows may be captured through an adjustment to a cost of equity, or hurdle rate. Focusing on the cost of equity enables a more robust global comparison within subsectors and captures improvements or degradations in a company’s ESG profile going forward.

- Engagement or active management: Managers of infrastructure portfolios should actively engage not only with company management but also with regulators, policymakers and other key stakeholders. Monitoring ESG controversies and active proxy voting are also key to influencing change.

Here we offer case studies in how ESG factors might influence infrastructure positioning in two different sectors: North American pipelines and U.K. water. The three-pillar framework not only identifies positive and negative ESG factors in these two case studies, but also allows for regular monitoring of how these sustainability factors evolve over time. Given the essential service and strategic nature of infrastructure assets globally, engagement with stakeholder networks is paramount to understanding how infrastructure companies operate on a day-to-day basis.

North American Pipelines: Pressure Will Lead to Differentiation

As the world transitions from higher-carbon-emitting forms of energy generation to more renewable-based generation in an attempt to control climate change, we expect a transition toward greater usage and increased capacity growth for lower-carbon generation and away from higher-emission fuel sources (Exhibit 1). As natural gas has lower carbon emissions than coal and oil, we expect it to be a bridging fuel, helping to meet the world’s energy demands with comparatively lower carbon emissions while more sufficient renewable energy infrastructure is built.

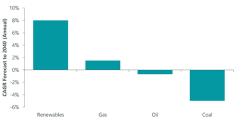

Exhibit 1: Growth in Energy Generation Capacity by Type

As of Sept. 30, 2020. Source: ClearBridge Investments, Bloomberg New Energy Finance. Compound annual growth rate ranges: renewables 7%-9%; gas 1%-2%.

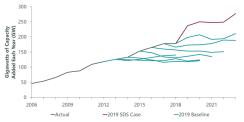

Some estimates would have natural gas serving as a bridge fuel for several decades. The market, however, is starting to price in a much faster transition to renewables as renewable capacity growth has consistently surprised on the upside (Exhibit 2), seeing this expressed in the higher amounts of capital expected to be invested into renewables.

Exhibit 2: Renewable Capacity Additions Continually Surprising on the Upside

As of April 30, 2020. Source: ClearBridge Investments, Bloomberg Finance.

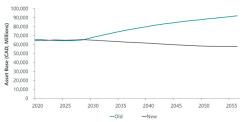

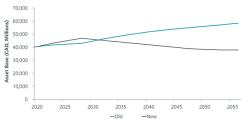

From an allocation perspective, increasing exposure to renewables allows a manager to benefit from this multidecade thematic. When considering North American midstream and hydrocarbon infrastructure, we have revised our longer-term growth expectations for commodity volumes lower. Rather than assuming hydrocarbon infrastructure will be a perpetual asset, we have made conservative assumptions that more effectively reflect a depreciating asset base over time, as renewables gain market share at the expense of hydrocarbons. Taking Enbridge, a hydrocarbon-focused pipeline infrastructure company, as an example, we have revised downward both its liquid and gas asset bases (Exhibit 3).

Exhibit 3A: Lowering Expectations of Natural Gas Asset Base Growth (Enbridge: Liquids)

As of Dec 31, 2019. Source: ClearBridge Investments, Bloomberg New Energy Finance.

Exhibit 3B: Lowering Expectations of Natural Gas Asset Base Growth (Enbridge: Gas)

As of Dec 31, 2019. Source: ClearBridge Investments, Bloomberg New Energy Finance.

Consequently, the total returns we expect to receive from pipeline companies focusing on the movement of hydrocarbons is coming down. These reduced expectations have impacted up to 25% of our equity valuation of pipeline companies in North America. The primary recognition here is a diminution in value as public policy shifts toward a cleaner environment, fewer emissions and less time using natural gas as a bridging fuel.

However, it is still possible to discover relative value in the North American pipeline space, where hydrocarbon infrastructure will still be used, albeit at a lesser rate, for decades to come. Those asset owners running trunk or mainline pipelines (transmission pipelines) will likely fare better in our view, as they are difficult to replicate, and are the key conduits that connect the supply to demand centers. Those that are running some of the smaller lateral pipelines and systems (gathering and processing pipelines) face a higher risk of disruption as they have a greater sensitivity to oil and gas production volumes.

We believe it is important to understand the winners and losers in the North American pipeline sector on a relative basis. Through cash flow forecasting, scenario analysis and in-depth research, it is possible to better understand the longevity of these North American pipeline systems and where there may be valuation anomalies. In 2019 and through 2020, after conducting extensive research, having detailed stakeholder discussions with numerous North American pipeline company managements and running comprehensive scenario analysis with inputs from industry-leading research groups such as Bloomberg New Energy Finance, BP Market Outlook, the International Energy Agency and the U.S. Energy Information Administration, our infrastructure strategies materially reduced exposure to the North American midstream sector.

U.K. Water: Privatization and Regulation So Far a Good Partnership

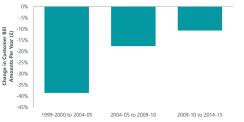

The U.K. water sector offers an interesting counter-example to North American pipelines. In the U.K., the water regulator, Ofwat, requires water companies to meet targets of environmental sustainability and service commitments, to which it attaches incentives and penalties. It also sets principles for board leadership, transparency and governance for the sector to ensure board decisions are aligned with customer and stakeholder needs. On the social side, Ofwat assesses the quality of U.K. water companies’ engagement with its customers and their satisfaction, as well as the utility’s relationship with its community. This regulatory assessment will have an impact on the companies’ investment plans, cost of capital and forward cash flows. In addition, due to Ofwat’s efficiency challenges, customer bills have fallen (Exhibit 4). Customer satisfaction levels for the value of water and sewerage service have been high: for water, 91% of customers are satisfied with what is provided by companies, while 76% are satisfied it is “value for money.”1

Exhibit 4: Efficiency Challenges from U.K. Water Regulator Have Lowered Customer Bills

As of Oct. 2015. Source: National Audit Report, Ofwat. Figures are the change in the average household bill over a five-year period, in 2014-15 prices.

There has also been substantial investment into water networks over time, and those networks have become far more productive after being privatized in 1989. This increased productivity has helped reinforce the above-mentioned decline in bills paid by customers over the last 30 years, in real terms. In this way, privatizations have benefited customers and other stakeholders of these regulated assets.

Over the longer term, we believe there is significant room for further growth in U.K. water assets. The sector continues to deploy capital to reduce leaking pipes, sewer flooding, supply interruptions and pollution incidents, while performing other necessary maintenance. Recently, the U.K. Environment Agency mandated all 20 water companies to deliver enhanced environmental obligations under the Water Industry National Environment Programme (WINEP). WINEP aims to improve and protect the water environment through initiatives put in place over the next asset management plan (2020-2025). In addition to WINEP, the sector has committed to achieve net-zero carbon emissions by 2030. Capital also needs to be spent on interconnector schemes to move water from high rainfall areas such as the northwest U.K. to larger population centers in the southeast. Importantly, Ofwat recognizes these long-term sustainability challenges and continues to urge and incentivize water companies to adopt new practices and innovate, to deliver long-term resilience against climate change, reduce environmental degradation and improve water quality. Social tariff schemes are also in place to support vulnerable customers and those that struggle to pay water bills.

Sustainability factors are therefore deeply embedded into U.K. water regulation, with the sector incentivized and aligned to achieve these outcomes. Mandatory performance standards for the sector continue to rise as regulators push companies to continually improve. Better-run companies with superior governance will benefit from regulation and legislation, earning incentives for delivering their strong environmental and customer engagement commitments as well as growing their underlying asset base. As a result, companies we view as more efficient and better operators of their underlying assets are held in our portfolios.

ESG Analysis Integral Part of Any Infrastructure Portfolio

It is imperative to incorporate an ESG and sustainability framework into any process that analyzes infrastructure assets. Such a framework should consider how ESG factors affect cash flows and the required return, or hurdle rate, of an infrastructure asset and should involve a process for engagement with several stakeholders on material sustainability issues. As evidenced when applied to North American pipeline and U.K. water sectors, such an approach enables active managers of infrastructure portfolios to identify compelling valuation discrepancies among assets. ESG factors form an integral part of any investment thesis in the unique area of the market occupied by infrastructure.

1 For sewerage, 86% are satisfied with what is provided by companies, while 77% are satisfied it is “value for money.” CCW Water Matters Annual Tracking Survey (6,310 total customers surveyed). Source: CCW; England and Wales, April 2019 to March 2020.