India’s 600 million mobile phone users face choices that are varied. They now have a faster and more robust Internet with better access to e-commerce, social networking and telemedicine. The market is flooded with 3G handsets and operators are ready with diverse services. The Indian telecom industry has come a long way. On one hand we have new players entering into the market and on the other, the existing players are facing stiff competition amongst themselves.

Though the subscribers have been growing at an exponential pace, the incremental subscribers are contributing significantly to lower ARPU’s (Average Revenue per User). This is due to a number of factors like voice becoming commoditized, reduction in tariffs, acquisition of lower-spending prepaid customers, etc. which are strategies adopted by the players to increase market share. In 1998 an outgoing call was INR 15.30 (30 cents in USD terms) per minute which has plummeted to INR 0.68 (0.01 cent in USD terms) this summer.

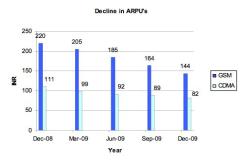

It’s not just India, ARPUs of top telecom operators across the world indicate that even though the data ARPUs show an uptrend, the combined ARPUs either have been declining or at best have remained stable. The decline is due to the falling voice ARPUs, which form the chunk of a customer’s spending.

The fierce competition between players has led them to look for alternative sources of revenue. Value Added Services (VAS) is one such example which contributes approximately 7 to 8 percent of the total wireless telecom revenues for Indian operators.

So, when we talk about Indian context, consumers are at a stage where they are still transforming from using basic telephony services to high-end value added services. India is yet to mature to data service usage and still comprises only a minuscule portion of ARPUs.

This brings us to the next big step that the telecom operators have taken, which is the introduction of 3G services. This has been termed as the big move that will boost broadband penetration and increase data usage. With the market already looking a bit slow, the amount bid for 3G technology is being seen as an unrealistic business move. It has not only created competition (which may in turn lead 3G to be commoditized) it has also made telecos fall into a debt trap. The bid that took place in May 2010 will go down in the history for being one of its kinds. The operators have to pay Indian Government a whopping sum of USD 15 billion (as against the government’s original expectation of USD 7.78 billion). Now, along with their diminishing revenues, Telecos have to deal with a hefty pile of debt. According to sources, till date, operators have managed to pay USD 10.8 billion for their licenses.

The companies are expected to shell out 30 to 47 percent of their FY10 revenues. According to sources telecos have borrowed loans from Banks and almost one third of their loans have been raised through the issue of commercial papers. Most of India’s telecom operators have high debt levels, with the exception of MTNL, BSNL and Bharti Airtel Limited. Servicing this debt will be a challenge as the firms are already facing more than 20 percent lower ARPU’s. Net debt to operating EBITDA ratio of most of the telcos will rise between 1 to 2.5 times. Reliance Communications and Idea will face grave challenges as their debt to EBITDA ratio is projected to be around 4.3 times and 3.1 times, respectively. Banks which have provided funds to the operators are treading carefully and are monitoring loans rigorously.

If the financial burden of these auctions would have been limited to license fees, we might have missed writing this piece. However, the license fee is just the beginning. The amount of capital expenditure investments required to install 3G handling equipment and technology across the telecom networks of all telcos will add a burden 2-3 higher than the license fee alone.

Some justify this investment by saying that some Telcos (like Airtel) are already facing severe bandwidth shortage leading to network outage, calls dropping on their voice frequencies. Therefore, they are buying 3G wavelengths to support the increasing growth in voice usage. However, increasing the total investments in telecom sector 3 times over is a very risky venture considering that further voice growth could still continue to be at the rate of lower ARPU’s, India being a very price sensitive market.

All these statistics lead us to one question- will the gamble pay off? Telecos have taken a huge risk with the 3G bids, now only time will tell what lies in store for them.

Shruthi Krishnamurthy is a Sustainability Analyst with Solaron Sustainability Services. She is based in India and covers the same market for Solaron. Solaron ( www.solaron.in ) is a niche Sustainability / ESG research firm with a global team of 60+ Analysts present across several Emerging markets like India, Brazil, China, UAE, Mexico, Russia, Eastern Europe and Africa.