Illustration by Jeremy Leung/II

Venture capital demands from investors a significant risk appetite — or at least that is the perception.

Academic research into VC funds since the 1980s has shown evidence to support the notion: On average, seven out of ten portfolio companies will not return even the money invested in those startups; the majority will need to be written off. This requires heavy lifting from the remaining three (out of our imaginary portfolio of ten). Two are expected to return enough to cover all the losses; the third to provide the 20 to 30 percent internal rate of return (IRR) investors anticipate.

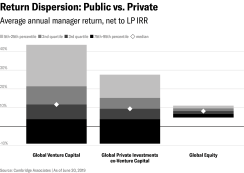

Venture capital, as currently commonly practiced, is rightly perceived as a risky asset class. As the below chart shows, venture fund industry returns show a very wide dispersion, with the bottom quartile of all funds losing money. This dispersion is significantly higher than in private equity funds and remarkable when contrasted with public equity, where even the bottom-quartile funds deliver 5 percent or better on average. Given the unpredictability of venture capital, one wonders indeed why VC portfolio allocations continue to grow among institutional investors, especially family offices.

Individual VC deals are indeed risky. It is also a fact that a few outlier mega-winners have an outsize impact on total industry returns. Much ink has been spilled on the selection of fund managers (the general partners, or GPs). Investors able to predict which fund managers will consistently pick those winners, if such is possible, will show exceptional returns.

How big is diversified enough? Classical portfolio theory says that in public equities, reasonable diversification effects can be expected when one combines 20 to 30 stocks, while more detailed recent studies set this number at 40 to 70. Most VC funds are of similar size: Why would this not be a sufficient number?

Two-thirds of venture deals fail, researchers have found. With such a high mortality rate, a VC fund’s actual ending portfolio size is merely one-third of its invested companies’. So to arrive at an exposure with 20 to 70 companies, a fund needs a starting portfolio of 60 to 210 startup investments. Very few funds meet this size.

In addition, experts in venture capital know that it is not a business of averages, but instead of many strikeouts and very few home runs. Significant portions of the average come from very few outlier deals. Evidence abounds. The distribution of returns in this study from Correlation Ventures shows that 0.4 percent of deals return 50 times the invested capital or more. Analysis shows that this handful of successful deals is responsible for around one-fifth of the total cash returned by the industry. To reliably access the excess returns generated by one in 250 deals, a fund size of more than 500 investments is needed. Anything less risks having a portfolio without any mega-winners.

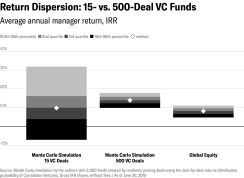

To verify, we ran a Monte Carlo simulation of returns in two VC funds: one with 15 investments picked randomly from a set of standard expected returns, and one with 500 investments (see the chart below). For each deal, we randomly selected outcomes based on the real observed probability distribution of venture deals. The simulated VC portfolio of 15 investments behaved very similarly to the real-life VC fund returns depicted in the first chart. There is a large dispersion between the top- and bottom-quartile funds, with a median return of around 10 percent. Bottom-quartile funds lost money, and the top quartile has its own large internal dispersion.

The second bar in the chart below shows the impact on returns when the VC portfolio expands to the recommended portfolio size of 500 investments. The outcome: The dispersion for the VC portfolio returns tightens to a range of 10 to 17 percent. This range of returns from bottom to top quartile is similar in size to that of public equity funds. With suitably high diversification, VC indeed becomes an investment-grade asset.

The Monte Carlo simulation also shows that funds with 500 portfolio firms have a 13.5 percent median return, compared to 10 percent for the 15-investment funds. In fact, the returns of the worst (fifth percentile) ultra-large VC funds are the same as the median returns from undiversified VC funds.

This counterintuitive result is further validated by a recent Kauffman Fellows study, which says that at the seed stage, “indexing beats 90 to 95 percent of investors picking deals.” In VC as a whole, it seems from Figure 2 that indexing beats 50 to 75 percent of investors picking deals, since indexing gives second-quartile results.

The golden rule for investors into the venture asset class must therefore be: Build a portfolio of 500 startups, with 100 companies being the absolute minimum.

So why are funds reluctant to offer such diversification? There are no rewards for diversification as a venture GP. Today’s investors flock to top-quartile managers, who must act in a risky manner to overachieve. Such GPs often insist that their portfolios must stay small to “not dilute their winners.” In other words, they rely on picking winners, but inadvertently admit to not being able to do so consistently. Managers who reduce risk by diversifying will, by definition, at best achieve second-quartile returns. Only the top quartile is rewarded, through performance and management fees on larger follow-on funds. Given the ten-plus-year life of each fund, and the way capital floods to proven winners, it is economically rational for a GP to take a risk at getting lucky with an undiversified fund rather than diversifying — knowing that diversifying would result in fewer if any rewards. This is especially true since most GPs show signs of overconfidence about their abilities, and trust that they will outperform, believing it will happen through skill, not luck.

Diversifying is also hard to execute operationally. Managing a portfolio of 100, let alone 500, investments takes significantly more effort than managing a portfolio of 20 investments. Manpower resource constraints in particular come to mind, as VC funds usually have a surprisingly small number of senior partners and dealmakers. (Most VC funds are structured as partnerships, with each partner expected to manage five to at most ten deals. Scaling a partnership above ten or so partners rapidly becomes complex.)

And few investors demand diversified funds, so GPs don’t offer them. A slow and steady “venture is a numbers game” pitch is much less emotionally compelling than “I am a rock star who can consistently beat the odds.” And GPs need an emotionally appealing pitch to get funded. In the world of venture, where deal-by-deal performance data is not widely, reliably, and publicly shared, and where fund-level results take a decade or more to be fully known, rational pitches should be expected to underperform emotional ones.

Many family offices and even institutional investors have explored a direct investing strategy as a way to gain venture exposure. This can be fun and exciting — who wouldn’t want a ringside seat to the young and aspiring startup world? — just as a casino can be fun: You might even win! But direct investing is hard to execute and is manpower-intensive. Building the minimum portfolio of 500 companies via direct investing requires a professional team with a set of expertise different from an investor’s fund-allocation team’s. Even more challenging is achieving suitably diversified deal flow sources. Nevertheless, it is theoretically possible for a disciplined institution that is willing to allocate substantial resources (see, for instance, the Canadian pension plans).

Building a well-diversified portfolio of startups with exposure to at least 500 venture investments is easier than one might expect: Investors who have deployed consistently into venture funds for the past decade without trying to time the market have been able to do so. By investing in three or four funds every year for a decade, you will maintain an ongoing portfolio of around 30 to 40 funds, likely aggregating to more than 500 companies.

Achieving geographic and sector diversification is significantly harder when investing in venture funds. Most limited partners (LPs) reinvest (re-up) with the same manager every two to four years. So an exposure to 30 to 40 individual funds may de facto result in exposure to ten managers. As a result, the exposure to 30 to 40 funds will be a de facto exposure to merely 15 VC firms, resulting in a mix of approximately five industry sectors across three geographies. This is a cherry-picking strategy, not a diversification strategy.

At a minimum, LPs should cover the gaps between their specialized fund strategies with one or more broad-based or index funds, of which a few exist, such as 500 Startups, the AngelList Access Fund, Y Combinator funds, or the Loyal Startup Index Fund (one of the authors’). More will be created if and as investors demand them. Alternatively, investors can target to manage 30-plus GP relationships to get full diversification, meaning investing in ten to 12 funds per year, or one per month. This may go beyond the resources of a large part of the allocator population.

How about fund-of-funds investing? In this case, investors must ensure the fund-of-funds managers obtain the diversification by geography, industry, stage, and time (and gender and race) that you are looking for. Many funds of funds tend to invest in the same few managers and strategies, with a focus on the same few geographies, industries, and stages. For instance, one fund of funds the authors interviewed has more than 80 percent of its venture allocation assigned to the U.S. market. This would raise eyebrows in any other asset class, yet is acceptable in private markets.

Based on industry studies, funds of funds frequently lack diversification across gender and race. This drives down returns as capital floods into overfunded sectors and entrepreneurs and ignores others that are less funded and hence, by the law of supply and demand, should offer high returns.

When paying a fund-of-funds for diversification — and exposure to unique, underfunded strategies and entrepreneurs — investors must demand that it delivers it. They should also demand proper reporting. The best reporting would be a company-level breakdown of where your funds have gone: by industry, country, stage, and year of the investment, and by gender and race of the CEO. This breakdown should then be compared with demographic benchmarks (e.g., country GDPs and population splits) to illuminate which strategies and types of entrepreneurs the fund of funds has left a portfolio globally overweight and underweight in.

Given how much effort it takes to do proper de-risked investing in VC, LPs may wonder, why do venture investing at all? One strong reason is the shrinking number of public companies; another is top tech companies choosing not to list until very late in their evolution. This means that to access the massive wealth creation of the tech sector, you need to be in private markets. Another answer is diversification: To get the best returns from your money, you should be exposed to all sectors of the economy, at all stages, including multistage venture capital.

A compelling financial reason is the relative performance and dispersion of a randomly selected 500-company VC portfolio, as shown in Figure 2, when compared with the return from public equity funds. Diversified VC offers evidence of consistently higher returns for a very comparable level of risk.

It will take work to assemble such a portfolio. It is hard to do by investing directly. Current funds and funds-of-funds are rarely designed with diversification in mind. Instead, they concentrate funding in a small subset of ultra-popular entrepreneurs, sectors, and geographies, which risks driving down returns on capital, leaving higher-return strategies underfunded.

Investors who allocate and diversify their funds wisely and accept the evidence will not only achieve better and less-volatile returns, but will also ultimately nudge GPs to finally design diversified funds.

Kamal Hassan is a founding partner of Loyal VC and an INSEAD alumnus. Monisha Varadan is a founding partner of Zephyr Ventures and an INSEAD alumna. Claudia Zeisberger is a senior affiliate professor of entrepreneurship and family enterprise at INSEAD and the academic director of the Global Private Equity Initiative.