Despite inflation continuing to slip further below the Federal Reserve’s 2 percent target, and Greece, Puerto Rico and China remaining firmly on investors’ watch lists, it appears the Fed will still raise rates this year. Here’s why.

The Fed is tasked with the dual mandate of promoting maximum employment and stable prices. The Fed’s ability to perform this delicate balancing act depends crucially on a two-part theoretical mechanism: specifically, a link between interest rates and economic activity and one between activity and inflation.

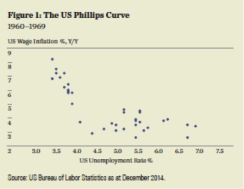

Economists have generally accepted that both exist. And there seems little doubt that high interest rates reduce activity by raising the cost of big-ticket consumer items such as cars and capital items such as residential housing, industrial plants and durable equipment. The link between activity and inflation, as illustrated by the Phillips curve (see chart 1), has changed over the past two decades, however — and might even have disappeared altogether, thus undermining the Fed’s inflation target.

The implication is that businesses have lost pricing power, so even if wage costs increase because of labor market conditions, employers are unable to pass them along to their customers but rather must absorb them as lower profit margins.

At least in the manufacturing sector, there is an intuitive explanation for why this has happened: globalization. Even if the U.S. labor market becomes extremely tight, there is a limit to how much workers can demand wage increases. If wage costs get too high, U.S. companies can simply ship jobs overseas. Similarly, if businesses are obliged to make some concessions on compensation to retain labor, they are limited in what they can pass through to customers because of, again, direct competition from abroad.

It is perhaps more difficult to understand why the Phillips curve has also flattened in the service sector, but not if you think about just how pervasive globalization has become in today’s economy. More and more service sector companies are becoming exposed to competition from abroad. Thanks to the communications revolution, a whole variety of business processes can take place nonlocally. Moreover, the offshoring of manufacturing jobs naturally creates an additional supply of workers for service sector jobs. That exerts downward pressure on wages in the sector, particularly toward the low end of the spectrum. It is no wonder, then, that wage inflation barely breached 4 percent and that favored Fed measure, the core personal consumption expenditures (PCE) index, which briefly hit 2 percent, even when the unemployment rate fell below 4 percent in 2000.

Why does the Fed need to begin tightening if unemployment is still above its full-employment equilibrium and inflation is essentially drifting sideways, about 0.6 to 0.8 percentage points below its target? These factors have already contributed to a revision of market expectations of the timing of Fed liftoff.

Earlier this year, most analysts predicted a June start to Fed tightening. The futures market is now pricing in about a 50-50 chance of a first rate hike in September. But why hike this year at all? After all, if the Phillips curve has flattened, wage inflation will remain largely unchanged, even if the unemployment rate falls below the level normally associated with full employment. Any effect on price inflation will be even more subdued, since any pickup in wage costs will depress profit margins, rather than raise output prices. Following this logic, from a purely economic standpoint, there would appear to be far greater risks associated with tightening too soon than tightening too late.

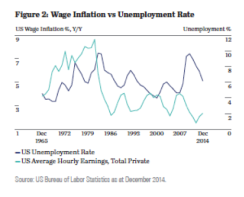

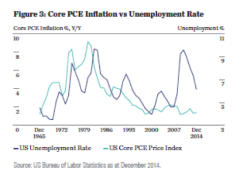

The Phillips curve was also at the heart of former Fed chair Paul Volcker’s battle to rid the economy of inflation in the 1980s (see chart 2). The Fed raised the federal funds rate to unprecedented levels early in the decade, causing the unemployment rate to rise to 9.7 percent in 1982 and wage inflation to fall from 8.6 percent in 1981 to just 2.2 percent by 1986. But whereas subsequent and sizable moves in the unemployment rate have caused inverse changes in salary growth, they have been relatively muted. Indeed, wage inflation hovered between 2.1 and 4 percent from 1986 to 2011 and only slipped slightly below that level in the aftermath of the 2008–’09 financial crisis, despite the unemployment rate’s hitting 9.6 percent. Core PCE inflation over the past three decades has been similar to that of wages (see chart 3).

The flattening of the Phillips curve means that if tightening were to coincide with some major deflationary shock — and the flaring of the Greece crisis this summer has provided an Exhibit A of the sort of risks that loom — the Fed would have little way of quickly getting inflation expectations back up again, and deflation could become a real threat. Given all that, what’s the rush? Why not repeat the fast-growth experiment of another former Fed chair, Alan Greenspan, in the 1990s?

There would appear to be three reasons not to, starting with the darker side of the legacy of that experiment — namely, its contribution to two major asset bubbles. It’s important to remember that the longer the Fed keeps interest rates at extraordinarily low levels, the greater the possibility for bubbles to form and to burst.

Second, in the same way the Fed would have next to zero ability to get inflation expectations quickly back up, it would also have almost no way of getting them back down if the Fed was perceived as falling behind the curve and expectations became unanchored to the upside.

Third — and perhaps most important — as long as policy interest rates remain close to the zero lower bound, the Fed has no ammunition to actually deal with a shock. Admittedly, the Fed could restart quantitative easing, but we at State Street are skeptical that would be particularly effective on its own.

The Fed thus appears to be trying to navigate a very narrow and tricky stretch of road ahead. By starting a gradual rate renormalization process in September, as the Federal Open Market Committee’s latest minutes suggest, the Fed is hoping it can reload the stimulus gun and gently let the air out of asset prices before a shock hits that could cause deflation to again become a risk — all while operating in an economy that has essentially stripped out the feedback loop between inflation and Fed policies.

Put that way, September is probably not a moment too soon.

Christopher Probyn is the chief economist at State Street Global Advisors in Boston.

See SSGA’s disclaimer.

Get more on macro.