Whereas various left-tail risks significantly diminished during 2013, Europe’s fragile economic recovery will likely see central banks keeping rates low for longer than forward-yield curves and many investors would suggest. Locking in “safe” credit spreads over the medium to long term has thus become a strategic priority for many insurance companies to enable them to meet their commitments to policyholders. Already, insurers operate under a wide range of investment and operational constraints that render asset allocation decision making increasingly complicated.

One might quickly conclude that insurance companies face only competitive disadvantages when it comes to investment decisions. One exception, given the long-dated nature of their liabilities, is insurers’ higher tolerance for illiquid fixed-income assets. Solvency II, which codifies and harmonizes European insurance regulation, appears to have accepted these liquidity advantages as regulators prepare to quantify capital requirements such as the matching adjustment. This aspect is also relevant to property and casualty insurers — even those with short-dated liabilities — which often seek to lock in a portion of their asset returns over the long term.

With liquidity after the credit crunch highly dependent upon financial regulation and central bank activity (see chart 1), insurers have an opportunity for strategic investment in illiquid or off-the-run investments with the hopes of capturing stable sources of meaningful, incremental yield from a range of options.

Note: Dealer inventories are at all-time lows in U.S. investment-grade corporate bonds, having declined 75 percent from pre-crisis to October 2013, with dealers holding less than 0.5 percent of bonds outstanding.

Source: Federal Reserve Bank of New York, J.P. Morgan as of October 23, 2013

Insurance companies should examine their asset allocation strategies in the context of the framework outlined in Pimco’s May 2009 economic outlook, “A New Normal,” and take a flexible investment approach. We have identified four relevant asset classes — emerging-markets debt, bank loans, financials and infrastructure debt — which illustrate the shift toward a more global and credit-diversified investment approach. They share the following characteristics:

- lower liquidity but appreciably higher yields than core European government bonds

- good technical and fundamental reasons to invest, with the possibility of allocating to up-and-comers

- capital treatment under Solvency II that is reasonable, with, for example, structured credit and securitizations excluded because of onerous anticipated capital charges

- investment strategies executed by insurers in a variety of markets but not yet universally accepted.

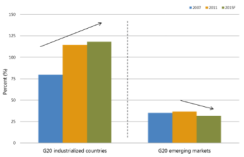

Emerging-markets debt has exhibited an upward-trending ratings trajectory driven by high growth and low levels of debt (see chart 2). We believe there is reasonable scope to expect strong returns in this asset class over the longer term. In fact, investing in emerging markets may provide investors with exposure to a secularly improving asset class with greater diversification than peripheral Europe, for example, which many would argue is a leveraged play on the euro zone.

Source: International Monetary Fund, World Economic Outlook (WEO) as of April 2013

Prior to the credit crunch, insurers usually accessed bank loans via capital markets by way of collateralized loan obligations, securities that allow banks to reduce regulatory capital requirements by selling portions of their commercial loan portfolios to international markets in a structured format, reducing the risks associated with lending. Whereas these instruments are enjoying some resurgence among U.S. insurance companies, Solvency II appears not to have sparked a similar rebound in Europe.

More acceptable, from a capital perspective, is the purchase of whole (not structured) loans whose capital treatment is in line with bonds. For insurance companies, the higher yield offered by bank loans provides a strong impetus to invest. Bank loans, which are typically five to seven years in maturity, usually constitute the most senior debt in corporates’ capital stock and often enjoy higher recovery rates than unsecured debt. Although providing reasonable spread duration, bank loans offer little interest rate duration because of their LIBOR-linked yields. There are some important technical differences to similarly yielding instruments for insurers to consider, however:

- The LIBOR floor provides insurers with some protection in very low interest rate scenarios such as those sketched out during Solvency II stress tests.

- The issuers’ option to refinance means that the opportunity for profit is capped because of spread narrowing if the loan is trading at or close to par.

In the face of regulatory reforms, global financial institutions are deleveraging to comply with widespread pressure that should lead to fewer bank failures because of stronger capital buffers. Given the present market size and the fact that some types of financial companies should qualify for matching adjustment under Solvency II, insurance companies should not overlook this asset class.

Option-adjusted spreads as of November 30 for financials within Europe range from 10 basis points, for senior secured credit in core Europe, to 500 basis points, over peripheral Europe. This accommodates a broad range of risk appetites. Insurance companies that can take part in various levels of the capital structure have a particular advantage, given the rapid evolution of regulation, debt structures and spreads.

The long-dated nature of infrastructure debt and the prospect of long-dated fixed returns, which are free of mark-to-market constraints, are attractive to life insurers, given that these debt portfolios are not frequently traded. Add in the potential of benign capital treatment under Solvency II, such as matching adjustments, and one can appreciate why investing in infrastructure debt has become attractive to insurers. Under the European Commission and European Investment Bank’s Europe 2020 Project Bond Initiative, there is presently €2 trillion ($2.71 trillion) in public and private infrastructure investments planned across the European Union between 2012, when the program’s pilot phase was launched, and 2020. Whereas the assortment of projects is diverse, from transport to utilities to renewable energy initiatives, and the market somewhat opaque, it is possible to get triple-B-rated investments with spreads of 200 basis points.

The present enthusiasm among investors often fails to take into account some significant challenges in infrastructure debt, however:

- The number and nature of infrastructure projects will not increase sufficiently in the short to medium term to accommodate the rising demand from insurance companies. Long-term trends are difficult to predict, as a meaningful increase in the supply of investible infrastructure projects will require thoughtful government-led changes to national economies.

- Infrastructure lending requires flexibility, such as early repayment or reacting to the need to change terms during the course of the project. Insurers with long-term stable liabilities often wish to cut back on the borrower’s options to be able to meet matching adjustment requirements or, from an accounting perspective, want to treat the debt as hold to maturity.

- Banks are unlikely to surrender their existing commercial position. Although they face clear funding and capital challenges, banks enjoy considerable competitive advantages over newer entrants like insurance companies, including broader product offerings, a tradition of accommodating some borrower flexibility and the ability to cross-subsidize.

Eugene Dimitriou is a senior vice president and account manager with Pacific Investment Management Co.’s financial institutions team in London.

See Pimco’s disclaimer.

Get more on fixed income.