It’s getting harder to generate equity returns in emerging markets. Simply chasing the index — the so-called beta trade — won’t do the job any more. But with a more discriminating, active approach, we believe investors can still capture opportunities in the next phase of the emerging-markets growth evolution.

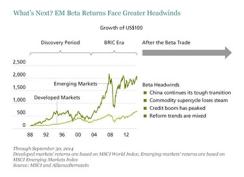

Over the past decade turbocharged emerging-markets economic growth has coincided with turbocharged investment returns (see chart 1). For the ten years ending December 31, 2013, emerging-markets equities and bonds delivered annualized gains of 11.2 percent and 11.8 percent, respectively, far outperforming developed-markets equity returns of 7.0 percent.

But the era of easy index-driven equity returns is probably over. Economic growth has slowed. The credit, commodity and investment cycles have peaked. Reform efforts in many emerging-markets countries have stagnated or regressed. China’s difficult economic transition and waning appetite for commodities is taking its toll. And the gradual normalization of ultra-accommodative U.S. monetary policy — and its resulting influence on capital flows — further cloud the outlook.

Emerging-markets equity valuations have fallen with the sell-off of the past couple of years, and these valuations are presently at some of the biggest discounts to their peers in developed markets over the past decade. But although emerging-markets companies are more profitable today, the disparity between emerging-markets and developed-world corporate profitability is far less pronounced than it was in 2003.

Against this backdrop, emerging-markets returns are likely to be more muted than during the previous ten years. So should investors steer clear? We don’t think so.

Great companies exist across the developing world, even in not-so-great economies. That’s the story for South African discount-apparel retailer Mr Price Group, which has posted earnings growth of 24 percent a year for the past decade, despite a sluggish domestic economy.

And emerging markets are no strangers to technological innovation. Such advances are producing new leaders across a variety of industries in Taiwan, including textiles, semiconductors and key industrial components (for tech giant Apple and carmaker Tesla Motors, for example). The rise of the emerging-markets middle class is creating new sources of demand for companies as diverse as Brazilian credit-card processing company Cielo and Chinese appliance maker Haier Group. And over the past two decades, we’ve seen the rise of world-class emerging-markets companies (think India’s Tata Consultancy Services and South Korea’s Hyundai Motor Co.), with good management, strong brands and differentiated technologies.

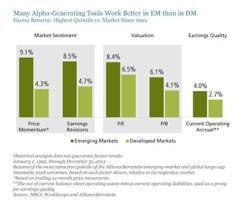

But is there fertile ground to generate alpha, or market-beating returns, in emerging markets? Our research shows that these markets are still far more inefficient and far richer with alpha potential than their developed-world peers. Certain equity factors, such as valuation, price momentum and balance-sheet quality, have been far more reliable drivers of excess stock returns in emerging markets than in advanced markets (see chart 2).

Other tools are less effective. For example, simply investing in companies with high sales growth hasn’t been a good investing strategy in most regions around the world, and emerging markets are no exception to this rule. Our research shows that focusing on a country’s economic growth potential also has had little or no predictive value in helping investors pick countries or stocks within developing markets. For example, Mexico has been one of the slowest-growing emerging-markets economies for more than two decades. Yet it is also home to one of the best-performing equity markets over the same period.

Beyond the metrics, to succeed in emerging markets, investors will need to identify companies that can most deftly navigate the new environment. Finding tomorrow’s winning economies will take rigorous research, entailing local knowledge and global industry insights — and a discriminating eye.

How best to capture the potential in emerging markets depends on individual return requirements and risk tolerance. But as a guiding principle, we think that shifting away from the benchmark and instead focusing on companies with strong capital management, high odds of positive earnings and attractive valuations should be a rewarding formula for investing in emerging markets — even after the beta trade.

Sammy Suzuki is portfolio manager for emerging-markets core equities and the director of research for emerging-markets value equities, and Morgan Harting is an emerging-markets portfolio manager, both at AllianceBernstein in New York.

See AllianceBernstein’s disclaimer.

Get more on emerging markets.