Local fixed-income securities issued in the emerging markets have become increasingly appealing to institutional investors seeking higher returns and diversification benefits. These markets — strong fundamentals, their growing economic weight and sound fiscal management — and the possibility of enhanced gains on both the underlying debt and appreciating currencies make for a compelling case.

The reality is more nuanced. Emerging-markets currencies can be volatile in the short term and subject to depreciations that can wipe out positive returns generated by local currency bonds. In fact, the currency risk is more than twice the underlying bond risk.

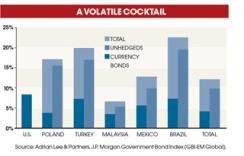

Similarly, Mexican government bonds returned an impressive 9.4 percent in 2011 only to see those gains wiped out by an 11.6 percent sell-off in the peso.

In other cases the currency market can be the main source of positive returns. For example, South Africa's rand rose by 25.5 percent against the dollar in 2009 while its bond market lost 1.4 percent.

The fact that a fixed-income market can remain healthy at the same time its associated currency is weakening, or vice versa, reminds us of a basic principle in investment, which holds that a bond and its associated currency are two separate investments that do not necessarily move together. In reality, they are driven by different fundamental factors. The bond markets reflect local monetary policy, inflation expectations, credit spreads and local real yields, while currency movements are determined by cross-border differences in price levels, the quality of traded goods and expected return on assets.

Over the past ten years, according to the JPMorgan Emerging Markets Bond Index, the best-performing bond markets did not have the top-performing currencies, nor did the worst-performing bond markets necessarily have the worst currencies. There was no systematic similarity or correspondence between these market performances. In fact, there were many periods when currencies and bonds moved in opposite directions. Indonesian bonds had the best performance in 2004 even as the rupiah was one of the worst-performing currencies. The statistical monthly correlation between local bond returns and currency returns has been low in the past decade.

Surprisingly, although they are aware of currency risk, many fixed-income managers rarely buy the bond market and hedge the associated currency. They tend to make some form of aggregate decision across both the bond market and the currency market. But with currencies frequently moving in a different direction from bonds, it makes sense to look into the possibility of unbundling these decisions to get the right currency and the right bond.

Given the higher risk attached to currencies, it is more important to get the currency decision right. This will help safeguard the portfolio's value against undesirable swings in foreign exchange rates and exploit inefficiencies in the currency markets to add alpha.

A process that separates the two decisions — a bond market selection and a separate currency exposure selection — can give investors the best combination of overall return from both sources. In practice, this requires picking the best-performing local bond market and then hedging the foreign exchange exposure into the currency that has the best expected performance. If investors had picked the top three emerging-markets bonds and the top three emerging-markets currencies over the past ten years, they could have generated additional returns of 14.5 percent, on average, compared with the three best markets by total return.

Managers that do not separate bond and currency decisions are being inefficient and missing out on the opportunity of enhancing returns. Those that leave the currency component unmanaged or undermanaged in the hope of long-term appreciation may be disappointed.

Adrian Lee is president and CIO of Adrian Lee & Partners, a Dublin-based manager of currency portfolios.