After Berkshire Hathaway (BRK.B) was added to the S&P 500 on February 12, 2010, the question many investors are now asking is: Does the BRK.B's sector classification actually belong in the Financial sector? If BRK behaves like a Financial, for all practical purposes (including portfolio construction and risk management) it should be treated as a Financial. However, our analysis of BRK.B’s historical returns shows it behaves more like a Consumer Staple stock than a Financial.

Investors in financial sector indexes are now finding themselves with exposure to BRK through commonly used products, such as ETFs. XLF, the most popular Financial Sector ETF, now has a significant weight in BRK.B. Other popular financial sector ETFs, like VFH, have smaller, though still significant, allocations to BRK.B. Since these ETFs are liquid, inexpensive and relatively precise, they’re widely used to make and hedge financial sector bets. However, if a large holding in a Financial Sector ETF doesn’t behave like other Financials, the ETF may be less representative of the sector and investors risk losing considerable precision.

BRK.B's sector classification is of particular importance to both long-only and long-short portfolio managers attempting to manage sector exposure. For example, consider a long-short portfolio manager attempting to construct a sector neutral portfolio. If the portfolio manager is long BRK.B and it behaves like a Consumer Staple and not a Financial, this portfolio will have unintended, potentially large sector tilts towards Consumer Staples and away from Financials.

Based on monthly return correlations, it appears that, in recent years, BRK.B behaves more like a Consumer Staple than a Financial.

As the chart below clearly shows, not only are BRK.B’s returns more closely correlated with Consumer Staples, but the magnitudes of its returns are more similar to Consumer Staples than Financials.

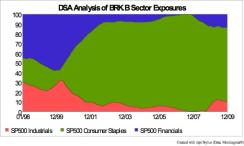

The results from this simple correlation analysis were further supported by more rigorous, quantitative analysis done using MPI’s proprietary Dynamic Style Analysis (DSA) model . When using a multi-factor model comprising of the S&P 500 sectors, Consumer Staples is the dominating factor driving BRK.B’s returns. Since 2001, the exposure of BRK.B’s returns to Consumer Staples is much larger than its exposure to Industrials and Financials combined.

Why does the market treat BRK.B as a Consumer Staple instead of a Financial when, according to Berkshire itself, their primary business is in the insurance and reinsurance sector? We posit that three different considerations, when viewed together, provide a plausible explanation. First, a large chunk of Berkshire’s insurance businesses are viewed as Consumer Staples not Financials. Second, Berkshire’s reinsurance businesses impact BRK.B’s idiosyncratic returns, but do not have a significant impact on its systematic returns. Finally, and most obviously, Berkshire has large public holdings in companies like Coca-Cola and P&G.

Interestingly, looking at the exposure chart above, prior to 2001, BRK.B traded more like a Financial than a Consumer Staple. What explains this apparent shift in how the market perceives Berkshire Hathaway? Arguably, 2001 was the start of a number of related financial and economic trends: The Fed’s infamous easy money policy; explosive growth in the origination and securitization of housing loans; expansion in the structuring and trading of complex financial instruments by many large financial institutions; the buildup of global trade and financial imbalances and the leveraging of US consumers and financial institutions. Perhaps what changed was not Berkshire Hathaway, but the financial world around it.

Michael Markov is the Co-Founder, CEO, and Director of Research, Markov Processes International, LLC (MPI), a provider of quantitative investment tools. Kushal Kshirsagar, Ph.D., is Director, Quantitative Research.