Some articles on municipal finance make it appear as if there’s a national crisis taking place. The reality, however, is more complex. Consistent with a country founded with a principle of rights accorded to individual states, there are enormous differences in how states have handled pension and retiree health care systems for public sector workers.

For many years, a full credit picture was hard to figure out. But more recently, new Governmental Accounting Standards Board rules have standardized the reporting of municipal liabilities. Accordingly, we at J.P. Morgan Asset Management are updating our assessment of how much it will cost states to service them.

Total state liabilities include bonds and other obligations related to underfunded pensions and retiree health care benefits, also known as other postemployment benefits, or OPEB. Pensions and costs related to OPEB are a big part of the picture: Whereas U.S. states have about $500 billion of bonds supported by state tax collections and general revenues, they have an additional $1 trillion to $1.5 trillion of unfunded pension and OPEB liabilities, depending on the rates used to discount them.

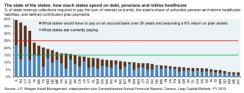

After analyzing 330 single-employer and multiemployer pensions, we came up with a single ratio for each state (see chart 1). In most cases, the results were reassuring. States at or below the green line in the chart do not need a disproportionate share of revenue to service debt. In a few other cases, however — states close to the red line or above it — the results are obviously very concerning.

Before getting into details, I want to be clear about something. Our project is called “The ARC and the Covenants,” a phrase that refers to the means by which states fulfill their obligations to public employees through annual required contribution, or ARC. Public sector workers form a critical part of civil society in the U.S. They protect us and rescue us when we’re in danger. They make our lives safer, cleaner and more efficient. We entrust them with the education of our children. They enforce the rule of law and provide remedies when laws are broken. They ensure our access to clean air, water and food. They heal us when we’re sick.

The legal, medical, environmental and educational problems sometimes found in other countries are a reminder of these workers’ importance. These individuals earned the benefits they accrued and which were granted by state legislatures — and have every right to expect them to be paid.

For states close to the red line or above it, the question is how these obligations will be paid. We’re closely watching the top four states most at risk in particular, which represent 20 percent of the entire general obligation municipal bond market. Our chart shows a statistic extrapolated from what we refer to as an IPOD ratio: interest on bonds (I) + pension payments (P) + OPEB payments (O) + defined contribution payments (D), all divided by state revenue collections (see chart 2).

Where would states get the extra funds to spend more on pensions and OPEB and still meet revised full-accrual IPOD ratios? In the table, we split the burden equally across tax increases, cuts in nonpension spending and increases in worker contributions. Illinois would need to raise taxes by 4.7 percent, cut spending by 4.4 percent and increase worker contributions by 100 percent. Each of these steps would need to be in place for 30 years, and revenues raised would have to be used solely for pension and OPEB purposes. Connecticut and Kentucky are similar to Illinois; however, the required tax increases and spending cuts are substantially higher in New Jersey. No such reforms will be easy, particularly since some of these states already impose the country’s heaviest state tax burdens on middle-income earners.

There are a lot of forensics involved with this sort of project. Nonetheless, the big picture remains. What is often described as a national crisis regarding state pension plans is very concentrated in a handful of states.

Michael Cembalest is chairman of market and investment strategy for J.P. Morgan Asset Management in New York.

Get more on pensions.