The sharp contrast between the growth in jobs and the performance of the rest of the U.S. economy is a particularly puzzling conundrum. Whereas gains in payrolls averaged more than 200,000 per month during the first quarter and recent jobless claims have hit their lowest levels since 1973, the wider U.S. economy slowed markedly, with gross domestic product growing only 0.5 percent the first three months of 2016. This is the slowest quarterly growth rate seen since the first quarter of 2014. Average annualized growth over the past six months was just 0.85 percent, the lowest since the fourth quarter of 2012.

And yet, during this six-month period, the U.S. added nearly 1.5 million jobs. Despite a disappointing jobs number in April — only 160,000, compared with the 205,000 that many economists were predicting — the overall outlook remains positive. The number of Americans filing for new unemployment benefits remains at historically low levels, which indicates a robust labor market. Of course, a further conundrum — particularly at the Federal Reserve — is why, given an unemployment rate of just 5 percent, wage growth continues to be conspicuous in its absence.

The answer to both of these puzzles most likely lies in the fact that while we may concentrate on the quantity of jobs being created, we should be paying closer attention to the quality of those jobs.

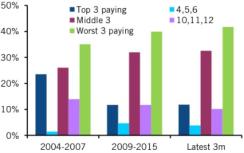

To illustrate this point, State Street Global Markets investigated job growth in the 15 major sectors in the U.S. labor market report (see chart 1) and split them into groups of three, based on average hourly earnings in those sectors. The three highest-paying sectors — professional and technical services, management and utilities — were grouped together; the next three highest-paying were in the following group; and so on. We continued down to the three lowest-paying: administrative and waste services, retail and the leisure industry.

Chart 1: Proportion of total jobs created

Top 3: Professional and technical services, management and utilities

4, 5, 6: Mining, information and finance, insurance and real estate

Middle 3: Construction, manufacturing, education

10,11,12: Other Services, wholesale, transportation.

Bottom 3: Administrative and waste services, retail and the leisure industry

Source: Bureau of Labor Statistics as of May 6

The disconnect between jobs and wage growth becomes much clearer.

Of the roughly 600,000 private jobs created over the past three months, nearly 42 percent were in the three lowest-paying sectors. In contrast, just 12 percent, or 68,000 jobs, have been in the three highest-paying sectors. That jobs growth gap has widened since the late 2000s financial crisis — and further still in 2016 thus far.

In the three years prior to the crisis, 35 percent of the jobs created were in the lowest-paying sectors. In the six years since the recession, this has risen to 40 percent. Also striking is the lack of jobs growth in the three highest-paying sectors: Prior to the crisis these sectors contributed 24 percent of all new jobs; postcrisis, only 12 percent (see charts 2 and 3).

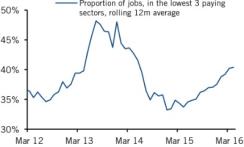

Chart 2: Lower-paying jobs in administrative and waste services, retail and the leisure industry on the rise

Rolling 12-month average

Source: Bureau of Labor Statistics, as of March

Chart 3: Better-paying jobs in professional and technical services, management and utilities, mining, information and finance, insurance and real estate continue to lag

Rolling 12-month average

Source: Bureau of Labor Statistics, as of March 2016

It is this lack of quality in the jobs created that goes a long way toward explaining why the improvements in the labor market have not been reflected in stronger growth — and also perhaps, why wages continue to struggle to post consistent gains.

Lee Ferridge is managing director and senior macro strategist for State Street Global Markets in Boston.

See State Street Global Advisors’ disclaimer.

Get more on macro.