“Many plan sponsors have been hesitant to de-risk their pension plans by allocating more to liability-driven investing (LDI) strategies in this environment,” says Jeff Whitehead, Head of Client Solutions, Aegon Asset Management US. “But there are alternatives to traditional LDI positioning available, and they may provide a transitional opportunity before full LDI implementation.”

Cash flow-driven investing (CDI): An alternative to LDI

For plan sponsors uncomfortable with allocating to longer-duration LDI strategies, Aegon AM US has developed an alternative approach that still allows for the implementation of a diversified equity and fixed income portfolio but with a focus on meeting the short-term cash flow needs of the plan. This approach allows pension plans to maintain a sizable allocation to return-seeking assets, if desired, while adding fixed income assets to the front-end of the curve to match near-term liability outflows. “Implementing a CDI strategy allows plans to take advantage of the flattening yield curve, and it is designed with the potential to mitigate the risk of needing to liquidate assets to fund pension outflows,” Whitehead says.

CDI portfolio allocations

Aegon AM US constructs CDI portfolios with the intention of providing cash flow from coupons, maturities and paydowns over each period immediately prior to a required outflow. The breadth of fixed income offerings across the curve combined with our deep and experienced credit research team broadens the universe of investment opportunities that may provide needed cash flows while maintaining portfolio diversification. “Our approach is a customized, multi-sector investment solution and provides plans with the potential to generate additional yield over the standard private pension discount curve, which references AA-rated corporate bonds,” says Jeremy Mead, Senior Portfolio Manager, Aegon Asset Management US. “The potential additional yield is sought through investments in investment grade corporate bonds, structured finance, high-yield corporates, and emerging markets debt.”

For investors that are looking for enhanced yields, a CDI Plus strategy may be a better fit, incorporating higher allocations to high-yield corporate and emerging markets debt, and also adding allocations to bank loans and distressed debt. “The opportunity for enhanced yields with CDI Plus also means the risks are higher compared to the CDI strategy given lower liquidity, higher cash flow uncertainty, and increased credit risk. These risks are considered during the portfolio construction phase with the goal of reducing the potential that asset cash flows fall short of plan outflows,” Mead says.

The charts below depict hypothetical allocations and estimated yields for CDI and CDI Plus strategies as of March 31, 2018. These examples are for a generic plan; Aegon AM US works in partnership with clients to evaluate potential asset allocations to meet the desired cash flow and risk profiles of each plan.

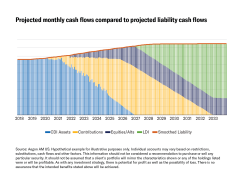

Transition to LDI

The implementation and continuation of a CDI approach can mean periodically funding the strategy with contributions, or re-allocating from other asset classes, to maintain a rolling matched cash-flow period. This longer-term approach to extending the cash-flow match allows for the transition into a more traditional LDI approach if yield opportunities and plan funded status improve over time. The graph below demonstrates a hypothetical pattern of sources of cash flow needed to meet projected liability cash flows. Note that the contributions shown in the chart may be deployed into CDI or LDI depending on the phase of transition in investment strategy.

Plan sponsors still evaluating whether the time is right to commit to a long duration LDI strategy may want to consider a CDI solution to meet short term cash flow needs. Today’s flattening yield curve presents an opportunity for plan sponsors to implement a CDI strategy, with the potential benefit of mitigating the risk of needing to liquidate assets to fund pension outflows. “Our team’s knowledge of multi-sector fixed-income investing, experience with asset liability matching, and our willingness to partner with plan sponsors on a customized solution, lend themselves to designing a solution to fit the needs of your specific plan,” says Whitehead.

Please contact Aegon Asset Management US for more information.

Past performance is not indicative of future results. This material is to be used for institutional investors and not for any other purpose. This communication is being provided for informational purposes in connection with the marketing and advertising of products and services. This material contains current opinions of the manager and such opinions are subject to change without notice. Aegon AM US is under no obligation, expressed or implied, to update the material contained herein. This material contains general information only on investment matters; it should not be considered a comprehensive statement on any matter and should not be relied upon as such. If there is any conflict between the enclosed information and Aegon AM US’ ADV, the Form ADV controls. The information contained does not take into account any investor’s investment objectives, particular needs, or financial situation. Nothing in this material constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to you. The value of any investment may fluctuate. Investors should consult their investment professional prior to making an investment decision. Aegon AM is not undertaking to provide impartial investment advice or give advice in a fiduciary capacity for purposes of any applicable federal or state law or regulation. By receiving this communication, you agree with the intended purpose described above.

The information presented is for illustrative purposes only. Individual accounts may vary based on restrictions, substitutions, cash flows and other factors.

Results for certain charts and graphs are included for illustrative purposes only and should not be relied upon to assist or inform the making of any investment decisions.

Specific sectors mentioned to not represent all sectors in which Aegon AM US seeks investments. It should not be assumed that investments of securities in these sectors were or will be profitable.

Diversification does not ensure a profit, nor guarantee against loss.

The estimated yield calculations shown for the CDI and CDI plus hypothetical fixed income allocations were calculated using the following market indices as proxies for asset class allocations. All yields used in the calculations are as of March 31, 2018. The yields for each asset class were weighted by the allocation weighting to calculate an estimated yield for each investment strategy.

IG Corporates: Bloomberg Barclays US Intermediate Credit Index

Emerging Markets: Bloomberg Barclays Emerging Markets USD Aggregate 3-5 Year Index

CMBS: Bloomberg Barclays CMBS 1-3.5 Year IG Index

ABS: Bloomberg Barclays ABS Index

HY Corporates: Bloomberg Barclays US High Yield Ba/B 1-5 Year Index Non-agency RMBS: Bloomberg Barclays US Treasury 1-3 Year Index

Distressed Debt: Bloomberg Barclays US High Yield CCC Only Index

Bank Loans: Credit Suisse Leveraged Loan Index

The hypothetical portfolio shown is based on Aegon AM US’ investment process and assessment of the market and reflects a portfolio of securities similar to one which the team would construct today if they were awarded a mandate of similar market value to the portfolio shown. The portfolio is based on sample guidelines and the credits selected are reflective of similarly managed portfolios, but do not reflect an actual portfolio currently being managed by Aegon AM US.

Portfolio holdings and other characteristics in individual accounts may vary depending on a variety of things, including but not limited to, account size, cash flows, account restrictions, and other client-specific factors. Holdings selected may positively or negatively affect performance. Portfolio holdings are subject to change daily. The hypothetical portfolio has been provided for purposes of comparison and as an example of a potential allocation. It should not be assumed that a client’s portfolio will mirror the characteristics of the example shown. The hypothetical portfolio characteristics shown are not taken from a representative account, although Aegon AM US manages accounts in similar strategies. The specific characteristics provided may not represent the entire universe in which Aegon AM US seeks investments.

Hypothetical examples are for illustrative purposes only. Hypothetical or simulated examples have several inherent limitations and are generally prepared with the benefit of hindsight. There are frequently sharp differences between simulated results and actual results. In addition, there are numerous factors related to the markets in general or the implementation of any specific investment strategy which cannot be fully accounted for in the preparation of simulated results, yet all of which can adversely affect actual results. No guarantee is being made that results shown will be achieved.

The holdings and asset classes listed should not be construed as investment advice or recommendations to buy or sell a particular security or invest in a particular asset class. The information presented is for hypothetical accounts and is for illustrative purposes only. Holdings may vary depending on a variety of things, including, but not limited to, the size of an account, cash flows within an account, and restrictions on an account. Holdings selected may positively or negatively affect performance. Portfolio holdings are subject to change daily. The portfolio examples have been provided for purposes of comparison and as examples of potential allocations. It should not be assumed that securities purchased for any portfolio were or will be pro table or that the securities listed were profitable. It should not be assumed that a client’s portfolio will mirror the characteristics of the examples shown. Aegon AM US may trade for its own proprietary accounts or other client accounts in a manner inconsistent with this report, depending upon the short-term trading strategy, guidelines for a particular client, and other variables.

There is no guarantee these investment or portfolio strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest over the long-term, especially during periods of increased market volatility.

This document contains "forward-looking statements" which are based on the firm's beliefs, as well as on a number of assumptions concerning future events based on information currently available. These statements involve certain risks, uncertainties and assumptions which are dificult to predict. Consequently, such statements cannot be guarantees of future performance and actual outcomes and returns may differ materially from statements set forth herein.

These materials are intended for use by sophisticated parties. While we have a financial interest in the sale of our products and services because we earn revenue once we are hired, we do not receive a fee or other compensation directly for the provision of investment advice (as opposed to other services) in connection with any such sale. We are presenting these materials to an independent fiduciary that is acting on behalf of a retirement plan in connection with the decision to hire the firm as an investment manager, and is capable of evaluating the investment risks associated with that decision.

Aegon USA Investment Management, LLC (AUIM), a wholly owned indirect subsidiary of Aegon N.V., is a US-based investment adviser registered with the Securities and Exchange Commission (SEC) and part of Aegon Asset Management, the global investment management brand of Aegon Group. AUIM operates under the brand name Aegon Asset Management US (Aegon AM US) and is a limited liability company formed on June 1, 2001 and began managing assets on December 1, 2001. The firm definition was revised January 1, 2018 to better reflect AUIM’s brand name and relationship within the global Aegon Asset Management organization. Aegon AM US is also registered as a Commodity Trading Advisor (CTA) with the Commodity Futures Trading Commission (CFTC) and is a member of the National Futures Association (NFA).

Aegon AM US claims compliance with the Global Investment Performance Standards (GIPS®). Please contact us at AegonInvestments@AegonUSA.com or 877-234-6862 to obtain a compliant presentation and/or a list of composite descriptions.

The enclosed information has been developed internally and/or obtained from sources believed to be reliable. Aegon AM US is under no obligation, expressed or implied, to update the material contained herein. Recipient shall not distribute, publish, sell, license or otherwise create derivative works using any of the content of this report without the prior written consent of Aegon AM US, 4333 Edgewood Rd NE, Cedar Rapids, IA 52499.

©2018 Aegon Asset Management US

2328293.2