It’s been a long road, but finally, on December 16, the Federal Reserve’s Federal Open Market Committee is highly likely to announce the beginning of policy rate normalization. Remarkably, this would be the first policy rate hike in nine years, so there is virtually a generation of young fixed-income traders who will experience their first rate-hiking cycle.

Ironically, the central bank waited so long for this move that we’ve reached a point at which domestic growth — and, clearly, global growth — appears softer as we head into the hiking cycle. Although that’s typically not a great sign, we think the Fed will be extraordinarily gradual in rate normalization and will do so in a manner that does not excessively unsettle the economy or markets. In fact, whereas FOMC forecasts suggest four hikes next year, we believe the path of rate increase is likely to be slower, with perhaps two rate hikes in 2016 after the initial December move. Still, these hikes will result in meaningful divergence in policy trajectory between the U.S. and other regions, such as Europe and Japan.

Further, the Fed is not likely to reduce its balance sheet for a long time, as global liquidity is continuing its evolution, with quantitative easing a thing of the past in the U.S. and with many countries’ foreign exchange reserve growth slowing or even contracting. Also, we think the U.S. dollar’s drag on the domestic economy may not be so intense in the year ahead, and because rate normalization should be a very gradual and controlled process, the economy and markets will be able to handle it well.

We have long awaited liftoff, and indeed for some time we have believed the Fed was running behind the curve on policy. In early 2013, we at BlackRock urged the Fed to rein in its third round of quantitative easing, arguing that it was distorting financial markets in unhelpful ways and was accomplishing little to directly aid labor markets. In mid-2014 we suggested in this very column that the economy was prepared for the start of rate normalization, yet a series of external events, such as trouble in Greece and slowing growth in China, combined with concerns over inflation expectations and a strengthening U.S. dollar, stayed the Fed’s hand. Today, however, with strong payroll data confirming the resilience of the U.S. economy to external shocks, we finally see fed funds futures pricing in a greater than 90 percent likelihood of a December hike.

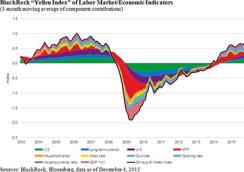

Indeed, after the seasonally weak pattern of late-summer jobs growth broke last month, the fourth quarter is shaping up to be a very solid period for labor markets. This headline labor market strength and a series of other jobs and growth metrics indicate to us that the economy is prepared for an initial rate move, as displayed by our proprietary Yellen index (see chart), which is back to pre–2008 financial crisis readings.

Beyond growing tightness in job markets displayed by headline payrolls, we are also now beginning to witness signs of wage acceleration. In fact, wages rose 0.2 percent month-over-month (2.31 percent year-over-year) in November, but extrapolating the two-month average (October and November) would get us to a more than 3 percent annualized rate of growth. Moreover, when those wage gains are considered alongside lower energy costs and generally subdued rates of overall inflation, the stage is set for quite strong real wage gains in the year ahead. That could power improved consumer spending in 2016, even though the U.S. consumer has recently displayed an increasing propensity for saving.

We’re not suggesting that market volatility will be subdued in 2016 — we expect it to be elevated — or that returns will be easy to come by. Both will present challenges to investors in the year ahead. Indeed, given the starting place on yields for many developed-markets bonds, as well as seemingly full equity market valuation levels in these regions, we believe many pension funds will struggle to meet overly ambitious return targets in the year ahead. Many institutions will likely seek to rely on increased allocations to alternatives. Here too, however, we’ve seen muted returns, and only tangibly differentiated instruments in this category may deliver required returns. In the end, with monetary policy diverging by region, we think it will be vital for investors to source interest rate exposures deliberately in those regions in which rates will be supported by continued policy accommodation and to exercise great caution in the parts of the market that will be pressured by rising rates. Thus flexibility, opportunism and caution will be key watchwords for the coming year.

Rick Rieder is chief investment officer of fundamental fixed income and co-head of Americas fixed income for BlackRock.

Get more on macro.