Illustration by Pete Ryan

Wall Street excels at selling things — but the academic-industrial-finance complex’s reputation for sophisticated mathematics is a myth.

The financial industry uses mathematics in a manner that would be mortifying to any other field of science. Academic literature and industry research are rife with pseudo-mathematical nonsense. You don’t have to look far to see where the motivation lies: Many of the authors are either employed by or retained by richly paid investment management and consulting firms. Faced with soaring investor interest in algorithm-powered investment strategies, the habit — indeed, the requirement — today is for firms to use scientific language and notation to nourish the idea that they’ve proved mathematically that there’s a way to systematically beat the market.

They haven’t.

It’s not surprising that more is claimed by their suggestive language than they actually “prove” because the field suffers from a subtle corruption. There is a pattern developing of publishing a semi-quantitative paper and using it as the basis to establish an investment advisory firm, become the seller of an investment product “relying only on math,” and go off on a globe-circling marketing bender. The fastest-growing asset management firms are purveyors of investment products that draw upon mathematical finance research, so theories ridden with poorly specified mathematics and wildly exaggerated results abound.

There is a saying that the math does not lie, but in 2015, renowned Nobel Prize–winning economist Paul Romer published a paper titled “Mathiness,” fashioned after the word “truthiness,” coined by satirist Stephen Colbert. The math is not real math, the kind you need to design an airplane or build a bridge or land a moonshot. Real math is painfully precise. (Watch the movie Hidden Figures if you didn’t already know that.) Investment finance math is sales math. It doesn’t matter that you don’t need it or that everybody interprets it in their own way. You’re using it to impress clients.

For many years, alpha was the Holy Grail of investment and almost all money managers claimed they could produce it. Then, under a Jupiter-sized weight of evidence that no investment manager — not mutual funds, not hedge funds — could reliably produce alpha, investment managers stopped laying outright claims to it.

Now, for many, there is a new Holy Grail: diversification.

Unable as a group to show that they can get returns, the industry changed the subject by shifting the focus of investing from return to risk. While the quest for diversification is never-ending, it is unclear exactly what would satisfy the promise of diversification: risk efficient, maximum diversification, minimum variance, equal-risk contribution, inverse volatility-weighted, diversity-weighted, and infinitely on.

Bedazzled by such superficial complexity of the math, risk-based portfolio construction products are all the rage.

Don’t let them pull the wool over your eyes.

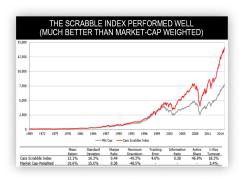

It’s exceptionally easy to come up with strategies that are more “diversified” than the market, beat the market in hindsight, and require no math. City University of London's Cass Business School created one of the more innovative weighting schemes when it introduced a portfolio based on the popular board game Scrabble using each company’s ticker symbol to calculate the Scrabble weight for each stock.

Xerox Corp. (XRX), for example, has nearly three times the weight of Apple (AAPL). Pulled from the largest 500 stocks in the University of Chicago's Center for Research in Security Prices (CRSP) database each December, it’s a better “diversified” portfolio and returned almost double the cap-weighted index.

Maximum diversity would be attained if all the stocks had the same capitalization — that’s called equal weighting, which is the most basic of diversification strategies. It buys a little of everything, and if you think about it, that Scrabble portfolio with 500 stocks is just tweaking around the edges of an equal-weighted portfolio.

What no one is telling you is that the historical performance and risk statistics of easier-to-understand, equal-weighted portfolios are very close to — and often dominate — these new, mathematically inspired portfolios. It is a supreme irony that almost anything that’s not of the capitalization kind will work — or not — as well as these new formulas.

Rebalancing plays an enormous part in the debate over alternative forms of equity indexing. Proponents claim that rebalancing provides some sort of a return bonus — harnessing volatility as a source of return — but you can’t say, “The rebalancing premium is always positive, as demonstrated by stochastic portfolio theory.” It’s impossible to distinguish rebalancing returns — which are specific to the act of rebalancing — from diversification returns, which can be earned by both rebalanced and un-rebalanced strategies.

And the so-called proofs for rebalancing are janky. One claims there’s a rebalancing bonus, but it’s based on computing average annualized return — a meaningless number — instead of annualized average return. You can’t earn that number in real life; it’s a math error. Others rely on the provably false assumption that assets always mean-revert, when, in reality, all markets have portions that are trending and de-trending. Markets experience both mean reversion and momentum; they are not in a perpetual state of negative autocorrelation. In any random time period you can get momentum or mean reversion. But their “proof” improbably assumes that the moment of rebalancing is also the moment at which mean reversion occurs. Curious coincidence.

It’s obviously not true; it’s easy to find an unlimited number of cases in which rebalancing doesn’t outperform buy and hold. If a lot of stocks persistently display strong trending behavior (up or down), this will harm a rebalancing strategy, as you will be constantly trimming the winners and adding to the losers. When assets have unequal and skewed-to-the-right returns — as in real life — a buy-and-hold strategy will produce a higher expected return as assets with higher returns drift upward and become larger components of the portfolio. You don’t need to invoke unnecessarily complicated stochastic calculus to understand that.

This rebalancing issue may explain why most active managers underperform: According to Hendrik Bessembinder, a finance professor at Arizona State University, the entire gain in the U.S. stock market since 1926 is attributable to the best-performing 4 percent of listed companies, and the cap-weighted indexes captured all of it because they don’t rebalance.

The promotion behind formula-based approaches is shameless.

For example, one recent article is titled, “Mathematician Believes He Has Magic Formula to Generate Wealth: Paris-based portfolio manager created an 'anti-benchmark' strategy that he says reduces risk while retaining growth.”

Magic formula? Seriously?

Sure, it’s important how you position your investment advice so stories differ in a Rashomon way — but when you look under the hood, the formulas behind many of these diversification approaches are so similar that they might be brothers from another mother.

A theory is just a theory. It is not a fact. By definition, a portfolio that has components that diversify each other will have a portfolio variance below the weighted average of the individual stocks within it. But hang on a minute: To the extent that this difference is large, an investor has put together securities that are intrinsically different from each other — but it doesn’t necessarily mean it’s more diversified than the market-cap-weighted portfolio. Betting on both red and black at the same time in roulette delivers a mammoth diversification ratio. It’s also stupid.

Maximum diversification has a name and story so fat that, like yelling “Hey Kool-Aid!” investors come crashing through the wall. What they’re leaving out of the sales pitch is that the maximum diversification portfolio is always more concentrated relative to the market-cap-weighted portfolio in terms of risk contribution.

Diversification usually means owning a lot of different investments, but maximum-diversification and minimum-variance approaches typically employ a relatively small portion of the investable set; it’s not uncommon for them to use only 100 out of 1,000 stocks — and this percentage decreases with larger investable asset sets. Where we come from, that’s concentration risk, and this whole process started because we were afraid the index was too concentrated and put too much weight on only a few assets. The new approaches made a de-biasing argument against concentration but then concentrated the portfolios in a different direction.

The truth is simply that there is no such thing in practice as maximum diversification. Assuming it is possible to create a portfolio more diversified than one that includes every company, the apostles of maximum diversification would have you believe they capture more independent sources of risk, but they’re erroneously calling random stock jiggles “more bets” when they're really evanescent uncorrelated sources of randomness associated with no risk premium.

“Maximum diversification” is a fetching catchword, but assumptions are being promoted as truths rather than disclosures. It’s popular these days to claim that a strategy does not rely on forecasts; these risk approaches claim to be agnostic, free of bias, and made without forecasts or bets. But presuming that all assets have the same Sharpe ratio is functionally equivalent to reverse-engineering expected return, so they don’t actually avoid that problem — they just use algebra as a backdoor way of addressing it. And, historically, expecting returns to move linearly with beta has been a bad bet.

The advertising says diversification is the firms' only bet, so maximum diversification is commonly misunderstood to have even exposure to all risk drivers, but as Apollon Fragkiskos, director of research at Markov Processes International, notes, “They claim to be unbiased, but it’s a rather technical definition on their side that isn’t what many practitioners consider it to be because their portfolios have biases and sector concentrations. You cannot have it both ways; you either diversify against stocks or factors.”

The bet that maximum diversification makes isn’t entirely on diversification; it’s that the market is wrong. Whatever new influence is reflected in market beta, the strategies lean away from it. To the extent that market beta reflects a growing influence — internet commerce, driverless cars, artificial intelligence, or cryptocurrency — this strategy will lean away from it. But markets aren’t always and forever wrong. Letting Amazon.com, Alphabet, and Netflix compound — instead of buying Sears Holdings Corp. because it was increasingly non-correlated — is exactly what made the index difficult to beat.

Facts of the Slide-Rule Variety

The investment world is characterized by one overarching feature — covariance — but everything has been utterly miscalculated, right from the start.

The cleverly named “anti-benchmark” formula for maximum diversification is looking for stocks that have exhibited the weirdest return history relative to the remaining universe — an objective that devolves into finding stocks that are less correlated to the market than most.

But since when is de-correlation equivalent to diversification?

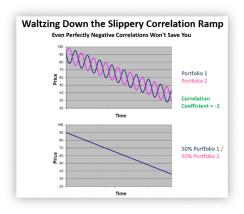

The central idea behind all this is safety. Yet the risk-mitigating capability of anti-correlation is somewhat suspect. The looming spoilsport observation is this: De-correlation won’t protect investors because two assets can be negatively correlated and crash simultaneously. Even if all of your investments are perfectly negatively correlated, you should still be nervous as a cat:

Low correlation won’t reduce your crisis beta; the truth on this will become clear when the next unrestrained liquidation of stocks is underway. That’s when you'll find the baby in the icebox!

Since the largest companies essentially are the index, becoming non-correlated translates into biasing away from the mega-cap stocks — but then so do all of the new strategies.

They are all designed to hold less capital in the larger stocks. It’s a new story but with the same small-cap and value answer we’ve been hearing about for decades. And ubiquitous: Value and small-cap exposures are naturally occurring characteristics unless the portfolio, like the cap-weighted benchmark, is designed to have a positive relationship between company valuation and weight — and nobody but cap-weighted indexers does that. The newest strategies are moving toward equal and even inverse weighting. Since small stocks typically have larger market betas than large stocks, part of the size premium may simply be the equity market risk premium in disguise. If that’s the case, these new, risk-based approaches will work no better than a prayer for a plague to pass you by.

(There was an extremely low percentage of kidding in that last comment.)

But still. If the end result of all these fancy ideas is to tilt toward small caps and value, why not just do that?

The math is a smokescreen for what can be accomplished relatively easily. English-lit majors are snickering at how obvious this is. You don’t need an elaborate model or have to optimize anything.

The most sellable products have hitched onto the intuitively plausible — but false — premise that cap-weighted indexes overweight overpriced stocks and underweight underpriced ones.

Naturally, there’s a “proof” that any non-cap weighted portfolio will beat the cap-weighted market — but this is logically impossible because for every non-cap weighted portfolio there’s a complementary non-cap weighted portfolio, together with which they are the market. They can’t both beat it.

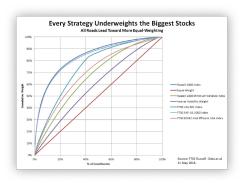

It’s supposedly easy to beat the index: Just avoid the bubble stocks and all you need to do is kick out — or underweight — the biggest stocks in the index.

Sorry, but school is still in session on this issue.

If it were that easy, active managers would be beating their indexes year after year because by now we’re sure they’ve gotten the memo about Rolf Banz’s 30-year-old paper “proving” that small-cap stocks beat large caps, which, by the way, isn’t true: He forgot to transform monthly holding-period returns to log returns before running his regression.

'So . . . Are We Alone?'

As we pride ourselves on having all the right prejudices, we will share the correct explanation with you.

Building an index and skipping or underweighting the biggest holdings is not genius. It’s true that the most expensive stocks — like Amazon and Alphabet — comprise the largest percentage of the index, but high-cap companies can just as easily be undervalued and low-cap ones overvalued. It’s not a statistical property that market-cap weightings leave you overexposed to overvalued companies and underexposed to undervalued ones because the largest stocks do not underperform the index.

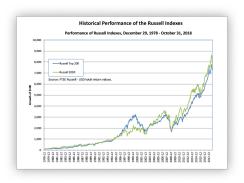

It all depends on how you landscape the facts. According to a 90-year study by Bessembinder, when buy-and-hold portfolios of stocks are sorted by beginning market cap and held for a decade, large-cap portfolio returns are higher (153 percent) than the mean returns for small-cap portfolios (97 percent).

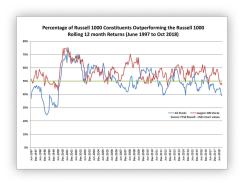

Nor do the largest stocks underperform the Russell 1000 year in and year out.

All that conference rigamarole sounds good — but do you know how the song goes?

We don’t want to disturb the sure-thing delusion, but this might curb your enthusiasm: Whether you look at the number of constituents or compound growth of the group overall, the largest 200 stocks do not underperform small stocks — not since Russell/FTSE has been keeping track.

The funny thing is how easy it is to believe the most expensive stocks are overvalued while at the same time we know the five horsemen of the digital apocalypse — Facebook, Apple, Amazon, Netflix, and Alphabet — have absolutely crushed it in the last five years.

More than 50 percent of the rally in the Dow in 2017 came down to just five stocks; more than 80 percent of the advance was centered in ten names. Funny how? Like a clown?

It’s a highly successful act of hypnosis, but there are lateral truths.

It may be true that the biggest stocks often mean-revert — but that doesn’t mean you can turn it into a strategy. Blockbuster was the Netflix of its day and if history is any guide, about 50 percent of the S&P 500 will be replaced over the next ten years. It’s also true that most firms fail. Disappearance or decline was almost three times as likely as growth, and corporate mortality rates are rising. And guess what? Larger companies are less likely to fail than smaller companies; older companies are less likely to fail than younger companies. Despite the existence of a small-cap premium, just 37 percent of small stocks have holding-period returns that exceed those of the one-month Treasury bill — versus 69 percent of stocks in the largest decile.

As soon as it implements a winning bet, a cap-weighted benchmark concentrates even further in its largest bet — but that doesn’t mean it’s gone complete village idiot and maximized its allocation at the worst time.

Avoiding the market’s most extreme bets sounds like a smart idea because cap weighting devotes the most shelf space to stocks that are not only the largest but also the most expensive. But — pay close attention here — expensive is not the same thing as overvalued. Recent research shows that very few companies — McDonald's, Johnson & Johnson, Alphabet, and the like — are responsible for most of the cap-weighted index’s gains over time. They are also all large, expensive companies that keep getting even larger. And today, the rich keep getting richer: More than 1 percent of global GDP passes through the Amazon/Alibaba ecosystems. Contra-trading against popular stocks and products must mean you don’t believe in the digital platform? Our guess is no. But maybe you're right; it’s all just a fad. Like the computer. And the internet.

And what if the larger companies are — and they undoubtedly are — more diversified than the smaller companies? Then shouldn’t you own more of the larger companies than the smaller ones, if you want to be diversified? Accidents do happen and the lower deciles experienced downright terrifying losses in the 1930s, so we wouldn’t consider driving smaller in size to be a great risk-control strategy.

Avoiding bubbles is one kind of risk-control strategy; surviving macro-economic crashes is another.

We’ve disbelieved plenty in our long lives, but only because so many of the facts don’t tie out.

These strategies carry the stamp of scientific certitude, but Wall Street’s researchers, like all scientists, have an ethical responsibility to communicate the limitations of these supposedly systematically proven models to an aroused but insufficiently skeptical, public.

Yet much of their world is bullshit. And yes, maybe we’re a bit too blunt. But we don’t want them to sell you more of what isn’t working.

Richard Wiggins works as a strategist at a large corporate pension fund. He authored this article independently of his employer.

Michael Edesess is a mathematician and economist. He is currently a research associate at the Edhec-Risk Institute.