The current fiscal thrust will likely push the U.S. budget deficit for 2009 to about $1.75 trillion, exceeding 12 percent of U.S. GDP. In all, according to the IMF, advanced global economies have infused direct support amounting to nearly 10 percent of world GDP. The fiscal stimulus, however, will not guarantee a return to growth. More likely, it will impede recovery and hamper medium-term prospects.

Upfront discretionary stimulus brings cost ramifications that can only be recovered over time, rendering the prospects for medium-term economic growth uncertain. Accelerating fiscal deficits across the globe have resulted in greatly increased issuance of government bonds. The lesson from Japan is that a shift to monetary growth in 2001 (quantitative easing), not fiscal stimulus, is what provided a way out of the “lost decade” of the 1990s.

The simple fact is that all government spending must be financed through taxation, borrowing or inflation. So any government’s ability to borrow and tax is limited. The stimulus debt must be repaid. If the stimulus is spent wisely on projects that truly expand output and hence yield a stream of revenue, then the medium-term effects are positive. If, however, the new debt is frittered away, then the outcome is problematic. The outcome of this grand Keynesian experiment ultimately depends, therefore, on how the money is spent.

The current stimulus in the U.S. is being allocated in ways that are unlikely to meaningfully expand output. Rather, it reallocates resources, by way of taxes, away from the most productive segments of the economy (information technology, healthcare) and toward less productive segments (autos, insurance, banking, home buyers). The auto and financial service sectors are unlikely to provide the robust economic growth engine required in the long run to provide the government with the revenue it needs to service its increased debt burden. Our debt servicing ability is further hampered by an aging demographic that will assuredly put immense pressure on the viability of social programs, such as Social Security and Medicare.

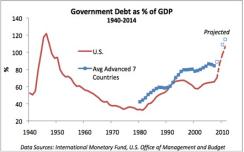

The challenge of producing a positive outcome by pulling the fiscal stimulus lever is compounded by the fact that the impact of fiscal policy on the strength of recovery is weaker for economies that have higher levels of debt relative to GDP. A historical view of debt-to-GDP ratios, depicted in the chart below, shows that developed countries are fast approaching historically high debt levels not seen since World War II.

A high debt burden neutralizes the influence of fiscal policy on the strength of recovery. This is due to some combination of a higher cost of debt, the crowding out of private investment and reduced consumer spending. The IMF estimates that fiscal policy actually becomes fully impotent when debt reaches around 60 percent of GDP. Beyond that level discretionary fiscal stimulus actually detracts from economic recovery.

Interestingly, the U.S. debt level was recently hovering right at this 60 percent level in 2007 and is now rapidly rising, making fiscal policy even less useful. This all suggests rather muted medium-term growth prospects. In short, the evidence suggests we cannot spend our way out of debt. Pursuing another round of significant stimulus — in order to decrease the margin of uncertainty, as some are suggesting — seems imprudent.

The key question is: Will the current aggressive stimulus generate the necessary growth to improve our fiscal stability going forward?

After World War II, the U.S. economy entered its halcyon days with vigorous growth led by the manufacturing sector (autos and steel, for example). The current decade has been quite different. We’ve placed emphasis on the much weaker prospects of financial services, while borrowing from the emerging nations in exchange for future promises (debt). This is why emphasis is needed now on industries that will fuel our future growth engine — if we can know what these are. This growth could very well come from innovations in health care, say for the aging populations of the developed world, or maybe it will come from technology innovations targeted at the young workers in China or India. It’s difficult to say. But a bright future clearly cannot lie in a focus on the relatively less productive auto and financial sectors, while continuing our debt binge.

This all bears compelling evidence that our current explosive path of stimulus hampers recovery and weakens confidence in government solvency. Sure, bailouts and stimulus instill short-term confidence as long as the state of public finance remains credible, but expectations of future long-term economic performance also matter importantly for how people behave today. On that basis, monetary policy should be favored over fiscal stimulus. However, given our current expansive fiscal programs, monetary authorities, in the near future, will likely need to strenuously fend off politicians in order to raise short-term rates to stave off inflation.

A prompt and specific plan for ensuring fiscal responsibility is critically important. That is, we must put in place now an exit strategy for paying off this massive debt. To some degree, this action is already in place as the host of automatic stabilizers (unemployment insurance, for example) will self-reverse as employment and output recovers. The same can be said for some of the recently initiated government lending programs — TARP, TALF and TSLF. These too are temporary and it is reasonable to expect that some debts are paid off in due course. However, if our massive debt is to be paid off by higher future taxes, we will likely follow Japan’s “lost decade” stagnation experience.

Worse, if we find that we are unable to pay off the debt via economic growth or, if we find that our ability to tax is lost (that is, higher tax rates result in lower tax revenues), then we are ripe for a period of inflation.

Rodney N. Sullivan is head of publications and editor of the Financial Analysts Journal at CFA Institute. Click here to view his profile.