To view this report as a PDf click here

Liability-driven investing, or LDI, is an investment framework used to manage current assets in order to pay off future liabilities. Many defined-benefit plan sponsors have adopted LDI strategies to improve their funded status ratios, or the percentage of future liabilities they are able to cover. “The use of LDI is growing with corporate pension plans separating their assets into return seeking vs liability hedging assets while also increasingly taking a more holistic view of their plans, thinking more in terms of overall hedge ratios,” says Nicholas Savoulides, vice president and portfolio manager at Loomis, Sayles & Company. Since the US Pension Protection Act in 2006 and the financial crisis two years later, pension funds have been challenged by stringent regulatory and accounting requirements, low interest rates, and volatility in equity markets. Implementing LDI has far-reaching affects—not only does it provide the ability to pay retirees in the years to come, it can reduce overall costs, smooth volatility, provide tax advantages, and strengthen corporate balance sheets.

Over the past year, funded ratios of many corporate pension plans dropped, taking major hits from lower interest rates and updated mortality tables. “Interest rates fell about 100 basis points, and the resulting increase in liabilities—perhaps 15–20 percent for a typical plan—more than offset gains in equities and alternatives,” says Amy Morse, director of U.S. pension strategies at Wellington Management. In 2014, the MSCI World Index returned 5.5 percent, including dividends. In addition, the Society of Actuaries issued updated mortality tables, which will increase pension liabilities for most plans by raising the assumed lifespan of plan participants and lengthening time horizons. “The new tables likely led to a drop of 5-10 percent in funded ratios,” she says. Collectively, the drop in funded status means higher deficits on balance sheets and higher pension expenses on income statements. In 2013, by contrast, pension plans overall saw a boost in their funded ratios as interest rates rose slightly and the equity market gained 27 percent.

“This seesawing of funded ratios has raised challenges for the growing number of corporate plans implementing glide paths that de-risk their portfolios as funded ratios improve,” says Amy Trainor, asset allocation strategist and portfolio manager at Wellington Management. As the funded status of a plan improves, assets are reallocated from the return-seeking portfolio, generally equities and other growth investments, and into the liability-hedging portfolio, composed of high-quality bonds with durations similar to the plan’s liabilities, typically 12-16 years. “Many plans are still in the early or middle stages of their glide paths, with a heavier emphasis on return generation,” says Trainor. “With the setback in funded ratios, de-risking might be on pause until funded ratios recover.” Some sponsors are considering re-risking—shortening duration or adding to return-seeking assets. “While the automatic response based on the glide path might be to re-risk, factors such as the current interest rate environment might require a more dynamic approach,” she says.

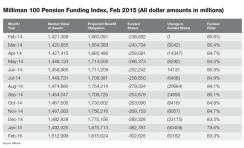

Liabilities are largely tied to interest rates, and funding ratios improve when interest rates rise or return-seeking assets perform well. On average, the funded status of the 100 largest U.S. corporate pension plans stands at 83 percent at the end of February 2015, according to the Milliman 100 Pension Funding Index. “With continued low interest rates, as well as the upcoming mortality table revisions, we may see a slowdown in de-risking,” says Savoulides. The process of de-risking is governed by a fund’s particular glide path toward improving its funded status. “Glide paths are pre-dominantly dictated by funding ratios,” he says. “Until funded status levels increase, many pension funds may be reluctant to invest further in long-duration fixed income.”

Interest Rates

While the future potential path of rates may be somewhat asymmetric, it is still not obvious that rates will go higher. “Quantitative easing in Europe, with the 10-year German bond at 0.25 percent, certainly makes 10-year U.S. Treasuries at 2.0 percent attractive,” says Savoulides. Even when the Fed starts to raise rates, it does not imply that the longer end of the Treasury curve will also move higher. “Managers who think they’ll rise could choose to shorten duration exposure and exploit some of the by-products of a potential rate increase,” he says. For example, corporate spreads and spread curves tend to be inversely related to the Treasury curve.

Despite the pause in de-risking, plan sponsors aren’t abandoning LDI. “They are actually more convinced,” says Joe Nankof, a partner at Rocaton Investment Advisors. While the short-term reallocations to long credit, predicated on funding status improvements, might change plans’ glide paths, adherents to LDI believe it’s best to stay the course. “There’s a total return mindset among pension directors, and it’s true, long-duration assets would perform badly in a rising rate environment, but LDI allocations are not made to generate return,” he says. LDI works best with a risk management mindset and a view of the bigger picture. “We recommend shifting into long duration regardless of the rate environment,” he says.

The most successful LDI programs are those that have a plan-level liability de-risking strategy in place, are systematic and have an agnostic view of the direction of the financial markets or interest rates. “Timing interest moves is a fool’s game,” says Suny Park, institutional client strategist at Janus Capital Group. By matching plan assets to plan liabilities, LDI strategies seek to decrease the funded status volatility so that moves in the equity and fixed income markets aren’t amplified in the funded status of a pension plan.

The average volatility of the S&P 500 has been about 15 percent per year over the past 25 years, compared with the Barclays Agg, which has varied by 3-4 percent on an annual basis. Focusing on growth assets, pension plans can be more tactical in the way they compose equity portfolios. “If you can decrease the volatility of an equity portfolio from 15 percent to 10 percent, it can have a meaningful impact on the funded status volatility,” he says.

Those who are concerned about equity volatility can tactically tilt portfolios tilt away from the S&P 500 to low- or managed-volatility equities. Another way is to use liquid alternatives or hedge fund strategies that target 8-12 percent portfolio volatility. “Six to eight percent is an acceptable level of return if they are uncorrelated to stocks and bonds,” he says. The mix between growth and liability hedging assets and the asset mix within the growth portfolio will determine how fast or slow the plan assets will grow, as expected return on plan assets decreases when assets are shifted from growth to liability hedging. “Looking at it holistically requires the plan sponsor and investment committee to have a completely different mindset,” he says. Too often, plan sponsors segregate the left side of the plan’s balance sheet from the right side. But if the ultimate objective is to decease the plan liabilities, plan sponsors cannot ignore the interaction between plan assets and plan liabilities.

The effects of market conditions may prevail—plans want to de-risk, but not at the current low interest rate levels. “However, there is a strategic imperative to continue to de-risk underfunded plans,” says Jim Moore, managing director at PIMCO. While it may be counterintuitive to buy long bonds at historically low interest rates, there was overwhelming demand among pension funds to buy long credit in 2013. “There was a massive inflow during the taper tantrum,” he says. Although tactical considerations are colored by low interest rates and low levels of funding, LDI is, by definition, a strategic initiative. “LDI is not an either-or program,” says Rene Martel, EVP and pensions and insurance solutions specialist at PIMCO. “The glide path is the bridge to fully funded status.”

An Ongoing Process

Most U.S. DB plans implement some form of LDI, and some estimates are as high as 75 percent. “It’s an ongoing risk management process,” says Martel. A typical portfolio with an allocation of 60 percent equities, 40 percent fixed income usually has broad market exposure and sensitivity to interest rate moves. “The first step is to align the fixed income assets with liabilities, which means investing in long-duration bonds that have a similar risk profile,” he says. The next step is to decide if a 40 percent fixed income allocation is enough. Finally, the strategy can be optimized with interest rate derivatives and other strategies to maximize the coverage of the liability hedging assets. Derivatives can also be used in a smaller plan or in the early stages of a plan that has an emphasis on asset growth. “It’s important to be strategic and get the process and governance in place,” says Moore.

Structuring a growth asset portfolio within an LDI strategy is a holistic process. “The liability hedging side needs to be aligned with the growth side,” says Nankof. The default is long-only equities, which are liquid and they carry a risk premium. “Anything other than that requires a good risk management rationale,” he says. High-yield bonds, convertibles, emerging market debt and bank loans can offer more diversification and downside protection. Multi-asset strategies, including risk parity and macro asset allocation, as well as liquid alternatives, such as hedge funds, long-short and relative value, can mitigate risk as well. Finally, illiquid total return investments in private equity and real estate can complement the overall portfolio. “The perception of these change when you think of LDI,” he says. “We look for shorter duration investments of five to seven years to get your money back to help annuitize the plan.”

“We think the current market environment requires a smarter, more nimble approach to re-risking,” says Trainor. “For example, given the potential for rates to remain low, sponsors might want to be cautious about reducing duration aggressively.” However, those who have a strong view that rates will rise and have the risk tolerance to absorb a lower funded ratio if that view is wrong may want to consider reducing interest rate duration while leaving corporate bond exposure untouched. This may help to manage transaction costs, and it also takes into account future demand from corporate DB plans for long-duration corporate bonds. “Coupled with low liquidity in the corporate bond market, that future demand could make it difficult and costly to reestablish those positions later,” she says. Plan sponsors could also consider innovative glide path approaches, such as basing the re-risking or de-risking decisions on funded-ratio volatility targets. “Another new approach we’ve been working with is a two-tiered glide path that gives the plan sponsor leeway to actively manage exposures along the glide path,” says Morse.

By Howard Moore