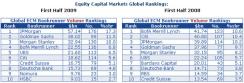

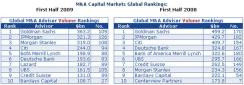

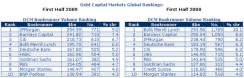

In the preliminary ranking for the first half of this year from Dealogic, it’s easy to separate the winners — JPMorgan Chase, Goldman Sachs and Morgan Stanley — from the losers — Bank of America Merrill Lynch and Citigroup.

All three winners are at the top of the chart in equity ratings, and in advising companies on mergers, acquisitions and (increasingly) restructurings in this down economy, Morgan Stanley is the big gainer, moving from eighth last year to third. In the less-lucrative business of underwriting debt, Bank of America Merrill Lynch dropped from number one to fourth place while JPMorgan moved up to the top spot.

The gainers are picking up market share as never before. JPMorgan’s market share in global equity underwriting jumped to 17.3 percent from 10.2 percent last year. Its share in global debt underwriting increased to 9 percent from 8.2 percent.

The falling angels — to borrow a term from credit-rating agencies — have been forced to reduce capital and personnel in these businesses over the past year. Rochdale Securities analyst Richard Bove says the current trend will likely continue. He doesn’t see the likes of Merrill Lynch, Citigroup, UBS or Credit Suisse increasing their capacity at investment banking anytime soon as each battles substantial internal problems. Moreover, new legislation will probably reduce competition from competitors like GE Financial and Target Financial Services.

So the top-ranked firms’ concentration of market share leaves them well-positioned.

“Investment banking is the first domino of a series of revenue-driven activities,” Bove says. “It leads to more proprietary trading opportunities, more margin account and investment management businesses.”

As to when the rankings will be reflected in the companies' bottom line, Bove says that it won’t be until next year for JPMorgan, which continue to deal with the fallout of problems in loans, consumer credit and commercial real estate. For Goldman Sachs and Morgan Stanley, it could be as soon as the next quarter.

Xiang Ji (Nina) is the capital markets reporter at Institutional Investor, covering mergers and acquisitions, debt and capital markets from an institutional investor’s perspective. Xiang Ji was formerly with BusinessWeek in China covering the wider business world. Send email to capitalbeat@iimagazine.com .