Sponsored by Capital Group®, home of American Funds®

Are you confused by long menus at a restaurant? Plan sponsors face the same challenges with their investment menus, which can lead to participant inaction and imbalanced portfolios. The science behind restaurant menus may provide some insight into how to combat this.

The science of menu engineering

Did you know menus are designed to make it easier for you to choose the meal you want? “The restaurant industry has probably spent tens of billions of dollars over the years trying to understand menu design, menu engineering and psychology,” according to restaurant consultant Aaron Allen. Every item you see on a menu is placed in a precise location to drive customer behavior, which often comes down to making difficult choices easier and quicker.

Examples of menu engineering

Menu engineering naturally extends to the number of options diners have. “More than seven is too many, five is optimal and three is magical,” according to menu engineer Gregg Rapp.

Streamlined menus make it easier for diners to choose — and take less time to read.

We can learn something from this in the retirement plan industry.

76% of DC assets are outside of target date options

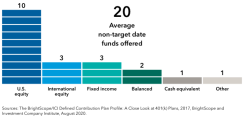

Despite the success of target date funds as a “one-stop” solution for retirement plan participants, most defined contribution (DC) participants are still “do-it-yourself” investors who pick funds off the investment menu.

With 20 funds on an average plan’s menu, this may be too much choice, and can lead to decision paralysis.

How did DC menus get so big? The Morningstar style box, which was originally intended to be a descriptive evaluation of a managers’ investment style, has turned into something prescriptive — as building blocks for portfolios.

Some action steps to consider for reducing plan menu size:

U.S. equity

Checking all the style boxes is no substitute for offering a small number of well-thought-out U.S. equity menu options.

- Beware too many entrees — Make participants’ decisions easier by limiting U.S. equity menu options to three or four funds with clear and distinct investment objectives.

- Fusion outside the style box — Select funds that capture a broader range of styles, market capitalizations and sectors to make it easier for participants to digest.

- Consider participants’ appetite for risk — Look to pure growth funds for younger participants and to more dividend-oriented “blue chip” equities for those nearing retirement.

Funds with broad geographic flexibility may be used as core international/global menu offerings to simplify and direct participant choices.

- “It’s good for you” — Treat non-U.S. equities in participant education efforts as the vegetables participants may not want to eat but don’t get enough of. Many participants are “home biased,” preferring more familiar U.S. companies to less-familiar foreign names.

- The global smoothie — Make non-U.S. exposure easier to stomach by offering global funds, which combine unfamiliar non-U.S. firms with more familiar, multinational companies.

- Don’t attempt the exotic at home — Let portfolio managers, not participants, strike the right balance between developed and emerging markets exposure. Consider an international equity fund with flexibility to invest meaningfully in emerging markets.

One core fixed income menu option that has done what it’s supposed to do without unpleasant surprises can go a long way toward providing balance in a retirement plan.

- Balance the meal — Use bond funds to help dampen portfolio volatility in four ways: diversification from equities, capital preservation, income and inflation protection

- Don’t get fancy — Emphasize core bond funds that stay true to their role by not reaching for yield at the expense of too much credit or duration risk.

- Taste before appearance — Evaluate how fixed income actually behaved in real-market conditions instead of just relying on benchmark or category to approximate risk and return levels.

Investing outside the United States involves risks, such as currency fluctuations, periods of illiquidity and price volatility, as more fully described in the prospectus. These risks may be heightened in connection with investments in developing countries. The return of principal for bond funds and for funds with significant underlying bond holdings is not guaranteed. Fund shares are subject to the same interest rate, inflation and credit risks associated with the underlying bond holdings.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses. This and other important information is contained in the fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only.

American Funds Distributors, Inc., member FINRA.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

Copyright © 2021 Capital Group. All rights reserved.