No matter where you look in the capital markets, it’s getting harder to find returns. But don’t despair. By taking a fresh look at high-conviction strategies, we believe investors can discover more effective active routes within equity allocations to reach diverse destinations.

Conviction isn’t just a catchphrase for unbridled confidence. It’s about applying knowledge, judgment and experience in an active stock-picking approach with a clearly defined angle on the market. Our research shows that strategies like these can be very productive — if you understand what conviction really is and how it works.

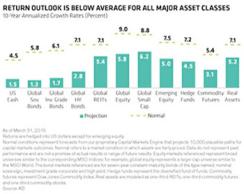

The outlook for returns is sobering. From stocks to bonds to real assets, our forecasts indicate that returns are likely to be below average for all major asset classes over the next decade (see Chart 1). In this environment, beating the market by even a small margin of 1 percent a year can make a big difference.

Click to enlarge.

Yet many investors are settling for much less. Instead of trying to augment returns, they continue to flock to passive investing. Diversified portfolios that were the lifeblood of many active managers have been largely abandoned.

This shift, of course, reflects genuine concerns about the costs and efficacy of active management. Market innovations have allowed investors to purchase two components of equity returns — broad market exposure and factor exposure — fairly cheaply.

However, there could be an opportunity cost to pay in a world of low returns. In a subdued market environment, high-conviction strategies have an important role to play in an equity allocation to achieve above-benchmark returns. By rethinking how various types of high-conviction strategies are chosen and deployed, we believe, investors can discover better ways to make their equity portfolios work harder. What’s more, identifying strategies that demonstrate persistent conviction can help guide investors toward successful managers.

What does conviction really mean? Our definition of high conviction has several layers. First, a portfolio must differ meaningfully from the benchmark. Second, you need a clear investing philosophy. Third, a disciplined process is crucial. Fourth, high conviction means an ability to stand by research findings, even when the tide goes against you. At the same time, managers with conviction must also know when to step back and revisit a thesis if circumstances change.

Seen through this lens, conviction can take many forms. It’s much more than high active share, which is often considered the linchpin of conviction.

We’ve conducted research on eight types of high-conviction equity strategies, spanning income, value, quality, growth and concentrated approaches. For our study, we defined high-conviction portfolio managers as those ranking in the top 20 percent of one of these categories in the eVestment U.S. Large Cap Equity universe at least 60 percent of the time. They also had to have at least three years of reporting characteristics to qualify. From this group, we extracted managers that delivered above-median returns during the reported period. In other words, we looked at portfolio managers that consistently demonstrated commitment and skill in a specific type of investing discipline.

The results are compelling. From 2004 to 2014 skilled high-conviction equity managers outperformed the Standard & Poor’s 500 index by a significant margin (see Chart 2), gross of fees. Outperformance ranged from 1.6 percent and 1.9 percent in the value and income categories through 3 percent and 3.2 percent in momentum and high active share, respectively. Even after accounting for fees, these are meaningful premiums to the benchmark, backed by strong information ratios, which indicate attractive risk-adjusted returns.

Five of these groups are also represented in passive MSCI factor indexes. Here too the skilled high-conviction strategies delivered solid results, well ahead of the passive factor indexes (see Chart 3).

Click to enlarge.

These findings are a starting point for a broader discussion about combining high-conviction strategies to achieve a broad range of investing objectives including downside protection, sourcing income and consistent alpha and upside capture. In future blogs we will show how high-conviction strategies perform in up and down markets and how different combinations can be used to help manage volatility for specific investing needs.

There may not be a silver bullet for a world of lower returns and higher uncertainty. But, equally, the passive/active debate is not black and white. In our view, by acquiring a deeper — and broader — understanding of how to find conviction in equities, investors can create a combination of passive and active strategies that will achieve their goals.

Dianne Lob is senior managing director of equities and Nelson Yu is co-head of equities quantitative research, both at AllianceBernstein in New York.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio management teams.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indexes or any securities or financial products. This report is not approved, reviewed or produced by MSCI.