With concentration and duration risk building inside the Barclays aggregate bond indexes, fixed-income investors have been tempted to abandon the classic investment-grade benchmark. But what if, like a lot of major institutional investors today, you can’t simply walk away from the Agg? There is another way.

Ultralow interest rates are one of the most challenging trends for investors across the globe. The thirst for yield has spawned investments outside the traditional arena and led to a growing sense of unease over the possible fallout from an inevitable rate hike. For institutional investors with fixed-income portfolios anchored to the Agg, the issues are especially acute. The unprecedented policy and market developments since the 2008–’09 global financial crisis have meant that the yield of the Global Agg has fallen below 2 percent, a historical low. At the same time, duration of the Global Agg has risen to 6.52, compared with 5.3 before the financial crisis. For those invested in regional proxies such as the U.S. or Euro Agg, the picture is no better. To be sure, passive investors benchmarking to Barclays Agg indexes have reached such a boiling point that a meme has taken hold in the industry to scrap the benchmark completely: “Bag the Agg.”

In reality, it’s not so simple. To investment committees with billions of dollars’ worth of assets under management, the Agg represents the most diversified exposure to the investment-grade bond universe. But there is another option. The Agg, after all, is not only an amalgam of sleeves, or fixed-income sectors, but also a combination of factor or risk premiums. In general, investments in fixed income generate returns because of default risk, term factor premiums — that is, elevation of risk as maturity is increased — or risks surrounding the ability to freely trade an instrument. Looking at the Agg as a grouping of these risks, then extracting these premiums, can be an effective way of potentially improving risk-adjusted returns while remaining within benchmark weights.

Smart beta has gained popularity as a good marriage between passive and active management. Many investors think of smart beta in the context of equities. It turns out, though, that systematic, rules-based strategies can also be used to extract the premium in fixed income. Given the much more fragmented nature of the bond markets, however, it’s just a bit more complicated. We at State Street Global Advisors have focused on extracting the credit risk premiums in corporates and sovereigns because we think that gives us the biggest bang for our buck. Yet, even there, the rules we’ve had to construct to extract it within each of the two sleeves are somewhat different.

Source: Barclays as of June 5

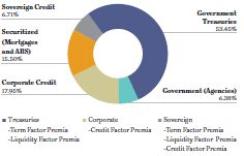

The Global Agg is made up of 60 percent government debt and just 18 percent corporate credit (see chart 1). Don’t be fooled by the smaller percentage of corporates, however. Data show a strong correlation between the corporate credit sleeve and the overall Agg.

The corporate-quality tilt is duration neutral, which is done intentionally, to avoid a duration bet that differs from what is already embedded within the index. In that sense, we are truly advancing the Agg, rather than upending it. We isolate the element of default risk premium that is pronounced within corporate credit, extract that premium and leave all other features in line with the benchmark (see chart 2).

Source: State Street Global Advisors, Barclays POINT, as of April 2014

Investors can also use the quality tilt potentially to improve the sovereign sleeve of the Agg by overweighting countries with lower sovereign credit risk and underweighting riskier economies. This process also helps to address concentration risk, which is a particular issue in the sovereign sleeve, with 53.49 percent of market cap stemming from the largest global issuers: Japan and the U.S.

To manage concentration risk, one alternative is to reweight investors around a new metric other than market cap, such as by weighing constituents by debt-to–gross domestic product. Using a sole metric to weight constituents, however — whether liquidity, market cap or equal weighting — may reduce concentration risk but inadvertently heighten other sources of risk in the asset class. Within emerging markets, a simple debt-to-GDP reweighting would place Russia at a stronger position than South Korea, resulting in greater levels of sovereign credit risk.

Historical analysis demonstrates that a smart beta quality tilt to the sovereign sleeve can potentially improve risk-adjusted returns. When applied to the Barclays Global Treasury index, for example, the tilted strategy achieved steady outperformance relative to that index from December 31, 2002, to April 30, 2015, even with fairly conservative overweights and underweights relative to the benchmark.

Lori Heinel is chief portfolio strategist, and Ritirupa Samanta is head of quantitative research and senior portfolio manager for fixed income, cash and currency; both at State Street Global Advisors in Boston.

See State Street Global Advisors’ disclaimer.

Get more on fixed income.