Long-term institutional investing, as practiced by the world’s leading sovereign wealth funds, enjoys large strategic and tactical advantages:

• It allows for fundamental themes to fully develop.

• By taking positions with high potential payoffs despite possibly uncertain timing, the strategy both shapes the future and profits from it.

• The long view, coupled with ample resources, can exploit tactical opportunities created by short-term investors under pressure from liquidity demands.

• More broadly, a long-term strategy stands to benefit from mispricings arising from errors in valuation and elevated risk aversion.

• The ability to absorb liquidity risk inherent in unlisted and illiquid assets can generate a premium return.

These advantages have rarely mattered more than in the current environment of low yields, mounting volatility, unexciting global economic growth and subpar investment returns — nor have they contrasted more sharply with the prevailing transaction-oriented mentality. Yet today, as much as ever, long-term investors can and should access the full range of long-term nonpublic assets — value-added real estate, private equity and private debt — to diversify their holdings, mute the volatility of the public markets and earn steady and favorable risk-adjusted returns.

The contrast between transactional markets and the breadth of opportunity open to long-term strategies suggests that investors across the entire institutional spectrum — pension plans, insurers and endowments — should give the approach serious consideration.

Unlike some of their institutional peers, sovereign wealth funds have the advantage of rapidly growing assets under management — projected to eclipse the $10 trillion mark by 2020, compared with roughly $7.5 trillion today. But it is time horizon — not portfolio size — that sets a long-term investor apart. Although many long-term opportunities, particularly in illiquid and nonpublic markets, are better suited to large pools of capital, the long-term mentality can apply across the investment spectrum.

Conventional wisdom ties market cycles to economic cycles, which last an average of nearly five years. One of the most successful institutional investors, Singapore’s sovereign wealth fund GIC, places market cycles in a similar time frame. Discussing GIC’s investment practices, CIO Lim Chow Kiat has stated that “the minimum time horizon for performance measurement is five years.”

Paring down the definition of long-term investing still further not only dispenses with considerations of portfolio size; it also subordinates the time criterion. In the words of Lim, “It is actually not the time horizon that matters most, but rather the mind-set and discipline.” This mind-set implies two long-term prerequisites: first, that anticipated near-term liquidity needs are a controlled and manageable proportion of total portfolio values; and, second, that investors have not only the financial capacity to withstand the inevitable intracyclical drawdowns but also the political will and emotional aptitude.

The most recent five-year records of eight large SWFs give an idea of the lift alternative assets have provided in the environment coming out of the 2008–’09 financial crisis. According to our research at J.P. Morgan Asset Management, the median allocation to alternatives among the eight funds amounted to 18.5 percent of the total portfolio. Returns for the funds with above-median allocations beat the conventional 60-40 allocation return by 551 basis points and beat the returns of the below-median funds by 316 basis points annually. The top four performers among the eight SWFs, with alternatives allocations ranging from 16 percent to more than 35 percent, with a mean of 26 percent, beat the benchmark by an average of 671 basis points (see chart 1).

Alternative Allocations Have Boosted SWF Performance Since Financial Crisis

Source: Latest available (as of June 2015) reported five-year annualized returns from the websites of this selection of eight notable sovereign wealth funds. 60/40 portfolio represents annualized return between 2009 and 2014 of a hypothetical portfolio consisting of 60 percent MSCI ACWI equity index and 40 percent Barclays global aggregate index; data from Bloomberg.

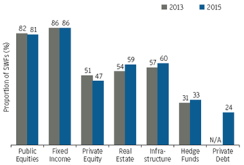

Although SWF allocations to infrastructure have been increasing, the Organization for Economic Cooperation and Development commented in a recent working paper, “Institutional Investors and Infrastructure Financing,” that “in principle, institutional investors should be natural investors in infrastructure ... but allocations are generally low,” noting that less than 1 percent of the world’s pension funds had invested directly in infrastructure (see chart 2).

SWFs Invest in Infrastructure

Source: Cambridge Associates, Lipper, J.P. Morgan Asset Management; data as of December 31, 2014.

Over a sufficiently long investment horizon, the odds favor the success of many investments. As time horizons shrink, market factors increasingly enter into target return calculations. Bid prices may rise so high that assets may not realize the desired gain over any reasonable time frame. By contrast, assets overlooked in the rush of conventional investors to capture a current fashion — or to sidestep a current dislocation — may stand to reap all the premiums on offer: risk, liquidity, lockup, first mover, distress and so on.

Such assets come with challenges of their own, however. Since the 2008–’09 financial crisis, the emphasis on mark-to-market valuation in accounting and regulation has raised the price of patience — for pension funds especially. And even as long-term investors must look past transient volatility to a distant time horizon, they need to remain sensitive to the near-term opportunity — when a flood tide of enthusiasm lifts the value of their positions to their price target or simply when another opportunity comes along that will improve the calculus of risk and reward in their portfolios overall.

Perhaps the gravest threat to the long-term strategy may arise from the shortsightedness of stakeholders who stand to benefit most. “Mark-to-peer pressure” can undermine the rationale for the soundest contrarian investment, especially in the early years of staking out a first-mover advantage when short-term investors are posting better results. This threat is pervasive, and it spotlights an aspect of the discipline no long-term investor can afford to ignore. Thorough education, plus open, frank and frequent dialogue with stakeholders, is essential to staying the frequently arduous course that leads to superior returns.

Patrick Thomson is global head of sovereigns and head of institutional business in Asia (ex-Japan), Australia, the Middle East and Africa, at J.P. Morgan Asset Management in London.

Get more on pensions and on sovereign wealth funds.