“Keep calm and carry on,” reads a popular World War II–era British motivational poster and Facebook-era Internet meme. We think the first half of the slogan is good advice for bond investors in today’s uncertain markets. But we at AllianceBernstein would adjust the wording slightly and substitute the second half of the catchphrase with “go global.”

As we’ve noted before, bond investors around the world tend to harbor a strong home bias, that is, a preference for domestic over foreign assets. This inclination shows up in many core bond portfolios, which aim to provide investors with stability and income by focusing on investment-grade debt and holding a healthy share of government bonds.

Our research, however, suggests that global bonds have offered historical returns comparable to domestic ones — and with considerably lower volatility. What’s more, varied global exposure offers investors diversification of interest rate and economic risk. As business cycles, national growth rates, monetary policies and yield curves around the world diverge, this is a key allocation strategy.

But adding global isn’t just a tactical move for dealing with uncertain market conditions. A hedged global bond portfolio that strips out currency volatility can meet an investor’s core objectives of stability, income generation and diversification against equities. In other words, the ideal core portfolio should, by definition, be global.

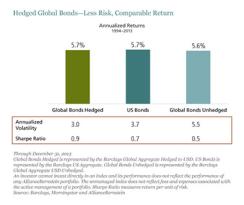

When looking at the three-year rolling standard deviations of three different bond strategies — a hedged and an unhedged global approach and a U.S.-only approach — over the past two decades, we found that the unhedged strategy was considerably more volatile than the one completely focused on the U.S.

But here’s the part that may surprise some people: It was the hedged global strategy that had the lowest volatility of all. And investors did not have to sacrifice returns in the bargain. In fact, our analysis shows that returns over the period were about the same for all three strategies. But risk-adjusted returns were highest for the hedged global approach (see chart).

A global approach also offers protection when U.S. bonds stumble. A review of quarterly returns between 1990 and 2013 shows an average 2.4 percent return when the Barclays U.S. Aggregate Bond index, also known as the Agg, was positive. The hedged global aggregate performed nearly as well, capturing 94 percent of those gains. We call this the up capture.

The down capture was a different story, however. To be sure, when the Agg was negative, the hedged global aggregate was also negative. But its down capture was just 67 percent. In other words, we found that the hedged global approach captured nearly all the returns of the Agg during positive quarters but only about two thirds of its average quarterly loss.

Over the years those investors who shifted away from the U.S. and toward countries where rates were either rising more slowly or falling preserved more of their capital. That may be worth keeping in mind if, as expected, the U.S. Federal Reserve is one of the first central banks in a developed market to start raising policy rates in the year ahead.

Finally, we found something similar when looking at correlations. Since 1970, U.S. Treasuries have shown a low correlation to U.K., German, Italian and Japanese sovereign bonds. And the correlations were in many cases lowest during extremely negative months for Treasuries. In the case of German Bunds, Treasuries fell by nearly two thirds during those months.

Of course, there are risks associated with global bonds, as there are with all investments and strategies. As we’ve seen, an unhedged global portfolio can be highly volatile and carries heightened risk because of its currency exposure. Investors also need to decide how global they want their core portfolio to be. These issues will get a closer look in upcoming posts.

We understand that these are tense times for investors. Stretched valuations, increased volatility and the specter of rising interest rates have many on edge. But fear can be a great catalyst. And when it comes to bonds, this may be a perfect time for investors to go global.

Douglas Peebles is chief investment officer and head of fixed income at AllianceBernstein in New York.

See AllianceBernstein’s disclaimer.

Get more on fixed income.