I have been traveling to Brussels, London, Milan, Paris and Berlin for many years, but lately I have focused on Europe’s periphery: Think Dublin, Lisbon and Madrid. Through these visits I have come to appreciate that there is a specific playbook for understanding the life cycle of investment opportunities in Europe’s recovering economies, and it differs materially from the playbook for assessing a country like Germany or the U.K.

The divergence across Europe’s various economies — the periphery in particular — has become even more pronounced since 2010. As a result, we believe that an investor risks overpaying for an asset or buying an asset too early if he or she does not fully appreciate where each country is in its economic life cycle.

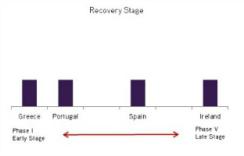

So, to help us better understand the periphery, KKR recently developed a macroframework for assessing investment opportunities in these more troubled countries, such as Spain, Ireland, Portugal and Greece. Our framework identifies five phases in the renewal process, which break down the opportunities into a sort of macroeconomic timeline, as follows:

— Phase I: Investors should focus solely on local export companies that benefit from a recovery in global growth and avoid traditional consumer stories.

— Phase II: Migrate toward companies that sell into capacity-constrained exporters (and the real estate required to build out capacity).

— Phase III: Move toward import substitution stories as the export value chain vertically integrates.

— Phase IV: Find less cyclical consumption stories that benefit from some form of economic recovery. Trade-down/substitution stories should work nicely, too, but remain cautious on traditional cyclical consumer stories.

— Phase V: Finally, focus on companies that are levered to falling unemployment or benefit from hypercyclical industries like advertising, etc.

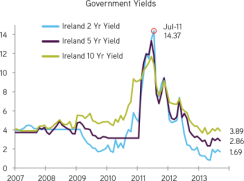

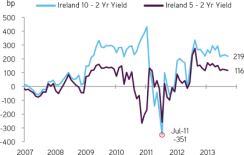

In terms of specific countries, our research leads us to believe that Ireland is probably the peripheral economy that has transitioned its economy from Phase I to Phase V. Exports in such areas as health care, technology and agriculture are now booming, and house prices in Dublin are up 11 percent year-on-year. That is the good news, particularly for consumer cyclical sectors of the economy. The bad news is that the country is now flush with capital, and as a result we see lower return profiles for opportunistic capital, particularly compared with Phases I-III (see charts 2 and 3). We note that, as a proxy for investor perceptions of Ireland, Irish government bond yields have collapsed, falling to below 4 percent from about 14 percent in July 2011.

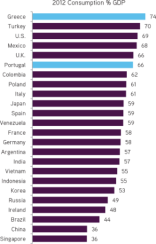

Spain’s outlook is more complicated. On the one hand, the previous focus on exports during Phase I of recovery has gotten a bit stale. We originally wanted to avoid consumption-oriented investments and focus on export-related stories. Key to our thinking was that an investor could get globally competitive companies domiciled in Spain at discounted Spanish equity prices with upside to both margins and improved financing costs. After our latest visit in the summer of 2013, however, it seems that the consensus — and all the capital that typically follows the consensus — is now extremely focused on export-related stories, making this area of the market less attractive on the margin.

On the other hand, we think that there are two important positive knock-on effects from a robust export cycle worth considering in Spain, which we consider to be in Phase III of our recovery framework. First, many Spanish exporters are running out of capacity. To put this in context, consider that investment in Spanish machinery and equipment has declined by almost 22 percent since 2008, and now amounts to just 5.7 percent of GDP. As a result, Spanish exporters are being forced to play catch up by finally reinvesting in their businesses. For a country that may endure another 7 percent decline in overall fixed investment in 2013, this pocket of strength is notable. Second, as Spanish companies become more competitive exporters, they are bringing more of the intermediate goods assembly in-house via vertical integration. Not surprisingly, this initiative could mean more jobs, more investment and more efficient Spanish exporters.

Meanwhile, our research still leads us to believe that Portugal and Greece have not had enough economic momentum for folks to move past Phase I or Phase II investment considerations. True, overall exports have grown, but the knock-on effect to related industries there has been noticeably more muted than in Spain or Ireland. Moreover, high unemployment and a weakened government sector likely mean more weakness in consumer cyclical industries, including traditional media.

Our bottom line: The periphery appears to be recovering, but knowing where and when to deploy capital is becoming increasingly important. The good news is that there is still not enough foreign direct investment in many of these countries, nor is there enough bank capacity in many instances. As a result, we believe there is opportunity for investors with strong knowledge about refinancing and recapitalization options, particularly those with a local presence.

Henry H. McVey is head of KKR’s global macro and asset allocation team.