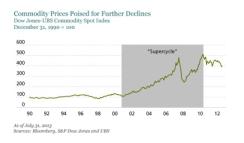

Commodity prices soared during the first decade of this century. But now the party is over. New sources of supply are coming online just as demand from China is slowing, leading to expectations of price declines.

Should investors shun commodity-related investments? We don’t think so. Still, the new environment will require that investors take a more focused approach to extract commodity returns.

From 2001 through 2010, commodities posted double-digit price increases year after year, with only a brief pause during the global financial crisis. Those days are over. Decades of underinvestment, along with China’s unexpectedly strong emergence, drove the so-called supercycle, which has now given way to new dynamics.

Today significant investment combined with China’s growth slowdown has fueled expectations of supply surpluses and spot price declines. While each commodity faces a unique supply-demand situation, the cases of iron ore and crude oil highlight how investors can effectively navigate a more challenging pricing environment.

Chart 1: Commodity Prices Poised for Further Declines

Spot iron ore prices are averaging more than $130/MT so far in 2013, but we expect them to fall toward this $120/MT marginal cost over the next couple of years. Yet despite the likelihood of falling prices, iron ore is still an attractive investment in our view.

Here’s why. Direct exposure to iron ore prices occurs through futures contracts. Today futures contracts for the average spot price of iron ore in 2016 are trading at around $100/MT. This pricing structure means that if spot prices fall to the $120/MT marginal cost and stay there for all of 2016, an investment in the 2016 futures contract at current levels will produce a 20 percent gain. The investment would only lose money if spot prices average less than $100/MT in 2016, which the consensus believes but which our analysis suggests is highly unlikely.

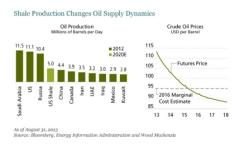

Crude oil also faces oversupply concerns. The application of hydraulic fracturing and horizontal drilling to shale formations, commonly known as fracking, is revolutionizing the crude oil supply picture. In the U.S. alone, crude production from shale is expected to reach 5 million barrels per day (bpd) by 2020; that’s more than the current total production of any other country except Russia, the U.S. and Saudi Arabia (see chart 2). What’s more, this and other marginal sources of supply are profitable at an oil price of $85 per barrel (bbl). Modest cost inflation brings the break-even cost to around $95/bbl by 2016.

With spot Brent crude oil prices currently averaging about $110/bbl, we expect prices to fall toward the $95/bbl marginal cost over the next few years. This $95/bbl level also happens to be the 2016 futures price for Brent crude. We think this creates an interesting opportunity to benefit from potential price shocks with relatively little downside.

Chart 2: Shale Production Changes Oil Supply Dynamics

The downside is limited because we believe the $95/bbl cost is more a floor than a target price. Shale well producers are able to quickly curtail production if oversupply pushes prices to uneconomic levels. In the event oil is abundant, the 2016 futures are unlikely to appreciate but they are also unlikely to fall in value.

In fact, the 2016 futures stand to benefit significantly in the event that oil prices rise above $95/bbl because of supply disruptions, geopolitical risk or general cost inflation. Furthermore, such inflationary shocks would likely hurt most equities and fixed-income investments. In our view, this makes 2016 oil futures quite attractive from an overall risk-return perspective.

These examples show how investors can seek to generate returns from commodities with ample medium-term supply and likely declines in spot prices. Meanwhile, other commodities such as copper and natural gas, with different supply and demand dynamics, should see spot price increases, though perhaps not on the scale of those of the past decade.

While each commodity has a unique profile, there is a common denominator: Commodities in general tend to perform well during inflation spikes, when both stocks and nominal bonds often face headwinds. Even after the supercycle, this remains the most important role for commodities in an overall portfolio allocation.

Jon Ruff (pictured) is lead portfolio manager and director of research for real asset strategies at AllianceBernstein. Seth J. Masters is chief investment officer of Bernstein Global Wealth Management, a unit of AllianceBernstein.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AllianceBernstein portfolio-management teams.