In 1973, the venerable boutique investment bank Kuhn, Loeb & Co. developed what many consider to be the first bond index. In time, the Kuhn Loeb index would come to dominate the industry, and would later be known by its more famous moniker, the Lehman Brothers aggregate bond index, or simply the Agg, after Lehman merged with the small firm in 1977. The index was taken over yet again by Barclays Capital in 2008 following Lehman’s collapse, and it then adopted its latest name, the Barclays aggregate bond index.

The Agg is a U.S. market-cap-weighted, investment-grade, fixed-income index. As such, it can be thought of as a passive taker of debt issuance. That is to say, the duration profile and issuer concentration of the Agg is in large part dictated by the preferences of the issuers themselves, a fact that presents some special challenges to fixed-income investors today. In particular, the 2008 financial crisis and subsequent monetary policy responses led to significant changes in the sector composition and duration profile of new issuance in the Agg, which led the index’s duration to extend and its yield to compress. In essence, investors in Agg-based mandates are taking greater duration risks for lesser-yielding rewards in the present than in the past.

As a result, a wide-ranging debate has been happening in the investment community regarding the best manner in which to respond to the historically stretched risk-reward profile that fixed-income investors now face.

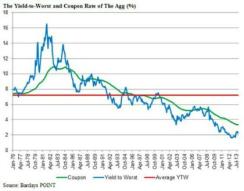

It is commonplace today to associate the Agg’s strong performance track record with the U.S. bond market rally that started in October 1981. A simple performance attribution portrays a different story, however. While the Agg’s annualized total return of 7.94 percent from the start of 1976 through October 2013 is quite impressive from an absolute (and risk-adjusted) return basis, comparatively little of that return can be ascribed to bond price movements. Indeed, when dividing the Agg’s total return into its contributions from coupon and price returns — leaving aside other, very minor, return factors — it becomes evident that the annualized coupon return represents the vast majority of the index’s total return.

In August 1988, Barclays introduced the concept of so-called excess returns. Excess returns represent the embedded risk premium in fixed-income securities, while the remainder is driven by movements in the U.S. Treasury yield curve. Using this framework, fixed-income security returns could be distinguished by two primary drivers: returns due to duration exposure and returns due to excess risk. Historically, the excess return component of the Agg’s performance has been negligible by the index publisher’s own calculation. Given the Agg’s high sensitivity to interest rate risk and the present historically low yield levels on offer, where does this leave Agg-based investors?

Interestingly, while interest rates are near historical lows, the recent total-return volatility of the index has not trended lower in lockstep as rates have dropped. Formulated another way, the Agg’s risk is fairly close to its long-term average but the reward that can be expected to derive to investors tracking the index, as approximated by its yield-to-worst, stands well below its long-term average, as shown in chart 1.

One might think that historically low absolute yield levels and the associated low levels of compensation awarded for bearing duration risk might portend for reduced demand for fixed-income assets overall. Many investors, however, use fixed income to diversify their risky, or equity-like, asset exposures. The Agg has been a particularly useful tool in this regard, as its returns since inception have been only modestly — and, often, negatively — correlated to equities. To multiasset investors, therefore, assessing the risk-reward trade-off of owning fixed-income on a stand-alone basis perhaps holds less weight than its diversification benefits across their overall portfolios.

Still, the asymmetric risk-reward present in the Agg makes the index less attractive to many investors than in past periods. What could investors hold in its place? Any compelling alternative to the Agg should offer a stable income stream at an equal or higher coupon-yield level than offered by the Agg, but without such a pronounced overweight to duration risk. In other words, the present market environment calls for greater balance of exposures to fixed-income risk factors that are not significantly captured by the Agg.

Chart 2 shows the fixed-income assets we expect to outperform under specific scenarios of rising, falling or stable growth and inflation. This table illustrates that holding a broad range of assets in a passive portfolio can be a preferable way to yield a steady return, independent of the economic environment, given the likelihood of Agg underperformance in a high growth and inflation context. Additionally, it is important to note that the red outline on the chart roughly represents the economic environments covered by the Agg’s sector composition (high-carry products represent a variable component in the Agg). That is, the Agg’s component sectors are not particularly well suited for periods of rising inflation or growth, which can make the benchmark a challenging fit for longer-term asset allocations in those environments.

To elaborate on this point, one can think of these fixed-income assets as belonging to two families, one of deflation-hedge investments (cash, nominal bonds, investment-grade corporate bonds, agency mortgage-backed securities) and one of pro-growth investments (high-yield corporate bonds, high-carry assets, inflation spreads). The argument for holding a diversified portfolio of such assets is further reinforced by the historical steady and negative correlation between these pro-growth and deflation-hedge securities. As suggested by chart 2, the Agg would likely underperform in a rising-rate environment, whether in nominal or real terms, and it would similarly underperform in a stagflation scenario.

As a result, BlackRock advocates a portfolio with a balanced risk profile where the interest rate risk is limited to approximately half of the total portfolio risk contribution, with the remaining half deriving from spread risk. As duration and spread factors tend to be negatively correlated, such asset allocation leads to lower risk at the portfolio level. We can reasonably expect the corresponding portfolio to exhibit more stable performance through various investment regimes against any nonbalanced alternative. A more comprehensive look at this topic will soon be available in forthcoming issues of BlackRock’s By The Numbers: Perspectives on Capital Markets, to be found on the firm’s institutional market commentary web page.

Of course, there are other solutions to the Agg’s historically low risk compensation and limited upside; some propose moving capital to short-duration mandates, and others may decide to allocate to more active and opportunistic total return strategies. Yet these solutions are fundamentally different from either maintaining Agg-based exposure and hoping for the best, or the balanced alternative beta option outlined above. For investors explicitly seeking fixed-income beta that can solve the dilemma posed by the Agg, balancing risk factor exposures through an alternative beta is a very sensible solution and attractive alternative.

Mike Rierson is the head of research, model-based and index portfolios for BlackRock’s fixed-income group.

Read more about fixed income.