Local currency emerging-markets debt stands out as a poor performer thus far in 2014, against a generally favorable fixed-income landscape. The rally in U.S. Treasury yields— the ten-year Treasury stands 26 basis points below its year-end level— has generated positive returns across the bond landscape. The Barclays U.S. aggregate bond index has returned 1.5 percent year to date, with investment-grade corporates up 2.2 percent and high-yield posting a gain of 2 percent. Even sovereign U.S. dollar–denominated emerging-markets debt has eked out a 0.5 percent increase despite a spread widening of 32 basis points, thanks to the carry and the move in Treasuries. By contrast, local currency emerging-markets debt, as shown by the J.P. Morgan government bond index–emerging markets (GBI-EM global diversified) index, has lost 1.9 percent since the start of 2014.

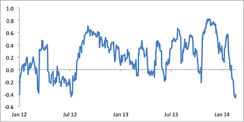

Local currency emerging-markets debt contrasts with the other asset classes mentioned because of its lack of a Treasury component. Its yields thus do not depend directly on a global risk-free rate but instead on local policy rates and yield-curve slopes. Whereas all-in yields in most fixed-income markets have fallen this year, the GBI-EM yield has risen 19 basis points. This outcome is the inverse of what happened in mid-2013, when U.S. Treasury yields increased sharply as the U.S. Federal Reserve signaled it would begin tapering at some point in the coming months. Emerging-markets yields moved up in tandem with Treasuries as investors feared decreased availability of capital flows to developing countries. The correlation between daily changes in local yields and Treasuries jumped. This time around, local yields rose even as Treasury rates dropped (see chart 1). Recent stress in emerging markets, which has caused local yields to rise, has likely helped push Treasury yields lower on a flight-to-quality trade.

Has the sell-off led to value in overall emerging-markets local currency debt? At first glance, the answer appears to be no. Chart 2 shows the relationship between GBI-EM and Treasuries, with the latter adjusted to incorporate emerging-markets credit risk via the incorporation of the average five-year spread in emerging-markets credit default swaps. Although imperfect, this comparison has proved useful in the past. The chart suggests that the recent rise in local currency yields has largely matched the increase in credit risk. The spread between the two series presently stands at 95 basis points, just below the 100-basis-point line that historically tends to indicate richness. On five out of the six occasions since 2007 in which the gap has narrowed below 100 basis points, the GBI-EM showed negative returns in the subsequent three months.

This broad-brush approach, however, overlooks two unusual aspects of the current market. First, although credit risk has gotten worse, the lion’s share of the move has occurred in weaker, high-yield emerging-markets sovereigns that are not heavily represented in the local debt universe. Spreads on Argentinean, Ukrainian and Venezuelan dollar bonds have each blown out by more than 150 basis points this year. Among investment-grade sovereigns — the pool from which the GBI-EM is primarily drawn — spreads have risen a gentler 12 basis points (see chart 3). In other words, the rise in the overall emerging-markets credit default swap spread likely overestimates the increase in credit risk associated with GBI-EM issuers.

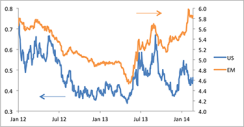

Second, the spread between the GBI-EM yield and credit-adjusted Treasuries exists in large part to compensate investors for the currency risk they assume in buying locally denominated securities. The sell-off in emerging-markets foreign exchange has improved valuations on that front and has likely reduced the risk associated with further depreciation. With recent emerging-markets forex weakness having come on top of fairly large moves in 2012 and 2013, in nominal terms emerging-markets currencies stand only marginally stronger than at their weakest point during the 2008–09 financial crisis (see chart 4). Moreover, central banks have responded to currency pressure by pushing up policy interest rates, which has contributed to the rise in longer-term local yields. With local short rates having jumped at a time when U.S. rates have fallen, the implied carry attached to emerging-markets currencies has risen significantly (see chart 5). This central bank support has succeeded in stabilizing currencies in emerging markets. Local rates drifted lower during the middle two weeks of February.

The differentiation between investment-grade and high-yield emerging-markets credit quality and the probable drop in currency risk following emerging-markets forex depreciation and policy interest rate hikes mean that local currency debt likely holds greater value than simple historical metrics would imply. Caution is still warranted at the level of the overall index, however. Currency depreciation and weak growth have gone some way to narrowing imbalances in some major emerging markets, such as India and Indonesia. But in other major components of the GBI-EM, such as Brazil, South Africa and Turkey, external deficits have yet to improve. Additional currency depreciation — or tighter local monetary policies, with negative implications for longer-term yields — may be required. For the time being, local currency emerging-markets debt likely represents an opportunity to be selective more for active fixed-income managers than for index investors. A bit more currency weakness, a further backup in yields or evidence of better external finances in a broader group of issuers would widen its appeal.

Michael Hood is a market strategist for J.P. Morgan Asset Management.

See J. P. Morgan’s disclaimer.

Read more about emerging markets.