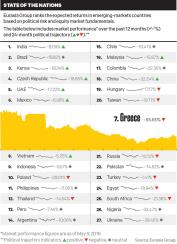

Since Greece’s debt woes burst into the open at the end of 2009, the crisis has seemed to spike each spring as predictably as the return of tourists to the Aegean Islands.

Last year the Syriza government of Prime Minister Alexis Tsipras played brinkmanship with the so-called troika — the European Commission, the European Central Bank and the International Monetary Fund — whose credit keeps the country afloat. His hardball tactics included a brief default on loans from the IMF before the European Union agreed to a fresh €86 billion ($97 billion) bailout. The economy, which had begun a tentative recovery in 2014, fell back into recession.

This year bailout funds have been on hold for months because of Athens’s failure to deliver promised economic reforms, putting the government at risk of defaulting on €3.5 billion in payments due in July to the IMF and the ECB. A standoff between the IMF, which believes Greece needs debt relief and less austerity in the short term to recover, and Germany, which has taken a harder line, hasn’t helped matters. Yet there are hints of progress. On May 9, Tsipras and his minister of Finance, Euclid Tsakalotos, persuaded parliament to enact pension cutbacks and an increase in the solidarity tax to boost the primary budget surplus (before interest payments) to 3.5 percent of gross domestic product, a target set by the Eurogroup of Finance ministers. That same day Finance minister Wolfgang Schäuble gave the first indication that Germany would support debt relief.

Some economists and investors see a path to recovery — if everyone can find a way to get along and get behind the bottomed-out economy.

One place to start rehabilitation is with the banks. “The banks have been uninvestable as banks,” says Mike Reynal, a Des Moines, Iowa–based portfolio manager of $245 million in emerging-markets funds at RS Investments. At the end of March, private sector loans were down 5 percent year-over-year, and loans to nonfinancial corporations were down 7.5 percent. Reynal is watching closely to see if the majors — Alpha Bank, Eurobank, National Bank of Greece and Piraeus Bank — start extending more credit. “Loans are the oil that makes the economy move,” he says.

Fabio Balboni, European economist at HSBC Holdings in London, agrees that banks hold the key to growth. “If you can get the banks in a position again to lend to the economy, you could be in a better place six months from now,” he says. Balboni doesn’t expect a dramatic turnaround, but even modest quarterly growth rates would reduce unemployment and encourage spending.

The economy shrank by 0.4 percent in the first quarter, slightly better than expected, which may portend a return to growth in the second half. Unemployment has been declining, approaching 24 percent — the lowest level since 2012 — but that rate is still more than double the EU average.

In addition to pleasing the troika, Greece could benefit from imitating some of the EU countries that have managed strong recoveries, such as Ireland and Spain. Essential to their turnarounds has been their ability to attract foreign direct investment, something Greece has largely failed to do.

“Greece has assets that with privatization could actually speed up the rate of growth significantly,” says Balboni. For this to work, though, the government has to be truly invested in reform.

“Greece’s advantage is going to be linked to tourism and services,” predicts Reynal. Tourism accounts for approximately 18 percent of GDP, according to the World Travel and Tourism Council. The government hasn’t taken sufficient advantage of the tourism potential, Reynal says, but he expects it to focus on this sector once it reaches an agreement on the next tranche of bailout funds.

The troika and the Greeks may quarrel on terms, but all parties agree that another bailout should be coming soon. “The fact that you don’t have one voice to impose itself means it’s difficult to have a single solution,” says Reynal. Ultimately, Greece is going to have to figure out a way to move forward on its own, one step at a time. •