For Professional Investors only. Not for further distribution.

Since the Fed started hiking interest rates in March 2022, global liquidity conditions have tightened materially, bringing inflation down, but it has now raised risk of an adverse growth outcome in 2024. Markets are unprepared for this scenario and continue to assume a ‘soft landing’ –- that inflation can dissipate without harming growth prospects. However, we expect a rise in recession risk in western economies, while in eastern economies, some parts of Asia could face growth challenges but still provide diversification benefits and a relative bright spot.

In the longer run, we believe a shift to a ‘new paradigm’ is underway, with inflation and interest rates somewhat higher than during the 2010s. Our preference in this environment will be for a ‘defensive growth’ approach which includes pivoting to higher quality markets. We also suggest ‘intelligent diversification’ strategies.

A Problem of Interest

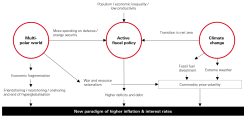

Monetary and credit conditions have tightened materially. That breaks inflation, but risks breaking other parts of the system too.New Paradigm

We are in a new economic regime of tighter money and more active fiscal policy. That means different macro dynamics, higher inflation and interest rates.

Defensive Growth

Market expectations are for a soft landing. But as the cycle slows and inflation falls, ‘bonds are back’. We focus on defensive strategies in portfolios.Read our full outlook for insights on the following:

- Economic outlook and asset class implications Our ‘house view’ is for defensive positioning in portfolios at present. That reflects what we see as an optimistic scenario priced into markets versus our concerns over elevated risk of recession and further disinflation.

- Answers to ‘top-of-mind’ questions Discussion on hedge fund performance during periods of stress, the impact of US rates on emerging markets, tactical stock/bond allocations and expectations for responsible investment.

- Refinancing the ‘Covid maturity wall’ Opportunistic funding at low rates during and just after the pandemic created a ‘maturity wall’ in 2024 and 2025, which could create refinancing difficulties at the higher rates now prevailing.

- The value anomaly in European equities Comparing the relative valuation of value and growth stocks over the last two decades reveals that value is now 30 per cent cheaper than it was, while growth is over 50 per cent more expensive.

- Intelligent diversification through thematic allocations We think new sources of diversification will be needed as part of a new investment paradigm that poses challenges to both equity returns and the role of traditional diversifiers.

Watch the Outlook Webinar Recording.

Learn more about HSBC Asset Management.

For professional investors and intermediaries only. This document should not be distributed to or relied upon by retail clients/investors.This commentary provides a high level overview of the recent economic environment, and is for information purposes only. It is a marketing communication and does not constitute investment advice or a recommendation to any reader of this content to buy or sell investments nor should it be regarded as investment research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination.

This document is prepared for general information purposes only and does not have any regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive it. Any views and opinions expressed are subject to change without notice. This document does not constitute an offering document and should not be construed as a recommendation, an offer to sell or the solicitation of an offer to purchase or subscribe to any investment. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. HSBC Global Asset Management (Hong Kong) Limited (“AMHK”) accepts no liability for any failure to meet such forecast, projection or target. AMHK has based this document on information obtained from sources it reasonably believes to be reliable. However, AMHK does not warrant, guarantee or represent, expressly or by implication, the accuracy, validity or completeness of such information. Investment involves risk. Past performance is not indicative of future performance. Please refer to the offering document for further details including the risk factors. This document has not been reviewed by the Securities and Futures Commission. Copyright © HSBC Global Asset Management (Hong Kong) Limited 2023. All rights reserved. This document is issued by HSBC Global Asset Management (Hong Kong) Limited.