By Blu Putnam & Erik Norland, CME Group

AT A GLANCE

- Difficult-to-quantify uncertainties can create an environment where certain types of event risk have an elevated probability

- The critical point to appreciate with event risk is how differently markets trade when under its influence, and therefore how risk management approaches must adapt.

The confluence of major transitions in the global economy is changing the nature of risk and how it is managed.

Key features that are shifting gears include the Federal Reserve, European Central Bank and many of their peers now fighting inflation with elevated interest rates; geopolitical tensions stemming from Russia-Ukraine and China-United States relations; global warming creating more powerful storms and periods of extreme heat and drought; and severe headwinds from shifts in demographic patterns in many aging industrial economies. Not only do these transitions have the potential to increase volatility in some markets, they are also highlighting the differences between difficult-to-quantify uncertainties and relatively more quantifiable known risks.

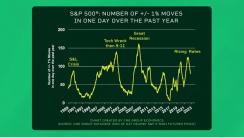

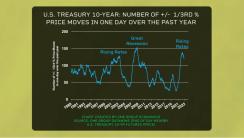

As these various themes collide in the markets, there are likely to be more days with exceptionally wide intraday price swings. That is, there may be wider price swings than typical, as measured by daily standard deviations. Also, markets may experience an increased number of large price gap days where the price makes an abrupt, sharp move up or down than would have been suggested by the elevated daily standard deviations used in traditional volatility analysis. Against this backdrop, we want to think about how volatility is typically measured, the day-to-day standard deviation of the percent change in prices; that is, daily returns, compared to probabilities of a price gap risk that complicates and changes volatility analysis.

We interpret the changed nature of volatility using the classic distinction Professor Frank Knight made in the 1920s in his book “Risk, Uncertainty, and Profit.” In economics, ‘Knightian uncertainty’ is extremely difficult to quantify, while typical volatility involves relatively well-understood risks around which we can utilize traditional metrics, such as the standard deviation. With a heightened sense of uncertainty coming from simultaneous and major global transitions, the changing nature of risk and volatility makes sense, even if it also makes risk management more difficult and complex. And just because measuring something is now more difficult does not mean that one can avoid managing the risk. Indeed, active risk management becomes more critical than ever for financial success.

Our central hypothesis is that elevated, difficult-to-quantify uncertainties create an environment where certain types of event risk have an elevated probability. In this analysis, event risk is defined as an environment in which there are at least two different scenarios with strikingly different potential outcomes. For example, the U.S. has a recession (i.e. lower bond yields) or modest growth continues (i.e. higher bond yields). Other potential event risk examples might involve up/down oil prices given OPEC or Ukraine and China uncertainties, or an up/down Japanese yen given any possible policy shifts by the Bank of Japan.

The critical point to appreciate with event risk is how differently markets trade when under its influence, and thus how risk management approaches must adapt. Once market participants focus on the event risk scenarios with two strikingly different outcomes, what gets highlighted are changes in the probabilities of the two different outcomes. That is, market participants view newly received economic data through the lens of how it might change the scenario probabilities.

Let’s take an illustration from U.S. interest rates to clarify this concept of how market participants might view economic data differently in an event risk environment. In traditional interpretations, a fall in headline U.S. inflation from 9% in June 2022 to 3% in June 2023 might lead to expectations of lower short-term interest rates and longer-term bond yields. In an event risk situation, such as the summer of 2023, where the focus was on the probability of whether the Fed might lower interest rates, the improvement in headline inflation was not relevant to market participants. That’s because the Fed was known to be watching core inflation, which was barely declining, and the labor markets, which were still quite robust. Data about the unemployment rate was more important than headline inflation. The sustained unemployment rate below 4% tilted the probability against a recession and suggested that core inflation could remain well above the Fed’s 2% target for an extended period despite the elevated fed funds rate and an inverted yield curve. In the summer of 2023, the flow of new data suggesting the “no-recession” scenario was gaining more traction, raising probabilities that the Fed would keep rates elevated longer than previously anticipated by market participants, and longer-term Treasury bond yields rose.

An interesting side note in event risk environments is that in some cases, measured market volatility actually decreases in the period before the outcome of the event is known. This can occur because the probabilities associated with the two different outcomes may be stable, at least temporarily. It is when the probabilities are on the move that market volatility tends to rise, and when probabilities are shifting, there is an elevated possibility of sharp, abrupt price moves reflecting the new event scenario probabilities.

What all this means for risk management is the shift in focus to the possibility of abrupt price moves, which could occur in either direction. Nondirectional price gap potential favors the use of multi-leg options approaches, such as straddles or strangles. By comparison, futures are the favored risk management tool when the risk management concern is mostly about a price move in a specific direction.

This distinction of when to use futures or options is heightened by an appreciation that traditional options valuation models, such as Black-Scholes-Merton, specifically assume that price gaps do not exist. Risk management approaches, such as delta hedging, which are based on Black-Scholes-Merton models, may not work well when the probabilities of abrupt price moves are elevated. Thus, in the context of Frank Knight’s ideas about risk and uncertainty, when there is an increase in difficult-to-quantify uncertainty relative to more traditional and quantifiable risks, one would expect that options trading could accelerate, especially for fixed income and equities, which has been the case for the last several years.

Moreover, elevated event risk can shorten risk management timeframes. That is, as the perceived timing of an event comes closer, trading in shorter-dated options is likely to be favored. We are seeing this in the extreme with the rising popularity of zero-day options, which also reflects the challenge of managing risk when intraday price swings can be more extreme than typically predicted by traditional volatility measures such as the standard deviation.