Key Takeaways

- The value of value relative to growth is back to historic highs, being driven by the extreme concentration of the top seven stocks in the S&P 500 Index.

- The combination of expanding equity multiples and higher interest rates in 2023 has overshadowed growing risks and created an environment reminiscent of 1987’s “Black Monday”.

- Value provides investors strong advantages in the face of these growing extremes, offering the potential for downside protection against market declines as well as compelling relative return potential on a decrease in market concentration.

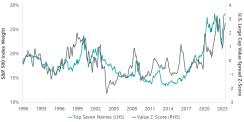

Today we have anything but a uniformly priced market. It is bearish for U.S. indexes, while providing a great opportunity to look for mispriced stocks with strong fundamentals beyond the concentrated top of those indexes. The value of value relative to growth is back to historic highs, being driven by the extreme concentration of the top seven stocks in the S&P 500 Index (Exhibit 1). Never has so much liquidity been sucked into so few stocks, and the risk may prove a black hole for capital and weigh on returns due to increased volatility from higher correlations.

Exhibit 1: Concentration and Spreads at Historic Highs: Big Seven Concentration and Value Spread

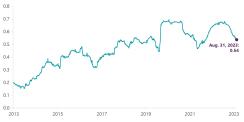

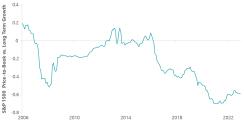

The correlation of the big seven bet is also elevated (Exhibit 2), especially compared to the rest of the market that is enjoying relatively low pairwise correlations. We are also observing an extremely low correlation between value and growth styles, which argues strongly for diversifying any U.S. cap-weighted index bets with value (Exhibit 3).

Exhibit 2: The Big Seven Show High Correlation: Average Correlation of the Big Seven Mega Caps

Exhibit 3: Growth and Value Maintain Low Correlations: Rolling Factor Correlation

The key observation is that indexes are positioned for extremely low uncertainty, reflecting a soft landing and a near-term growth boost from AI. However, what we see is that concentration in the market is being driven almost entirely by a spike in valuation multiples, despite the continued rise in real rates and the cost of capital. This is not sustainable unless interest rates come down in a benign soft-landing manner, or growth dramatically accelerates.

This combination of rising equity multiples and a significant increase in interest rates has also created the third outlier that we’ve observed: Extreme risk potential reminiscent of 1987’s “Black Monday” market crash. Between January and August 1987, equity valuation multiples increased approximately 25%. Conversely, over the same period, effective interest rate multiples (a valuation multiple derived from the difference between the initial and current yield to illustrate the attractiveness of a risk-free bond) decreased by approximately 30%. In 2023, year-to-date equity valuation multiples have expanded 39% while effective real yield multiples have declined almost 29%, a reality that is being overlooked in favor of soft-landing optimism. While we are certainly not forecasting such an event on the horizon, the similarities are too great to be ignored.

Value stocks continue to offer investors strong advantages in the face of these growing extremes, and we believe now is the best time to bet against expensive risks in highly concentrated U.S. indexes. Value stocks remain close to the cheapest levels they have ever been relative to historically concentrated long-duration growth assets and have arguably never been better index insurance. As a result, value investors have the tools to not only protect capital in the event of a market decline, but also the potential to realize compelling relative returns on any decrease in the current extreme levels of market concentration. We believe we are well-positioned for another surprise to consensus expectations, which should help the equity market become a little less extreme. In the meantime, we are comfortable waiting for such a reversal as low correlations between value and growth can smooth the ride.