Value investing has never been for the faint of heart, but this year is proving to be especially daunting. In a market plagued by multiple crises, investors in the cheapest stocks on the market have been badly burned.

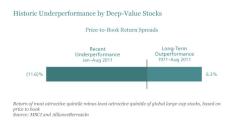

Based on price-to-book valuations, the cheapest quintile (or 20%) of our global large-cap universe has underperformed the most expensive quintile by 11.6% in the first eight months of the year ( Display ). In contrast, over the last 40 years, our research shows that the most attractively valued quintile of stocks outperformed the most expensive group by an annualized 6.3%. Deep-value stocks are in deep trouble today.

How can we explain the slump? The main reason is indiscriminate fear, which has worked against the principles of value investing that are rooted in behavioral finance.

Since markets react emotionally to bad news, investors can usually profit by analytically determining when the long-term outlook for an attractively valued stock is much better than widely believed by a nervous market. But that strategy works only if markets are capable of calming down and recognizing when they’ve overreacted. This year, a spiral of anxiety has infected the markets, and risk-averse investors abandoned stocks seen as vulnerable to economic weakness or European instability—especially those in deep-value territory. Little attention has been paid to the relative strengths and weaknesses of company-specific fundamentals.

Yet many companies are much healthier today than they were three years ago—even among the cheapest stocks. Our analysis shows that the most attractively valued quintile of global stocks had a net debt/assets ratio of 13.8% at the end of August, compared with 16.8% in February 2009. These stocks also improved return on equity to 11.9% from 4.9% in 2009 ( Display ). It’s rare indeed for deep-value stocks to have such strong balance sheets and profitability.

Many investors worry that numbers like these may be irrelevant if the European sovereign-debt crisis pushes the global economy into recession. Yet despite these fears, we’re seeing many companies improve profit margins, generate excess cash, increase buybacks and boost dividends. To me, that just doesn’t jive with the gloomiest outlooks that are now in the mainstream.

That’s why I remain a fervent believer in value investing, although I look at a broader array of valuation metrics than just price to book, coupled with an array of quality metrics, such as balance-sheet strength and return on equity. Over decades, value stocks have gone in and out of favor, with big periods of outperformance following weakness. I don’t think the cyclical nature of our investing style has really changed. It’s usually when value is most out of favor―like right now―that the greatest investment opportunities are uncovered.

In fact, our measure of the value opportunity gives good reason for optimism in the face of adversity. Price/book spreads between the cheapest and most expensive quintiles of global stocks spiked in recent months, and are now even higher than they were in March 2009. The world didn’t end then, and despite the huge challenges today, I expect markets will eventually realize that the world isn’t coming to an end now either. This psychological shift could be the trigger for value spreads to narrow, as investors stop acting purely on macroeconomic concerns and gain the confidence to reward cheap, resilient stocks with outsize returns. When that happens, I strongly believe that today’s disappointment will give way to a new deference for disciplined deep-value investing.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AllianceBernstein portfolio teams.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices, any securities or financial products. This report is not approved, reviewed or produced by MSCI. Kevin Simms is Global Director of Value Research at AllianceBernstein.