This is the first part in a three part series by Rick Rieder, Managing Director, Chief Investment Officer of Fundamental Fixed Income, BlackRock Inc.

This blog is part of a new series on Institutional Investor entitled Global Market Thought Leaders , a platform that provides analysis, commentary, and insight into the global markets and economy from the researchers and risk takers at premier financial institutions. Blackrock is our newest contributor in this new section of Institutionalinvestor.com, and will be providing analysis and insight into the global fixed income markets.

For well over a year now we have been discussing the market volatility and uncertainties surrounding the European sovereign debt crisis and over that time we have witnessed nothing but deterioration in the markets and policymakers in denial. Early on, policymakers in Europe appeared to embrace an "extend and pretend" mentality that we believe ultimately cannot succeed in resolving this trouble.

At its core, liquidity has been provided to attempt to address a solvency problem, and we do not think markets have been fooled. To use a common metaphor, European governments have become masterful at "kicking the can down the road," but we think we are fast approaching a limit to this "solution," and only by fully acknowledging the extent of fiscal and debt burdens and beginning to meaningfully address them can they turn the market tide. The most recent attempts to shore up confidence in European sovereign debt markets, with the release of the European Union's July 21st action plan, and recent ECB bond purchases, provide support to the situation, but ultimately still appear inadequate to the task at hand.

In the meantime, imbalances in current accounts and debt dynamics persist, and in some cases the problems are growing ever larger. Addressing unsustainable sovereign leverage and uncompetitive economies in Europe must happen under the constant scrutiny of the markets, as these issuers need consistent market access at manageable interest rate levels to survive, and obviously some countries have already found themselves shut out of credit markets. The economic performance of core Europe versus peripheral economies continues to diverge, as austerity and uncompetitiveness, imbalances that are slow to correct, elevated funding costs, and uncertainty, hold back the latter. These factors hold profound implications for credit selection in these markets, which in turn reduces the chances that the weaker peripherals will be able to grow into their debt levels. Indeed, even though only eight banks failed the most recent round of stress tests in Europe (5 Spanish banks and 2 Greek, among the peripherals), expectations for the test were quite low, particularly as the possibility of trouble in sovereign exposures held on banking books were omitted from the test, a glaring oversight given the Eurozone's current situation.

While the Eurozone's weakest members, such as Greece, are an obvious preoccupation, given their profoundly fragile state, our concern lies more with the mid-tier economies, such as Spain and Italy, which have also seen credit conditions deteriorate recently. With Spain, for instance, it is very difficult to gain much conviction over the size of the losses stemming from residential property market declines, but if its economy follows Portugal back into recession, we think funding the net foreign liability position will become very difficult. The situation is particularly troubling as unlike a country such as Greece, which only represents around 2% of EU-area GDP, Spain accounts for a more meaningful 11% of the region's GDP. Spain's domestic economy has shown few signs of stability, as wages and retail sales have been falling, house prices and sales volumes continue to decline, and the unemployment level has risen to an astounding 21%. Moreover, with public-sector spending set to decline further, it is difficult to see how domestic growth could drive the economy. Export segments of Spain's economy could help, as the country is a significant part of the European auto production chain, for example, but this places the country in a precarious position where it is unduly levered to global strength in auto consumption, which is hardly a given outcome, and indeed appears increasingly unlikely. While we believe the Eurozone can manage the crisis of the smaller peripheral economies, which was the focus of the July 21 agreement, if a bailout were required of a larger economy the likelihood of a very severe market dislocation could rise significantly.

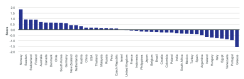

In response to shifts witnessed in sovereign debt markets in recent years, and specifically to the increased questioning of sovereign debt representing a genuine "risk-free rate," BlackRock has introduced a proprietary index that goes well beyond commonly used metrics to gauge sovereign vulnerability. The BlackRock Sovereign Risk Index (detailed in Introducing the BlackRock Sovereign Risk Index: A More Comprehensive View of Credit Quality) is one of many tools that we use to both mitigate risk in global government sector investing as well as to discern opportunities. When examining the Index's output (see Figure 1), the bifurcation between core European economies (Norway, Sweden, Switzerland, Germany), and the peripheral economies (Greece, Portugal, Italy, Ireland, Spain) is drawn in high relief. We anticipate greater levels of market volatility as the European sovereign debt crisis continues to unfold in the wake of the latest rescue attempt and it is one of the key market risks we are watching carefully.

This material is solely for educational purposes only, contains general information only and is not intended to be relied upon as a forecast, research, investment advice, or a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The information does not take into account one's financial circumstances. An assessment should be made as to whether the information is appropriate having regard to one's objectives, financial situation and needs. The opinions expressed are as of August 15th, 2011 and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources deemed by BlackRock, Inc. and/or its subsidiaries (together, "BlackRock") to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. There is no guarantee that any forecasts made will come to pass. Any investments named within this material may not necessarily be held in any accounts managed by BlackRock. Reliance upon information in this material is at the sole discretion of the reader. Past performance is no guarantee of future results. BlackRock is not responsible for any information posted on any third party websites. The information posted on any third party website does not necessarily reflect BlackRock’s views. BlackRock is not responsible for any information posted on any third party website.