Risk has risen to the top of the corporate agenda as CEOs are expected by shareholders and other stakeholders to show how they can guide a company optimally through today’s risk landscape as well as delivering on overall financial objectives.

In 2014 for example, a study* of 400 US CEOs noted that the majority of CEOs either lead the discussions on risk planning or have a strong voice in them (89%). Yet, even though risk management is the second-highest concern about the company for CEOs (following financial performance), risk planning is proactively discussed on a regular basis at just 27 percent of organizations.

The 2008 financial crisis is a likely culprit for the increased focus on risk. It resulted in increased regulation and highlighted how highly correlated businesses have become to financial (traded) markets. This, combined with a number of highly visible corporate risk events such as extreme weather and political instability, has increased complexity of risk management.

As a result, companies may have become somewhat risk averse, as testified by another CEO survey** – potentially implying a sub-optimal allocation of resources.

THREE PRACTICAL STEPS FOR A CEO TO ACTIVELY STEER FINANCIAL RISK MANAGEMENT

Risk is typically not a core area of competence for CEOs, unless operating in a financial or energy/commodity based industry. Typically a CEO delegates risk management responsibilities to finance and treasury teams who actively monitor markets and hedge risks where plausible and according to their guidelines. Complete abdication of responsibility is not advisable, however, given that the CEO is also ultimately accountable on risk to the board and the company’s stakeholders. The three steps outlined overleaf can help a CEO build a framework for relevant involvement in financial risk management.

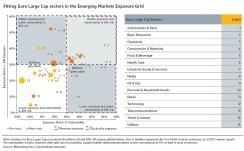

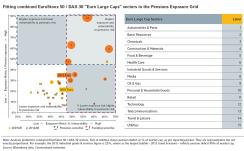

1. Finding the context for financial risk management measures: Knowing the industry’s risk profile and how peers compare to the company in market-risk terms is a good starting point. In Charts 1 and 2 below, two example Commerzbank proprietary risk measurement grids show how industries compare in their exposure (x-axis) and vulnerability (y-axis) to pensions and emerging markets (EM) risks before and after the financial crisis, respectively. From these it can be noted that Basic Resources, Industrial Goods & Services and Automobiles & Parts industries are placed in the top-right quadrant in both the pensions and emerging markets grids, indicating they are both highly exposed and vulnerable to both these risks.

Exposure in the emerging markets grid for example, is measured by % of Earnings in EM currencies while vulnerability is based on low EBITDA margin, high leverage and high correlation between businesses and EM currencies, interest rates and GDP. Being placed in the top-right quadrant whilst company’s peers reside in the lower- left quadrant would be a clear signal that a CEO needs to closely monitor the company’s EM exposures. On the other hand, being in the top right quadrant as an industry would highlight that this particular risk is very important that peers will likely be monitoring these risks closely too. The same principles apply to the pension grid although exposure and vulnerability are calculated using different metrics.

It is worth noting that exposure and vulnerability of companies and industries to both of these risks have increased since the financial crisis (as illustrated by the yellow (pre-crisis) and orange (after crisis) colored circles). This is mainly due to lower discount rates in the case of pensions, and increased internationalization in the case of EM.

Chart 1: Emerging Markets Industry Exposure Grid

2. Setting relevant Key Performance Indicators (“KPIs”) for risk management: It is sensible to set risk and cost objectives using

the same KPIs that the company’s stakeholders use in measuring the company’s performance. It is not as important to measure a risk on its own (for instance, how much interest rates could move) as it is to put this risk in the context of the corporate end-results – e.g. how much earnings could fluctuate as a result of interest rates moving by 50bps. The relevant KPIs may differ from those set for the individual teams under the CEO office (for example, for the CFO or the Group Treasurer) but ultimately all parties should focus on diminishing risk to key metrics. CEO-relevant KPIs will vary by industry and company. But they typically include earnings, return on equity and leverage, which all in different ways can be affected by exchange rates, inflation, interest rates, credit and liquidity spreads as well as commodity and equity prices.

3. Viewing risk as a resource allocation: measuring the impact of risk and hedging costs on KPIs: The beauty of financial market risk compared to other enterprise-wide risks is that it is far more quantifiable because most financial risks have a price and a price history ascribed to them. A European company looking to offset its USD-denominated dividend currency risk can in most situations find a price at which USD can be sold against EUR either immediately or in three years; similarly a UK company can efficiently hedge the sensitivity of its pension liabilities to interest rate movements.

Risk needs to be assessed in both historic perspective and through different future scenarios. Understanding how different financial market risks would have impacted the company in previous market and company cycles, is a good starting point. For example if an average earnings volatility has been 12% and currency risk has added 7% to it – of which the Russian Ruble has contributed 5% – then Russian currency risk and the cost to hedge it would clearly be worth a further analysis.

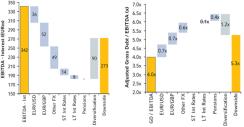

The level of potential risk can be expressed as risk attribution – see Charts 3 and 4 below. They show the measurement of risks to earnings and leverage (as observed from the longest available data-set historically) from various combined business and financial market events.

Chart 3 & 4: Financial risks to corporate earnings and leverage

Source: Commerzbank

A diversification benefit is also shown. This measures the correlation benefit from a situation where, for example in a booming economy, a company’s earnings increase at the same time as interest rates go up, thereby reducing the negative impact of a rate rise. Taking another example, if earnings from emerging markets were to drop at the same time as energy costs decline, these risks could offset each other. In 2008, the diversification benefit disappeared almost completely for most companies, and almost all risks had an additive impact on companies’ risks.

The cost of hedging is also an important element of risk assessment. The cost of hedging is variable, moving with market supply and demand as market participants take different positions on the risks that lie ahead. The balance between risk and cost at the enterprise level can be seen as the difference between having capital at hand (not hedging) to invest in other operations such as M&A or R&D and potentially as a result, having to invest (potentially much more) capital in the future to compensate for losses from unhedged risks versus hedging and paying a premium for this. The assessment of risk vs cost needs to take place concurrently.

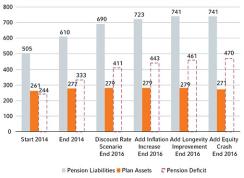

In the context of quantifying risk upon KPIs, appreciating causality (i.e. which events can cause what kind of outcomes) can help the CEO be prepared for future financial events and their impact upon the company. For example, Chart 5 below shows how a pension deficit could be affected by four different market price scenarios. An increase in pension deficit and leverage accordingly, can result from changes in interest rates, cost of credit, inflation and equity prices. Each of these can impact the company in others ways too. For example, as interest rates decline, pension deficit increases whilst cost of financial debt may decrease (depending on the fix-float mix of the company’s debt). It is good for the CEO to be aware what may cause the risk impacts seen in Charts 3 and 4 both in broad corporate and in more detailed market terms.

Chart 5: Development of pension deficit

Source: Euromoney

CONCLUSION: CEOs’ RISK STEERING MECHANISM IN PRACTICE

By having the three basics in place - putting risk in the context of peers and industry, making sure that the key metrics for measuring risk and cost of hedging are relevant to the company and its stake holders, and being aware of impact and causality of the markets upon the business – it is easier for a CEO to grasp the complexities of financial market risks and enable the steering of the business in terms of resource allocation. For example, the CEO can compare capital spent on an acquisition versus capital spent on hedging risks in the corporate portfolio in like-for-like terms, or assess the viability of an acquisition in an emerging market country in the context of the relevant risk and cost scenarios.

By implementing risk steering mechanism using the three basic principles outlined here, every CEO should have a better understanding of the impacts of financial risks to key corporate metrics, where these impacts can come from, what kind of events can cause them and how big these impacts can be. Equally, the CEO and their team can confidently assess whether the risks should be hedged away or outsourced and how much it would cost to do so.

*KPMG CEO Study “Setting the Course for Growth: CEO Perspectives” 2014

**KPMG CEO Study “Global CEO Outlook 2015: The growth imperative in a more competitive environment”

For more information, contact Corporate and Investor Solutions at Commerzbank.

Take control of market uncertainty — view Commerzbank's risk management solutions