There are many questions weighing on the minds of C-suite executives at financial companies. One of the biggest is what to do about fintech.

Financial technology companies are challenging the big banks in all sorts of areas, from financial advice to student loans, and offering novel products such as peer-to-peer lending and crowdfunding.

Bankers have recognized fintech as a real threat to their businesses for some time. From 2010 to 2015, investment in fintech ventures has grown from $1.8 billion to $22.3 billion. That momentum continued in the first quarter of this year, according to a recent Accenture report.

The question is how to deal with the challengers. Should banks collaborate or compete? The latest evidence suggests that both banks and fintech companies are deciding that the latter is a better bet.

Fintech companies are nimble and can target niche consumer areas. It is hardly surprising, then, that the most successful fintech companies are not staying small for long. Last year PayPal and Square achieved successful initial public offerings and now have market capitalizations that exceed that of many established financial institutions. Today there are 20 fintech unicorns — private companies with a valuation of more than $1 billion — operating.

The initial response to the emergence of fintech by the banking industry was either to ignore the trend entirely or develop competing technologies in-house. The evidence suggests that for many banks, the latter remains the strategy. Last year banks participated in less than 10 percent of all reported fintech deals, totaling about $5 billion, according to Accenture’s analysis of CB Insights data. This pales in comparison to the total $480 billion these institutions will spend on technology this year.

But the strategy of a head-on competition has fallen short. The banks’ legacy information technology systems are a major barrier, and hiring top tech talent for banks is difficult. Many prime candidates would rather work someplace where technology is the headliner, not a supporting role. Even at the most senior levels, banks lack leaders with significant tech experience. Accenture research found that among leading banks, only 3 percent of CEOs and 6 percent of board directors have professional technology experience. Add to that the layers of regulatory and bureaucratic complexity with which big banks must contend, and it is hardly surprising they cannot match the agility of start-up fintech rivals.

Fintech too is finding it tough competing head on. Technology start-ups usually fail because the cost of acquiring new customers is not sustainable. Investors have also become more cautious after a spate of bad news in the sector, including reports of slowing loan volumes for some fintech companies and management issues at others.

If competing is proving tough, collaboration could be a more effective approach for both parties.

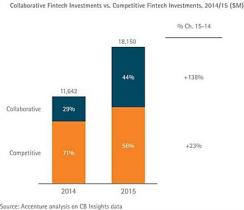

There is already evidence that collaborative ventures are gaining ground. Last year investment in fintech companies wishing to collaborate, as characterized by Accenture, with the traditional banking industry grew by 138 percent, now representing 44 percent of all fintech investment. That compares with an increase of 23 percent for fintech companies looking to compete against the banks, according to Accenture (see chart)

.

Direct investment is one option. Banco Santander, Spain’s biggest bank, participated in a $135 million funding round for Atlanta-based fintech start-up Kabbage this past October. This spring, Santander and Kabbage announced a partnership that uses the start-up’s technology to deliver fast loans to small and medium-size enterprises with Santander’s risk assessment system. In November, BBVA, the second-largest lender in Spain, took a 29.5 percent stake worth $68 million in U.K. start-up mobile-only Atom Bank.

To standardize and harmonize credit and debit card, Internet and mobile payments, PSD2, the European payment services directive, will require banks to open up data and transactions to new market entrants. In 2018 all financial institutions in member states of the European Union will need to be compliant. By opening up their own platforms, banks can allow fintech companies instant access to their huge customer bases while improving the experience for their own customers.

It is this last point that could prove critical for the future of the banks and the secret of future success for fintech.

Google (Alphabet), Apple, Facebook, Amazon and Alibaba, collectively known by the uncatchy acronym GAFAA, have reset consumers’ expectations of digital customer service. Despite some progress, banks are still struggling to live up to those expectations. The tech companies themselves are increasingly moving in on the banks’ territory, whether it is loans made by Amazon to small businesses or payment systems like Google Wallet.

Banks can learn lessons from GAFAA about how to understand and communicate with their customers and use that knowledge to meet their needs.

By forming partnerships with fintech, the banks can drive innovation in future products and services. They could surrender parts of their supply chain that others could run more efficiently, and concentrate instead on driving higher returns from other, more valuable parts of their businesses.

Collaboration has costs for all parties. Fintech partners will want a share of bank margins, which are already under extreme pressure. Fintech will have to deal with — rather than just step around — the lumbering giants of the financial services industry.

Bank CEOs will know they are winning in digital when bank valuations start to factor in the future value of innovation as well as an ability to protect their core franchise. No wonder bankers feel the need to talk about fintech. A re-rating is an attractive upside. But the potential price of getting it wrong is far greater: the threat of becoming obsolete.

Richard Lumb, based in London, is group chief executive of financial services at Accenture and founder of the FinTech Innovation Lab London, part of Accenture.

Get more on trading and technology.