Illustration by II

Past behavior is often called the best predictor of future behavior, but it’s well known that incentives drive behavior. Too often allocators believe these incentives come purely from dispassionate compensation structures and contractual protections at their investment managers. Although alignment of interests is indeed important, human beings are not machines. The key to true motivation and self-fulfillment at work comes from something deeper.

According to Daniel Pink, author of New York Times bestseller Drive, there is a serious mismatch between what businesses believe about motivation and what science knows. Business thinks that compensation, an extrinsic motivation, is the most effective means of compelling desired behavior. Pink argues that it is instead somewhat like a sugar high — effective at providing a short-term jolt but not capable of incentivizing over the long term. He cites some interesting studies that seem to support his contention that money isn’t the best motivator.

For instance, Pink describes research that has shown that children are actually less likely to produce a drawing if offered a monetary reward than if simply asked to draw something. And other research from the journal Health Psychology in 2013 shows that monetary rewards may actually demotivate people, reducing intrinsic motives in the long run.

Drawing on four decades of research into motivation, Pink argues that the secrets to sustainable high performance and job satisfaction come instead from three intrinsic incentives: autonomy, mastery, and purpose. People want the freedom to control their workflow, they want the flexibility to learn and improve, and they want to find a bigger purpose to which they can link their job performance. For investors that may involve managing the investment process; continual learning and process improvement; and linking their performance to specific social objectives, such as paying the retirement benefits for thousands of civil servants or funding research for a cherished philanthropic cause. This is how one finds meaning in the day-to-day work, an important objective for humans who have met their basic physiological needs, as psychologist Abraham Maslow argued decades ago.

In a landmark paper titled “A Theory of Human Motivation,” Maslow published the groundbreaking hierarchy of needs, in which he describes a five-stage model of human motivation. Broadly, these needs are divided into two main categories: deficiency needs, or those that arise from a lack of something and motivate us to fill that deficit, and growth needs, the things we desire so we can grow as human beings. Only once people have fulfilled the deficiency needs at the bottom of the pyramid —food, water, rest, shelter, and safety — can they move on to trying to meet their psychological needs. Someone struggling to stay alive is not going to be concerned with fostering a sense of belonging and accomplishment; that person’s efforts will be focused on survival.

After establishing relationships and meeting the need for belonging, people then can turn to achieving a sense of accomplishment. At this level, called esteem needs, people’s psychological drives are more about status, prestige, and respect. At first, people want respect from others, a step up from feeling like they belong. But at some point, humans experience a need for self-respect. We all want to feel important and worthy. Correspondingly, at the top of the hierarchy is the need to fulfill your ultimate potential, to be all you can be: self-actualization. Ideally, self-actualized people view the world with clarity, are comfortable with change and uncertainty, accept themselves and others for who they are, and — importantly — perform at a high level.

Maslow’s theory of motivation is a helpful framework for thinking about a great number of confounding social and psychological phenomena — for instance, why wealthier societies have higher suicide rates than poorer ones — but also suggests that the investment managers most likely to meet performance expectations are those who view investing as a vocation that connects them to a broader society and who, in part because of this, truly have the desire to generate the best returns they can. This may be one reason, as recent research shows, that purposeful companies outperform the stock market by 42 percent.

I believe true motivation must come not merely from an alignment of incentives between investors and asset managers, but, more important, from an alignment between the extrinsic and intrinsic motivations of a manager. In this framework, aligning incentives means ensuring that extrinsic compensation structures incentivize behaviors that are consistent with the intrinsic personal and professional motivations of the portfolio managers. Although compensation can be structured to pay people to do what you want them to do, in the long run people have an annoyingly predictable tendency to do what they want to do. And they probably will do their best work when they get paid well to do what they really want to do.

For the past six years, I have conducted aptitude tests and personality profiles during my manager due diligence process. One takeaway that I did not initially expect has to do with an interesting correlation between value creation and intrinsic motivation. The specific test I use ranks each candidate’s top three areas of interest across several different job functions, such as people service, enterprising, mechanical, technical, financial and administrative, and creative, similar to the career guidance tests many of us took in high school to nudge us toward jobs in science- or art-related fields according to our aptitudes.

The test identifies a respondent’s top three areas of interest and compares the candidate to average employees in similar jobs, standardized against thousands of other respondents from the financial services sector. This got me thinking that even with a small sample set, I might be able to see patterns emerge relative to more granular job functions in private equity.

Of course, it made sense that industrial buyout shops had mechanical interests and that fintech firms showed aptitude for both financial and technical job functions, but I thought I might be able to get deeper with the data. Which takes us to value creation. Let’s take a quick look at private equity drivers of return before coming back to motivation.

In private equity — assuming one does not take dividends along the way — returns can come solely from selling a business for more than it cost to acquire. And this sales price will be determined by applying a multiple to the terminal earnings of the business. Mathematically, it’s a tautology: price = price/earnings * earnings.

Practically speaking, how you get there matters. Those future — and hopefully higher — earnings can be generated only by revenue growth or changes in the profit margin. And the equity payout will come from the multiple applied to the entire business, less the amount needed to repay debt. Hence the capital appreciation will come from revenue growth and changes in profit margins, in the mix of debt and equity, and in the earnings multiple at sale.

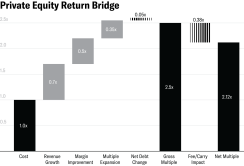

By decomposing a private equity manager’s historical returns into these components, one can create what is known as a return bridge. The graph below provides an example where a private equity firm has generated a historical net multiple of invested capital, or MOIC, of 2.12x on its portfolio. For every dollar investors have given the fund, it’s given $2.12 back.

Now in this case, we can see this manager grew revenue by 170 percent over the hold period, which equates to 0.7x of MOIC from top-line growth. It’s also improved the profitability of its firms, adding 0.5x of equity value from increasing margins. Additionally, the manager has been able to consistently sell its businesses at higher earnings multiples, leading to a further 0.35x of MOIC. Changing debt levels had little effect on the final equity value, which means this manager paid down some debt and put slightly more on the balance sheet — perhaps to finance expansion needed for revenue growth, or for new, more efficient equipment that helped enhance profit margins. So from the gross of $2.50, the general partner takes $0.38 for its fees and carries, leaving limited partners with $2.12. Not a bad return profile.

Now not all strategies or managers within private equity create value in the same way. Venture capital funds rarely if ever have companies that are profitable, so all of their firms are bought and sold on a revenue multiple, which typically contracts as a company grows and the top-line growth rate moderates. Thus virtually all the terminal equity value comes from revenue increases, which can be five to ten times initial sales.

Buyout shops, on the other hand, tend not to create nearly as much revenue growth. There will likely be profit margin improvement, but a larger relative percentage of the value creation will probably come from buying the company cheaply and paying down the debt over the hold period, like amortizing down a mortgage. They will own more of the equity when they sell at a higher valuation, so they benefit from the acquisition leverage.

And in between the two ends of the spectrum sit growth equity mangers. These strategies often buy smaller businesses that still have substantial revenue growth opportunity in front of them but also are profitable, or at least very nearly so. These managers can create substantial value from the combination of both top- and bottom-line growth, as well as consistent margin expansion — not necessarily because they buy cheap, but because they are able to create a bigger, more profitable business and command a higher multiple. Oftentimes growth managers use no debt at all at acquisition.

One observation I’ve been able to draw from the data is that there is a high correlation between areas of interest and the relative proportion of value drivers. The perception that managers in the above strategies should want to generate more value from one of these interests is confirmed by the data.

I created a proprietary ratio, aggregating the scores of investment team members at each GP across three areas most clearly linked to these drivers: enterprising (or building and scaling a business), financial and administrative, and creative. Then I averaged this intrinsic motivation ratio, or i ratio, across all the managers in the sample across venture, growth, and buyout. The differences were stark.

Even more impressively, when I compared the scores of individual managers within categories against their own return bridges, the pattern was confirmed. For example, buyout managers that were growthier in nature scored higher in enterprising, and growth managers that leaned toward earlier-stage, unprofitable businesses tended to be more creative.

As most private equity shops are run by founder-entrepreneurs, it’s reasonable to assume they built businesses to do what they wanted to do. They have the autonomy to master the things that give them purpose. Simply put, they can get paid to do what they enjoy doing. And instead of doing purely subjective diligence around such concepts, this behavioral tool allows me to quantify the effect objectively.

It is my opinion that managers who are engaged in a value creation process that they truly believe in — one that gives them a sense of personal fulfillment and accomplishment — have higher odds of persistence of returns and lower probability of style drift. And the ability to identify those behavioral tendencies ex ante sure looks a lot like alpha ex post.