Executive summary

- Not only has U.S. Investment Grade (IG) Credit performed well in the most recent period of rising rates, spreads for the asset class have historically tightened when rates have risen in the past.

- Sharp and sudden rates movements have historically been most disruptive for IG Credit. However, given the robust market backdrop for IG Credit we believe that additional episodes of spread widening will likely be temporary, a dynamic that will create attractive entry points for investors in the near term.

- IG Credit has also historically outperformed Treasuries during periods of rising inflation.

Rising rates and higher inflation remain among the most topical concerns with both domestic and foreign investors in U.S. Investment Grade (“IG”) Credit. Entering 2021, we discussed various factors that could lead to a move higher in U.S. interest rates and a steeper Treasury curve, notably above trend economic growth, abundant Treasury supply to fund fiscal stimulus, and higher cyclical inflation. We also noted several factors that, in our view, would cap how high and how steep the yield curve could move in the near to medium term, including global yield differentials, continued accommodative monetary policy and quantitative easing, and the lack of structural inflation. In this post, we will discuss why we believe this rate rise will not be disruptive for the IG Credit market.

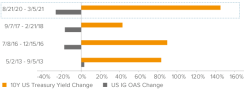

After steadily rising since their lows in August 2020, Treasury yields pulsed higher in February 2021, with the yield on the 10-year note settling at 1.39% as of month end after reaching an intra-day high of 1.61% on February 25. Despite this move higher, we maintain our stance that further steepening will be gradual, albeit with potential short-term bouts of volatility, leading to more attractive entry points for fixed income investors. Encouragingly, credit markets have remained resilient, with spread moves mostly muted. As Figure 1 highlights, IG Credit has historically performed very well in periods of rising rates, as spreads have tightened in 3 out of the last 4 periods of rising rates (negative percentage change in OAS indicates spread tightening or positive excess performance for IG Credit). In the most recent period of rising rates, IG Credit has actually posted its best performance.

Figure 1. IG Credit Spreads Have Primarily Tightened During Previous Periods of Rising Rates

IG Spreads in Rising Rate Periods

As of 02/22/21. Source: Credit Suisse. Rising rate periods defined using normalized percentage move. Negative percentage change in OAS indicates spread tightening, i.e. positive excess performance for IG Credit.

Episodic rate volatility reinforces importance of active management

While elevated rate volatility could lead to a widening in spreads, the market backdrop suggests that any move wider will prove to be temporary. First, the recent rate volatility is associated with the repricing of economic strength rather than with declining rates and a weakening fundamental outlook. In other words, we believe any spread widening will be a more temporary event because it is not a precursor to bigger picture credit market challenges. Additionally, bigger picture outcomes tend to be influenced by the outcome in financial conditions, which are easy and are going to remain so for the foreseeable future. The market has pulled forward its expectations for rate hikes aggressively, implying concerns that future financial conditions may tighten faster than expected. With that said, this risk has now largely been priced in and subsequent rate moves from here are likely to be more gradual.

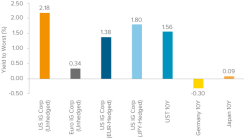

Second, higher yields in a low global yield environment will continue to attract demand for IG Credit from yield-based buyers, particularly pension plans and overseas buyers with hedging costs remaining low. As shown in Figure 2, the yield advantage of U.S. IG Credit over other fixed income sectors remains significant on both an unhedged and hedged basis.

Figure 2. Relative Value: IG Credit Continues to Offer Attractive Yield

As of 03/05/21. Source: Bloomberg.

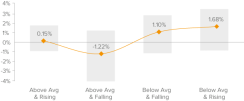

In addition to a favorable technical backdrop, IG Credit fundamentals are also strong, which should help shorten any move higher in spreads. The move higher in Treasury yields is primarily reflationary, driven by continued optimism for stronger nominal GDP growth in the U.S. Yes, near-term inflation concerns are also a factor, but inflation, nominal GDP growth, and corporate sales growth are all highly correlated. In our view, there is still too much excess capacity in the economy and slack in the labor market (on top of existing global disinflationary pressures) to create a sustained move higher in structural inflation. Rather, we expect there will be temporary inflationary pulses that will be more cyclical in nature. With that said, even with below-average but rising inflation, the associated uptick in economic and corporate sales growth should be net beneficial and has historically been associated with the outperformance of credit versus Treasuries (Figure 3).

Figure 3: IG Credit Has Historically Outperformed Treasuries During Periods of Rising Inflation

US IG Excess Forward 12m Returns by Inflation Bucket

As of 02/05/21. Source: Bloomberg, Morgan Stanley Research. Note: Orange dots show median while gray bars show interquartile range. Data series starts in 1970 and inflation buckets are defined using changes in U.S. headline CPI.

While higher input costs hurt some companies, others make money and there are likely more winners than losers. If consumer price inflation is occurring then presumably there is an ability for companies to pass costs through the entire supply chain, although there may not be 100% pass through at each level of the distribution channel. This would suggest a much broader array of “winners” than if there was mere input cost inflation that would lead to declining margins. Additionally, input costs are only a portion of the ultimate selling price, so 100% pass through is not necessarily required for companies to sustain their margins. A timely example of this would be homebuilders, an industry that is prospering despite strong input cost inflation. Lumber prices have surged yet builder margins are still expanding given strong home sale pricing power.

Ultimately, a continued move higher in rates could lead to a move wider in spreads, but there is a limit to how high rates can go without a change in policy signaling from central banks. We do not think rates can reach levels that would have a negative impact on credit, as refinancing would remain cheap even at those higher yield levels, and the impact on interest coverage ratios will be slow moving. As such, we believe any spread widening would be temporary and we would look at any such event as a buying opportunity given the positives of an improving economic environment and presumably declining credit risk should dominate.

For additional detail or more from Voya Investment Management, click here.

Past performance does not guarantee future results. This commentary has been prepared by Voya Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management's current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors.

CID# 1567432

©2021 Voya Investments Distributor, LLC • 230 Park Ave, New York, NY 10169 • All rights reserved.