Illustration by Zoe van Dijk

At the Yale School of Management’s summer school for Chinese executives, the bigwig investment speaker had a message: Don’t try what we did.

Charles Ellis, the lecturer, oversaw Yale’s famous investment office for 17 years as investment committee chair, and knows the effect its success has on people. Some see the extraordinary outcome, want to duplicate it, and ignore what makes their situations unique. “I’m thinking of one of the great lines in the history of movie making,” Ellis tells Institutional Investor in an interview, referring to the faked-orgasm scene in When Harry Met Sally. “‘I’ll have what she’s having.’”

As Billy Beane reshaped baseball through the use of analytics, Yale’s endowment revolutionized investing. Not simply by being better, although it was, but by creating a new model altogether — which, in turn, created a movement.

The architect of Yale’s model is David Swensen. The university’s chief investment officer for nearly 35 years, Swensen has raised an entire generation of endowment CIOs in his image, and explained Yale’s strategy to the world in his hit book. Yet the greatest institutional investment machine of modern times, though much imitated, has almost never been replicated. Legions of U.S. nonprofit CIOs claim they’re “doing the endowment model.” They’re not.

“David took the time and his talent to figure out — in a way that no one had yet figured out — what endowment investing was all about: perpetual institutions and their long-term health,” notes Ellis. As CIO, Swensen found the right answer for Yale’s continuing vitality. According to his former chair, “It was new, unconventional, and initially difficult for many people. But he explained it so well that soon the whole context of endowment management was changed forever.”

In his summer school presentation, Ellis argued vigorously against the active investing style that, under his watch, made Yale billions and Swensen into an icon. “Disagreeable Data: Losers lose twice as much as winners win,” one slide declared, noting that most mutual funds and institutions are losers. “Reverse the question,” another slide read. “Would you ever consider going active knowing: Higher fees, lower returns, more portfolio risk, more manager risk, takes more time, more uncertainty?” Having dissuaded the Chinese executives from striving for Yale’s portfolio, Ellis gave them a peek inside.

“What Makes Yale Endowment Unique:”

- Discipline at All Times

- All Equity

- Homework Before Meetings

- Liquidity Limits

- Rigorous Policy Portfolio

- New Managers

- Stock Lending Policy

- YALE

- Weekend of Thanks

- 35 Years of Building Network

- David Swensen

- David Swensen

- David Swensen

Of the myriad things from Yale to mimic, why this one? “Human beings are stimulus-response animals,” explains economist Paul O’Brien, former deputy CIO of the Abu Dhabi Investment Authority. “You don’t question if it’s worked — you probably do more of it.” Compared with passive or even traditional long-only investing, he adds, “it’s also more fun. iShares doesn’t take you out to dinner or invite you to conferences.”

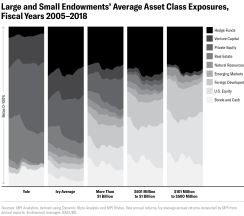

The share of total U.S. nonprofit money invested in alternatives has doubled in the past 15 years, according to the National Association of College and Business Officers, the sector’s longtime surveyor. Private equity, hedge funds, venture capital, real estate, and the like accounted for 27.7 percent of endowments’ and foundations’ invested assets in 2003. As of June 30, 2018, alternatives made up more than half (52 percent). Swensen spurned fixed-income, and the community copied him. In 2003, nonprofits had one of every five dollars invested in bonds (21.4 percent of institutions’ dollar-weighted average allocation). They’ve since slashed fixed-income by more than half. The average allocation is 7 percent among funds with upward of $1 billion.

Institutions tend to have dedicated investment staff at about the $1 billion mark — the three-comma club — whereas smaller funds are often run ad hoc by trustees or CFOs. Not coincidentally, that’s also the point at which funds start trying to be Yale.

“Notably, the ‘Yale Model’ that dominated Ivy endowments over the past ten-plus years has been adopted with the same rate of growth by large endowments, with assets above $1 billion, and the rest of the Ivies,” according to research from Markov Processes International. The quantitative analysis firm has a method for back-solving portfolios using returns rather than squishy self-reported allocations, and produced a study for Institutional Investor. “We see the Yale Model is adopted outside of the Ivies,” says CEO Michael Markov. “The trend is there.” Institutions above $1 billion have moved into private assets at the same rate — headlong — “but the larger funds dominate return-wise over smaller funds,” he explains. “The Ivy average dominates the $1 billion-plus average, and Yale dominates everyone. Whether the analysts included the global financial crisis or didn’t, the trend is exactly the same. The bigger the fund, the bigger the returns; smaller endowments, smaller returns.”

Institutions may quibble with these estimates, but data and logic support MPI’s conclusion. If you try to build a Maserati out of bicycle parts, it’s not going to go very fast and it’s not a Maserati. And maybe what you need is a bicycle.

Consultant Anna Dunn Tabke has worked with nonprofit institutions throughout her career, and has wrestled with this mismatch of ambition and capability. “Yale has a brand,” she says. “Even endowments and foundations that don’t have a blue-chip brand want to get into the same kind of deals as Yale, which obviously creates some challenges.” Her role as a consultant, of course, is to help clients get what they want.

But can the endowment model work with $2 billion and a small internal team? Tabke hesitates.

“It is . . . very difficult,” she says. “There are only so many really good alternatives managers, and they are oversubscribed. People are beating their doors down.” The best and often only way to get past those hallowed doors is to already be inside. Yale’s average manager relationship lasts 17 years, Ellis notes. Being able to write big checks helps too, as does having an esteemed institutional brand. But without either, allocators simply knock on door after door until a manager lets them in, then repeat the process until they hit their target allotment. With so much money flowing into alternatives managers, institutions are doing a lot of knocking.

Allocating from dregs is inherently more dangerous in private markets, Tabke points out. “In private equity there is a huge gap between the bottom- and top-performing funds. If you get it wrong, that can be very costly. You can put yourself in a big hole relative to your peers. Also, going heavily into illiquid assets doesn’t help if the public portfolio collapses. If a university relies on the endowment, it’s not going to make payroll. Kids aren’t going to get scholarships.”

For all of these well-documented pitfalls, institutions can’t seem to help themselves. David Swensen has beaten the market, and others want to as well. Cultural momentum has gathered around the endowment model — stripped down to its private markets tilt — and herding offers job security, according to Tabke. “Whether it works or not, you’re almost going to feel like you have to try it. Those who choose to pursue anything different will be taking on career risk. Ironically, that’s exactly what David Swensen did. He proved that if you’re willing to buck the crowd, you can accomplish the amazing.”

But you also might get fired.

In Ellis’s view, “IBM and the World Bank are two truly outstanding intellectual forces, and that they understood— through David’s explanation — why the deal made sense for them is stunning.” Swensen applied the same methodical creativity to investing Yale’s portfolio when the task landed in his lap a few years later.

Yale economics professor William Brainard called Swensen, according to an insider: “‘David, you’re going to take the biggest pay cut anybody has ever taken, and you’re going to manage the endowment.’ And David said, ‘Come on. I don’t know anything about managing an endowment.’ Bill said, ‘You know and I know you will figure it out, and when you figure it out, you’ll be the best endowment manager the world has ever seen.’” Brainard was correct on both counts. Swensen took the pay cut — 80 percent, reportedly — and moved to New Haven.

Privately, the young economist-turned-trader had a spell of impostor syndrome. “I was skeptical because I had no portfolio management experience,” Swensen said during a 2009 Lunch With the FT interview. “I remember wondering, even after I got to Yale, whether they were really serious about putting me in charge of this billion-dollar portfolio, because it seemed like an enormous amount of money and a big responsibility, and I’m not quite sure why it is they would have chosen me to do it.” He dove into the endeavor nonetheless, and spent two or three years doing his homework on what works for an endowment and why.

The system he developed extends far beyond the alternatives-heavy allocation template that some call the “Yale Model.” Indeed, people intimate with the fund spend much more time talking about risk management, manager relationships, and portfolio construction than they do about how big a bucket venture capital should be. Discussing Yale’s work as if it’s a portfolio recipe drives Swensen crazy, according to a longtime associate.

“He really, really can’t stand it when people take what he’s done and summarize it and therefore trivialize it. It’s really complicated stuff,” the associate says. Then they imitate someone trivializing it: “‘The Yale Model: What you have to do is a lot of hedge funds and venture and private equity and real estate. The percentages should be something like this.’ That’s not the starting point. That’s near the end! The starting point is understanding what is unique about this particular institution.”

Spending policy, for example, comes before any discussion of investing in Swensen’s Pioneering Portfolio Management. The book is essentially a guide to Yale’s model, which Swensen wrote reluctantly, according to Ellis’s introduction. Swensen was worried that smaller endowments might lust after Yale’s returns without the resources to achieve them. That’s precisely what happened, of course, but the book isn’t at fault. Any small institution with Swensen ambitions likely skipped the section on consultants, for example.

“Consultants express conventional views and make safe recommendations,” Swensen argues. “Selecting managers from the consultant’s internally approved recommendation list serves as a poor starting point. . . . Clients end up with bloated, fee-driven investment management businesses instead of nimble, return-oriented entrepreneurial firms.” Under-resourced CIOs often lean heavily on consultants and refer to them as “an extension of staff.” To Swensen, who recognizes the privileges of his budget, they are a “dysfunctional filter” selling a shortcut to hard work. “As is the case with many shortcuts, the end results disappoint.”

But perhaps the most overlooked principal of Yale’s investment strategy is the cold and humble assessment of one’s own institution. “Only foolish investors pursue casual attempts to beat the market, as such casual attempts provide the fodder for the skilled investors’ market-beating results,” he writes. “Even with adequate numbers of high-quality personnel, active management strategies demand uninstitutional behavior from institutions, creating a paradox few successfully unravel.”

“I think we would be kidding ourselves — almost to the point of being delusional — that we could do what Yale does,” Neale says by phone from Lincoln. “So many endowments and foundations have haphazardly or off-the-cuff decided that they’re going to replicate what Yale does. You don’t see that in other areas of institutional investing. For example, a pension plan’s decision on whether or not to adopt an LDI [liability-driven investing strategy] is going to be very idiosyncratic to that institution.”

For many CIOs and boards, their performance rank versus peers matters more than matching their institutions’ particular needs, he believes. Competitive people flock to investing, and nonprofit institutions attract the country’s highest tier. (Endowments and foundations pay handsomely. David Swensen made $4.7 million in 2017, whereas the CIO of New York City’s $199 billion pension fund earned $350,000.) The mirage of outdoing Yale — just for one year — motivates many to try to beat Swensen at his own game. Reliable funding for faculty payrolls might not juice the ego, but that’s what is at stake.

“You’re going to end up locking up capital for a really long time, paying exorbitant fees to managers that may ultimately prove to be disappointing,” Neale notes. Those who try the model unsuccessfully tend to stick with it, too. “I think there’s a hesitancy to want to admit defeat. It’s pretty hard, if this is your career, to say, ‘We tried to do this for ten years, and I led the effort and we weren’t successful.’” Once you’re in, you’re in.

The endowment model has — and does — work at institutions beyond New Haven, which adds to its allure. A private database of U.S. endowment and foundation returns reveals a top decile stocked with devotees. The catch: They all trained under Swensen. MIT, Princeton University, Bowdoin College, and the Packard Foundation are led by former Yalies, and these are just the best performers. But others in this elite group — university and charity funds jockeying for top-ten positions — ascended without direct ties to Mecca, via strategies that depart from Swensen’s.

When Ana Marshall became CIO of the now–$9.8 billion William & Flora Hewlett Foundation in 2012, she had spent more than a decade there building an endowment-style portfolio. But Hewlett is a foundation, endowed by the “H” in computer maker HP, and Marshall took Swensen’s advice seriously. “I had to take what was there — the endowment model that Dave created correctly for the needs of Yale — and then modify it to what we were trying to solve for at Hewlett.” Its long-term returns rival Yale’s and, more important, fulfill the foundation’s mission.

Nowhere in that mission is besting her peers, although Marshall does with nearly all of them. “It’s cultural,” she says of intra-endowment jockeying. “There are still a lot of endowment CIOs who have peer performance in their compensation.” When Marshall arrived at Hewlett 15 years ago, she was puzzled by the codified competition. “There was this view that if someone was an undergrad at Stanford but went to grad school at Harvard, then if Harvard beats Stanford, they were more likely to give the dollar to Harvard than Stanford.” This is simply a theory, Marshall points out. Harvard not only has the worst ten-year returns in the Ivy League, but it ranks 113th out of 118 major U.S. nonprofits, according to the database. Harvard is not hurting for donations. Nevertheless, “it’s still very much alive and well in the Yale Model of endowment management to have peer performance” in pay packages.

Team size and makeup further separate Marshall’s task from Swensen’s. A $10 billion endowment would almost certainly have a larger investment staff, fed by a pipeline of the university’s brightest financial scholars. Yale’s track record of churning out institutional leaders is unmatched. Asked to define Swensen’s legacy, Marshall replies, “I think his ability to make investors. He takes really bright people, and he gives them a really healthy understanding of all aspects of investing. If anything, I’ve tried to model that more than the portfolio itself.”

Marshall invests where Yale and Swensen offspring won’t, and it’s worked for Hewlett. “I do look at large firms,” she says. “We have found some tremendously talented people within PIMCO that run individual mandates for us. I run fixed-income. None of them do because they don’t want to waste their cash on fixed-income, but I think it’s important.” According to Marshall, Yalies also exclude relative-value strategies — except for Bracebridge Capital, Nancy Zimmerman’s Boston hedge fund, and “maybe Bridgewater” Associates. “Everybody likes Nancy. But they will look at nothing else in the absolute-return space, because Dave doesn’t do it.”

Herding around Yale opens pockets of opportunity for investors like Marshall, but it also creates a much larger threat to Hewlett and Yale alike. Vast public pension funds and sovereign wealth vehicles have caught the private markets bug, and their huge checks compete with even elite asset managers’ ability to make returns.

“The really big money allocating 20 or 30 percent to privates — that’s where the model breaks,” Marshall says. “Endowments and foundations want to feel like they’re big, but they’re not. The Canadian pension funds and major sovereign funds have their own internal teams, which are more and more in direct competition with our private equity managers. Ironically, as all of this money pours in, it’s flowing into the asset classes that are most capacity-constrained.”

The impetus for stampeding into private assets is the same for institutions great and small, in Marshall’s view. “FOMO. They look at the returns we’ve posted, and their bosses are saying, ‘Why don’t you have that?’ They’re sad.” Many public pension leaders face a math problem where the only solution is private equity. As one public fund staffer recently told Marshall, paying out retirees as promised requires a 7 percent annual return, and the only way the expected-return model spits out 7 percent is by putting 30 percent into private equity. “Personally, I think it’s crazy,” says Marshall. “But I guess that’s their job. Whether they think it’s crazy or not is totally irrelevant.”

If a $2 billion charity tries to be Yale and fails, it’s the charity’s problem. If five $100 billion-plus public pension funds do that, that’s everyone’s problem.

These billions are coming, and they will inevitably push down the high returns that Yale and others have reaped for decades. This compounds the scale problem that Yale and other mega-endowments already wrestle with. Marshall admits that her own strategy’s “sweet spot” is $8 billion to $10 billion. She’s maxed out at $9.8 billion. But unlike Swensen, Stanford chief Robert Wallace, and MIT’s Seth Alexander, Marshall doesn’t have deluges of donations to constantly put to work. “At $30 billion, I just don’t know how you do it,” she says. “It’s a scale question. But if anyone has a chance of cracking it, it’s Rob and Dave and Seth.”

Swensen inspires loyalty — to a startling degree. As one of his associates half-joked, “If you don’t do the very best you can on this story, don’t forget your knees.” Swensen is known as a nice guy, but his friends aren’t above kneecapping in his defense. “Wear your shin pads.”