Equity investors know better than to rejoice over a January bounce in the markets. But I think that the recent sharp gains in global stocks may be more than just an impulsive reaction to the start of a new year.

Last year, equity markets suffered from extreme volatility amid fears that the escalating crisis in the euro area might push a fragile global economy back into recession. While the euro area still faces major challenges, recent policy steps have gone a long way to reassure investors.

In December, the European Central Bank’s decision to provide €489 billion to the region’s banks for three years sent the right signals to the capital markets. The latest Long Term Refinancing Operation has significantly reduced the liquidity risk to the financial system — and that’s a big deal. It also tells us that the ECB is ready and willing to throw all of its might into preventing a worst-case scenario such as a run on Europe’s banks.

This, in turn, has allowed investors to take comfort in signs of economic improvement elsewhere. In the U.S., real gross domestic product grew at a 2.8 percent annualized rate in the fourth quarter. Then, unemployment fell to 8.3 percent in January, giving us reason to believe that the jobs market is finally awakening and that the U.S. economy is capable of solid growth in 2012.

There’s also good news coming from China. Consumer price inflation fell to 4.1 percent in January after five straight monthly declines. This paves the way for looser monetary conditions, which makes it increasingly likely for China to avoid the hard landing that markets have feared.

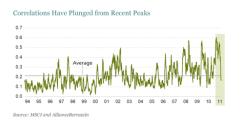

Our equities portfolios aren’t driven by a top-down macroeconomic approach. But for bottom-up stock-picking to succeed, you need the markets to let go of economic fears. During January, the pairwise correlation of global stocks started to recede from record highs in 2011, as the display below shows. Displays for U.S. and emerging market stocks look very similar.

High correlations mean that most stocks are trading in the same direction, with little regard for their fundamental strengths or weaknesses. That makes it extremely hard for active managers to beat their benchmarks. I see the recent decline in correlation as an encouraging sign that markets are starting to let go of apocalyptic macroeconomic fears and starting to take a cold hard look at stocks again.

This helps explain what did well during January. Cyclical sectors that were hit hardest in 2011 posted the strongest rebound. The MSCI World Index advanced by 5 percent, led by cyclical sectors such as commodities, capital equipment, technology and financials. Those are all signs of decreasing risk aversion.

Of course, it would be foolish to read too much into one month. We’ve all been through too much pain, and there are clear and present dangers on the horizon. Still, the trends in January give me confidence that equity markets haven’t irrevocably changed. Markets are capable of focusing on company fundamentals once again, and when they do, active managers who stuck to their guns during last year’s spell of volatility should enjoy a solid recovery.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AllianceBernstein portfolio-management teams.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices, any securities or financial products. This report is not approved, reviewed or produced by MSCI.

Kevin Simms is director of Global Value Research at AllianceBernstein