This blog is part of a new series on Institutionalinvestor.com entitled Global Market Thought Leaders, a platform that provides analysis, commentary, and insight into the global markets and economy from the researchers and risk takers at premier financial institutions. One of our contributors in this new section is BlackRock, which will be providing analysis and insight into fixed income.

When considering a future of slow economic growth and low nominal interest rates, and particularly one that resulted largely from the bursting of a property price bubble and increasing debt levels, it’s natural to want to turn to the past 20 years in Japan to think about economic lessons for other developed countries today.

At the outset we’ll concede that we don’t think the United States is going down the economic path that Japan has traversed over the past few decades, as the U.S. holds several favorable economic and demographic tailwinds Japan lacked.

When we compare both U.S. and Japan’s core CPI and 10-year government bond yields, using an 11-year lag (U.S. beginning in 1991 and Japan in 1980), the metrics follow a remarkably similar trajectory. At the same time, the governments of both countries saw budgetary balances that appeared to be on similar paths, and the velocity of money in both countries’ economies (US beginning in 1995 and Japan in 1984) also followed a similar (downward sloping) path. On this latter similarity, both Japanese and US banking sector balance sheets were impaired largely by real estate-related holdings and today higher capital requirements and a higher cost of funding may keep money velocity growth muted for some time. Finally, as Japan’s asset price bubble deflated in the 1990s the country’s labor market saw a doubling in the use of temporary workers (to near 6.5 percent of the labor force), which then remained at this high level for more than a decade. The U.S. has also seen a marked uptick in the use of temporary labor (yet still only 1.9 percent of the work force overall) since 2009, and we’ve argued previously that this cost-containing measure may become a more permanent feature of our labor markets as well.

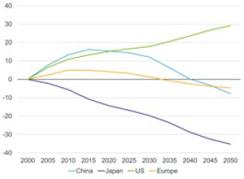

It is important, however, to not overstate the similarities between the case of Japan and that of the U.S., since there are some profound differences in their economic situations as well. Chief among these is the fact that the demographic profile Japan displayed in 1950, which served as an economic tailwind helping fuel its growth in the ensuing four decades, has faded and is projected to grow meaningfully worse in the decades to come. In contrast, the population dynamic in the U.S. is much stronger, and arguably the country has one of the best demographic profiles in the developed world today (see Figure 1). Another notable difference is the strength of the corporate sector in the U.S., which still displays high degrees of technological innovation, strong new business creation, and a productive and mobile workforce relative to many developed market peers. For instance, this strength is shown by comparing aggregate corporate return-on-equity by region, which stands near 17 percent for the U.S., 12 percent for Europe, but only 6 percent in Japan.

Figure 1: Percent Cumulative Labor Force Growth (ages 15-64)

More Favorable for the US

Chart 1

Source: Deutsche Bank |

Rick Rieder is BlackRock’s Chief Investment Officer of Fixed Income, Fundamental Portfolios.